9.3

8.833 reviews

English

EN

Central banks usually fight inflation with higher interest rates, but does this really address the underlying cause? In Argentina, inflation fell sharply while interest rates were being lowered. This raises the question of whether money growth is more important than interest rates.

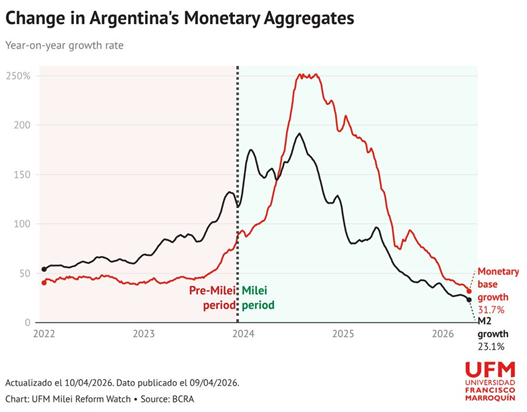

It sounds simple: if inflation is above the 2% target, interest rates should be raised; if it is lower, interest rates should be cut to stimulate inflation. When Javier Milei took office in Argentina in December 2023, many economists sounded the alarm over his plan to sharply reduce interest rates, something that has now happened nine times since he took office. Yet inflation fell from 211% to around 30% in 2026.

This raises the question of whether interest rates are the right instrument to fight inflation: what is the actual cause of inflation and what role does money supply growth play in this?

To determine the right weapon against inflation, it is important to understand what inflation actually is: the current description is often the general rise in prices of goods or services, but the issue is more nuanced. Inflation is, in reality, the redistribution of wealth through an artificial increase in the money supply. A classic example of this is the Denarius. The value of the Roman silver coin was debased by emperors. Coins collected through taxation were melted down and mixed with less valuable metals, allowing the emperors to create extra coins and thus increase their spending.

This leads to the debasement of the currency, which eventually causes prices to rise. The current definition treats the consequence as the cause. As a result, central bankers see everything that could potentially lead to price increases, such as wage growth, rising commodity prices or unemployment, as a possible inflationary threat against which action must be taken, according to emeritus professor Frank Shostak.

Although rising interest rates and quantitative tightening, policies that reduce the money supply, can certainly put pressure on the consequences of artificial money growth, such as inflation and economic bubbles, such intervention also leads to further distortions in market processes. Interest rates reflect what is known as time preference, which is the preference to consume now rather than in the future. When time preference declines, people save more, which leads to lower interest rates. Those lower rates then signal to companies that they should make more long-term investments, because capital becomes more cheaply available. Tight monetary policy distorts interest rates, prices and wages in the same way that artificial growth does. Economist Ludwig von Mises often described this with the example of a driver who had run someone over and then thought he could repair the damage by reversing over the victim again.

Stopping the artificial growth of the money supply, for example by ending central banks’ purchases of government debt or by abolishing fractional reserve banking, would undermine economic bubbles and inflation without disrupting market processes such as interest-rate formation. This could accelerate the economic recovery.

M1 money supply YoY growth in Argentina (source: BCRA)

With this theory in mind, Argentina’s sharp fall in inflation appears less surprising than many economists had predicted. Economy Minister Luis Caputo reported that a budget surplus had been achieved for the first time in 14 years, while the economy also posted strong growth figures of 4.4%. At the same time, inflation figures are tracking the money supply almost exactly and, according to economist Daniel Di Martino, they will probably continue to do so.

Defining inflation as the general rise in prices of goods and services means confusing the eventual consequence with the cause. As a result, central bankers see everything that could lead to rising prices as an inflation trigger against which action must be taken. Tight monetary policy undermines the consequences of artificial money growth, but at the same time it also distorts market processes, delaying recovery. Policy focused on stopping artificial growth also addresses these consequences without disrupting the economy. Falling inflation combined with strong economic growth is no coincidence, but the result of addressing the cause rather than the symptom-fighting carried out by most central bankers.