9.3

8.735 reviews

English

EN

Last week saw the release of a striking report by Deutsche Bank on the role of gold in a changing world. In 1989, historian Francis Fukuyama proclaimed the “end of history,” referring to the conclusion of the ideological struggle between communism and the liberal Western world. Analysts at Deutsche Bank now argue that history has firmly returned, marked by renewed great-power rivalry between nations such as the United States and China. Gold plays a crucial role in this shift, with emerging economies potentially driving the gold price significantly higher in the years ahead. In this weekly selection, we take a closer look at this analysis.

Brief explanation: why do central banks hold reserves? Central banks around the world maintain holdings of foreign currencies such as dollars and gold, known as foreign exchange reserves or gold reserves. They do this to support their domestic currency, maintain confidence, and withstand economic shocks. Since 2022, central bank gold purchases have contributed to rising gold prices.

The report by Germany’s largest bank is noteworthy. While the gold community has long pointed to the BRICS countries (including China, Russia, India, […]) and how they might use gold to challenge the dollar, established financial institutions have generally remained cautious on this topic.

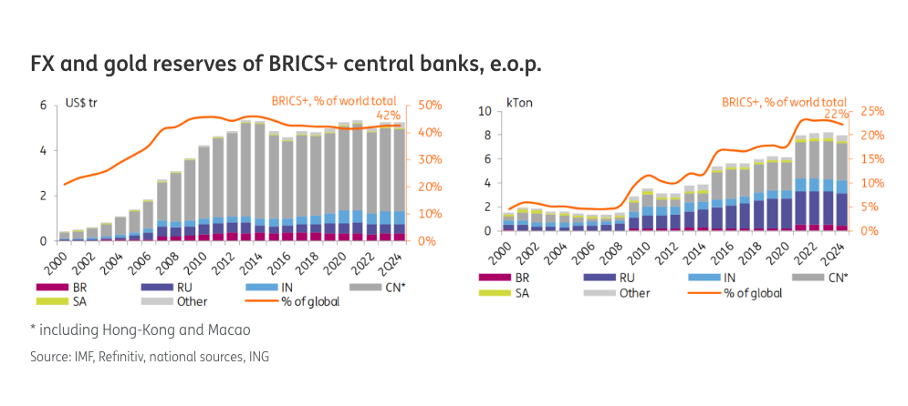

In 2024, :contentReference[oaicite:1]{index=1} published an extensive analysis on de-dollarization, identifying gold as a potential alternative for countries seeking to reduce their exposure to the dollar. However, their analysts saw limited chances of success, particularly in the short term. In their view, BRICS+ countries hold only around 10% of their reserves in gold, with both gold and foreign exchange reserves remaining relatively stable in recent years. Moreover, they did not expect that even a shared BRICS currency would pose a serious challenge to the dollar. According to ING, the global order largely remains intact, with only marginal changes at the edges.

Share of global dollar reserves held by BRICS+ central banks and their gold reserves as a percentage of the global total (orange line) in 2024 (source: ING).

Share of global dollar reserves held by BRICS+ central banks and their gold reserves as a percentage of the global total (orange line) in 2024 (source: ING).

Deutsche Bank takes a very different view. Their extensive analysis highlights the strong possibility that gold will indeed play a major role. They examine how shifts in the global order have influenced central bank gold reserves since the 1950s. The report even considers the possibility that emerging economies or BRICS nations could use gold as backing for a new international payment currency (p.15). Even under conservative assumptions, Deutsche Bank analysts arrive at a gold price of $8,000 per troy ounce, compared to the current level of around $4,500.

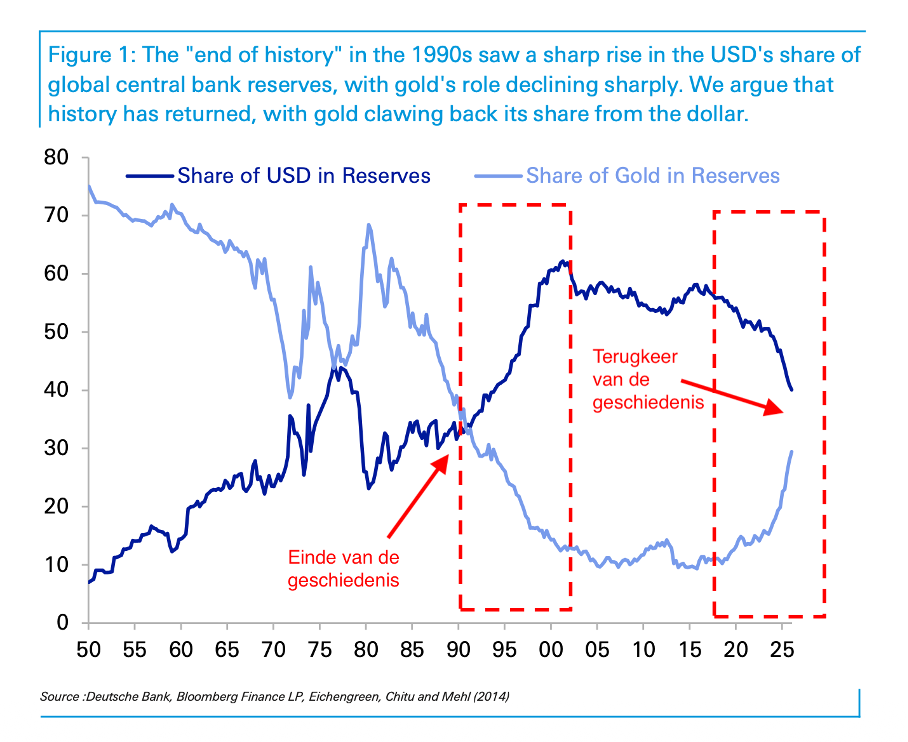

According to Deutsche Bank analysts, global central bank gold reserves are a key reflection of geopolitical tensions and challenges. Interestingly, the abandonment of the Bretton Woods system was not decisive in prompting central banks to reduce their gold holdings. President Nixon ended the final remnants of the gold standard in 1971, after which gold no longer had a formal role in underpinning the financial system. Yet during the turbulent 1970s, gold reserves actually increased. In that same decade, gold prices surged by 1,000%.

Global central bank reserves since the 1950s, based on IMF data. The light blue line shows the share of dollars in total reserves, while the dark blue line shows gold (source: Deutsche Bank).

Global central bank reserves since the 1950s, based on IMF data. The light blue line shows the share of dollars in total reserves, while the dark blue line shows gold (source: Deutsche Bank).

It was not until 1989, with the fall of the Berlin Wall, that international tensions appeared to ease. :contentReference[oaicite:2]{index=2} famously described the end of the Cold War as “the end of history.” This marked the beginning of the 1990s, when the liberal Western order seemed triumphant. The decades that followed saw unprecedented prosperity, peace, and economic growth, driving globalization to new heights. In this era of stability and security, gold came to be viewed as a barbaric relic of a bygone age. Only once geopolitical tensions had subsided did central banks begin to significantly reduce their gold holdings.

We see that the share of gold reserves declined and eventually crossed paths with rising dollar reserves. Confidence in the United States as the dominant global power was reflected in the growing share of dollar reserves held by central banks worldwide, often in the form of U.S. Treasury bonds.

Why did the “end of history” coincide with an increase in dollar reserves? During this period, the dollar had become the world’s primary currency, used for virtually all major international transactions, from oil to inexpensive goods produced in emerging markets. Global trade expanded rapidly, and between 1990 and 2007, global foreign exchange reserves grew ninefold. The declining share of gold was not only due to sales but also to the much faster expansion of dollar-denominated assets. A significant portion of these dollars flowed to countries like China through trade surpluses—something policymakers such as :contentReference[oaicite:3]{index=3} have sought to address.

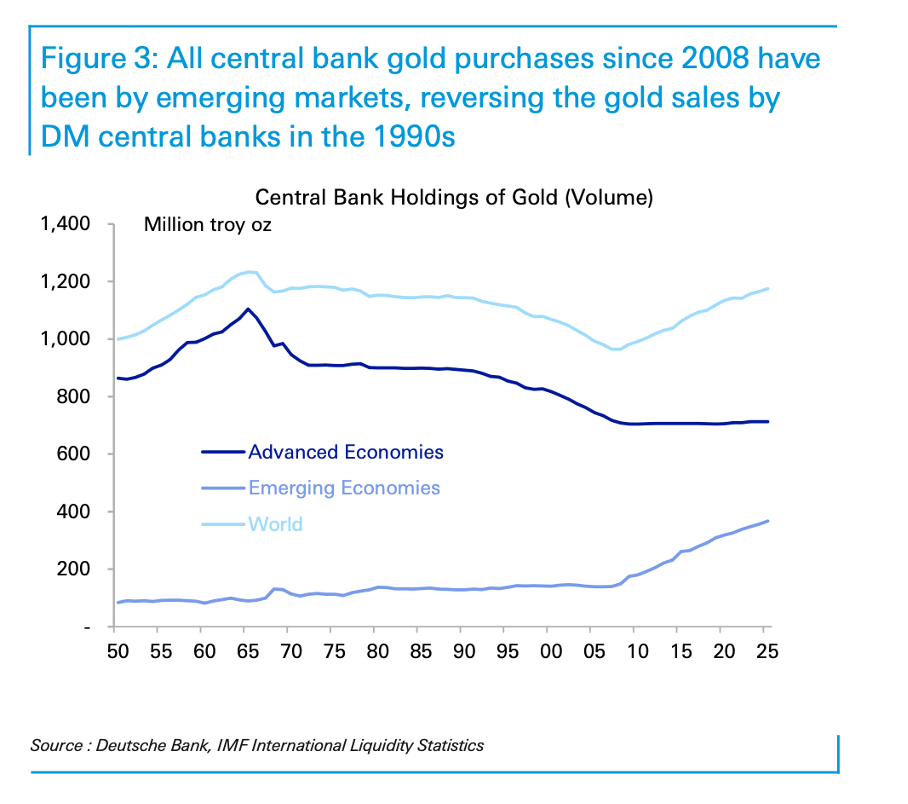

Central bank gold reserves in volume (millions of troy ounces) have been rising again since 2008, largely driven by emerging economies (including BRICS countries). Note: gold volume increases steadily, while its value rises significantly (source: Deutsche Bank).

Central bank gold reserves in volume (millions of troy ounces) have been rising again since 2008, largely driven by emerging economies (including BRICS countries). Note: gold volume increases steadily, while its value rises significantly (source: Deutsche Bank).

According to Deutsche Bank analysts, Fukuyama’s “end of history” no longer holds. This is reflected in declining dollar reserves and rising gold reserves. Central banks in emerging economies, in particular, are increasing their gold purchases, while developed economies tend to maintain their holdings. The main reasons behind the return of history, according to the analysts, are:

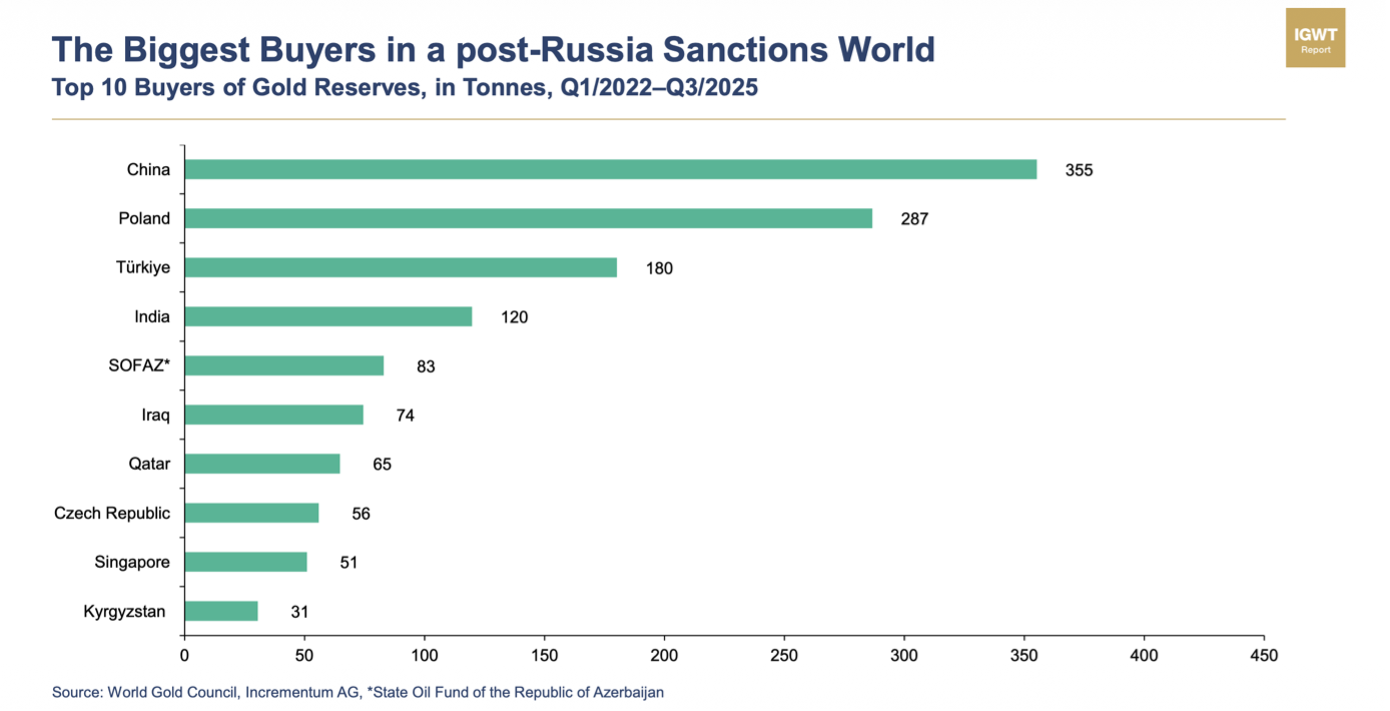

Gold purchases (in tonnes) by the top ten gold-buying central banks (source: In Gold We Trust report chartbook).

Gold purchases (in tonnes) by the top ten gold-buying central banks (source: In Gold We Trust report chartbook).

Central banks in countries such as Turkey, China, India, and Russia are among the largest buyers of gold, alongside former Soviet states led by Poland, the Czech Republic, Azerbaijan, and Kazakhstan. According to IMF data, the share of dollar reserves has declined from a peak of 60% of global reserves to around 40%, while gold has risen to approximately 30%. It is worth noting that IMF data tends to provide more conservative estimates of gold holdings compared to institutions such as the World Gold Council. As discussed in our recent market update, gold reserves may already have surpassed dollar reserves, with central banks expected to continue large-scale purchases in 2026.

In recent years, central banks have consistently increased their gold reserves by weight, contributing to rising gold prices and allowing gold to gain ground relative to dollar reserves. Does this signal a peak, or is there still a long way to go? And how far could prices rise?

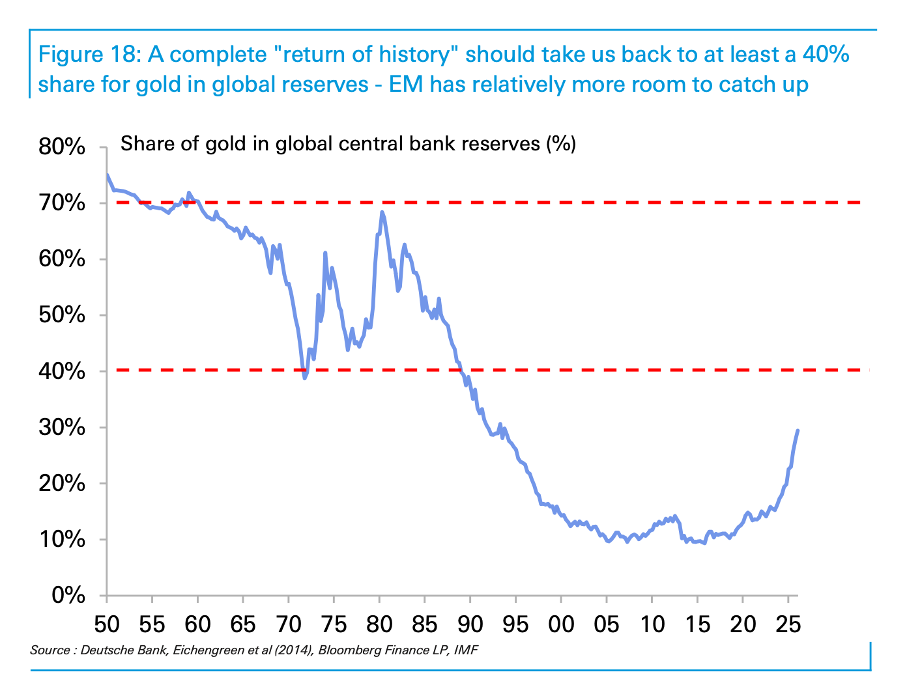

Deutsche Bank analysts assume a “return of history” and a shifting global order. Looking at the period between the 1950s and the end of the Cold War in 1990, gold typically accounted for between 40% and 70% of central bank reserves. If we return to a world characterized by geopolitical tension, central banks could once again move toward those levels.

Gold accounted for between 40% and 70% of central bank reserves between 1950 and 1970 (source: Deutsche Bank).

Gold accounted for between 40% and 70% of central bank reserves between 1950 and 1970 (source: Deutsche Bank).

In developed economies, gold reserves have remained relatively stable and now account for about 34% of total reserves, partly due to the sharp increase in gold prices. In emerging economies, however, this figure is only around 16%, indicating significant room for growth. At the Chinese central bank—one of the largest gold buyers in recent years—gold accounts for just 9% of total reserves. According to the analysts, this suggests substantial potential for further accumulation.

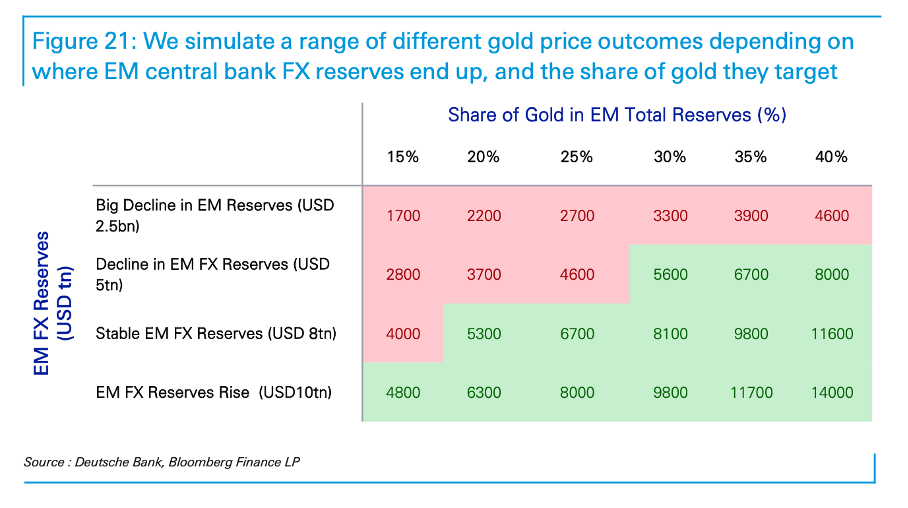

The gold price could rise dramatically if central banks in emerging economies continue to expand their gold holdings, the analysts conclude. They developed several scenarios based on the total size of foreign exchange reserves. If reserves remain at approximately $8 trillion and gold’s share increases to “just” 30%, this would imply a gold price of $8,100 per troy ounce—nearly double the current level. If the share rises to 40%, the price could reach as high as $11,600 per troy ounce.

Various scenarios based on total central bank reserve sizes; the current level corresponds to the third scenario at $8 trillion (source: Deutsche Bank).

Various scenarios based on total central bank reserve sizes; the current level corresponds to the third scenario at $8 trillion (source: Deutsche Bank).

The ongoing accumulation of gold reserves may signal the early stages of a potential return to a new monetary system anchored in gold, the analysts write. While such developments remain far from concrete, they place them in a historical context and identify a clear long-term trend in that direction. Notably, the value of all above-ground gold has risen so significantly in recent years that it now exceeds the total value of tradable U.S. government bonds—long considered the ultimate safe haven since 1990. A clear sign, perhaps, that history has indeed returned.