9.3

8.770 reviews

English

EN

Stagnating economic growth combined with rising inflation, that is stagflation. Former president of De Nederlandsche Bank, Nout Wellink, states that the Netherlands is on the brink of stagflation. The major fear is a return to a prolonged period of stagflation, similar to the 1970s following the oil crisis. Will the current oil crisis trigger a repeat of history? What can governments still do in light of rising sovereign debt and what are the implications for gold and other precious metals?

Central bankers such as Fed chairman Jerome Powell and Christine Lagarde of the ECB emphasized during recent interest rate decisions that there is absolutely no repeat of the stagflation seen in the 1970s. “Stagflation was an appropriate characterization of what happened in the 1970s […] and that concept is best left there,” said Lagarde. Their reasoning is that conditions back then were far worse, a unique period in history during which unemployment and inflation surged while growth stagnated.

ECB President Lagarde during the ECB interest rate press conference on April 30, photography by Felix Schmidt, source: ECB

ECB President Lagarde during the ECB interest rate press conference on April 30, photography by Felix Schmidt, source: ECB

“Lagarde should stop overcomplicating things, this is simply a stagflationary shock,” responds Lex Hoogduin, emeritus professor of economics at the University of Groningen. And he is not alone. Nout Wellink, former president of De Nederlandsche Bank, also warns of approaching stagflation, with economic growth at just 0.1% and inflation moving toward 3%. He fears the wrong response from labor unions and governments, where demands for higher wages and additional government support would only further fuel inflation.

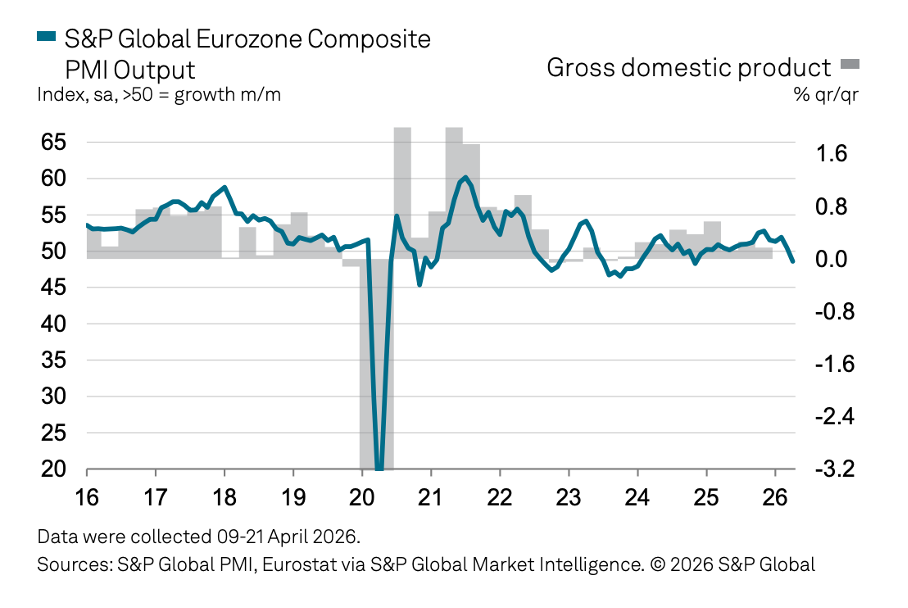

European Purchasing Managers’ Index shows -0.1% GDP and production contraction, with the largest declines occurring in 2020 after the outbreak of the pandemic, source: PMI S&P Global

European Purchasing Managers’ Index shows -0.1% GDP and production contraction, with the largest declines occurring in 2020 after the outbreak of the pandemic, source: PMI S&P Global

So is Europe completely blind to this risk? Apparently not entirely, judging by the statements made by European Commissioner for Economic Affairs Valdis Dombrovskis on May 4: “Higher energy prices affect every player in the European economy, businesses and households alike, pushing the EU economy toward lower growth and higher inflation.” The first signs are already visible, with the European Purchasing Managers’ Index in April coming in significantly weaker and pointing to a 0.1% contraction of the European economy.

The current oil crisis exposes the EU’s structural weakness, according to Daniel Lacalle, economist and fund manager, in an opinion piece. Like Wellink, he fears misguided government interventions. Measures such as EU windfall taxes on oil companies, rationing energy consumption and suppressing demand. Lacalle argues that the EU already made the same mistakes in 2022. That year, it was favorable circumstances such as a mild winter and declining Asian energy demand that helped the EU avoid disaster. Not EU policy, although according to Lacalle it was presented that way. The Purchasing Managers’ Index also shows that the services sector has been hit hardest. The European economy relies heavily on that sector, and that is where Lacalle’s concern lies. According to the economist, the EU should not increase regulation further, but instead tackle the oil crisis through deregulation, lower taxes, faster permitting, a more realistic energy policy and a serious strategy to restore European competitiveness. Calls we have been hearing for years.

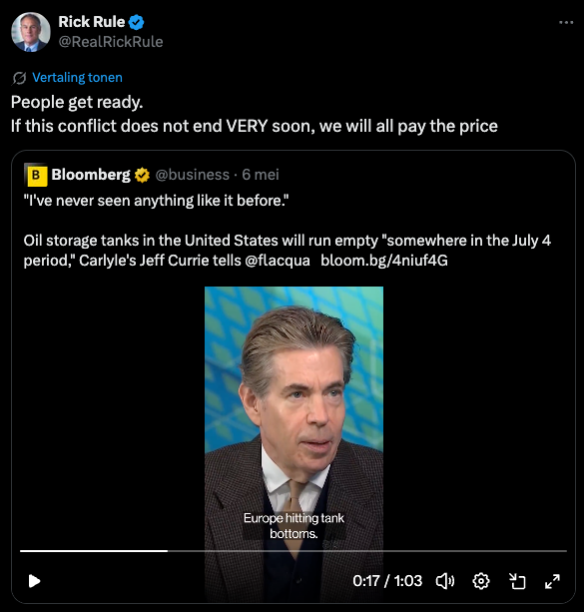

Everything revolves around oil prices. The longer the Strait of Hormuz remains closed, the longer it will take for oil prices to fall again. Added to that is the time needed to restore key infrastructure in the Gulf states. National oil reserves that countries are currently tapping to absorb the first shocks could quickly become depleted. Possibly as early as July 4 in the United States. “People, brace yourselves. If this conflict is not resolved extremely quickly, we will all pay the price,” warns Rick Rule, investment analyst and organizer of the Rule Symposium focused on commodities and gold and silver mining.

Rick Rule warns of oil shortages in the US if the Iran war is not resolved quickly, source: X.

Rick Rule warns of oil shortages in the US if the Iran war is not resolved quickly, source: X.

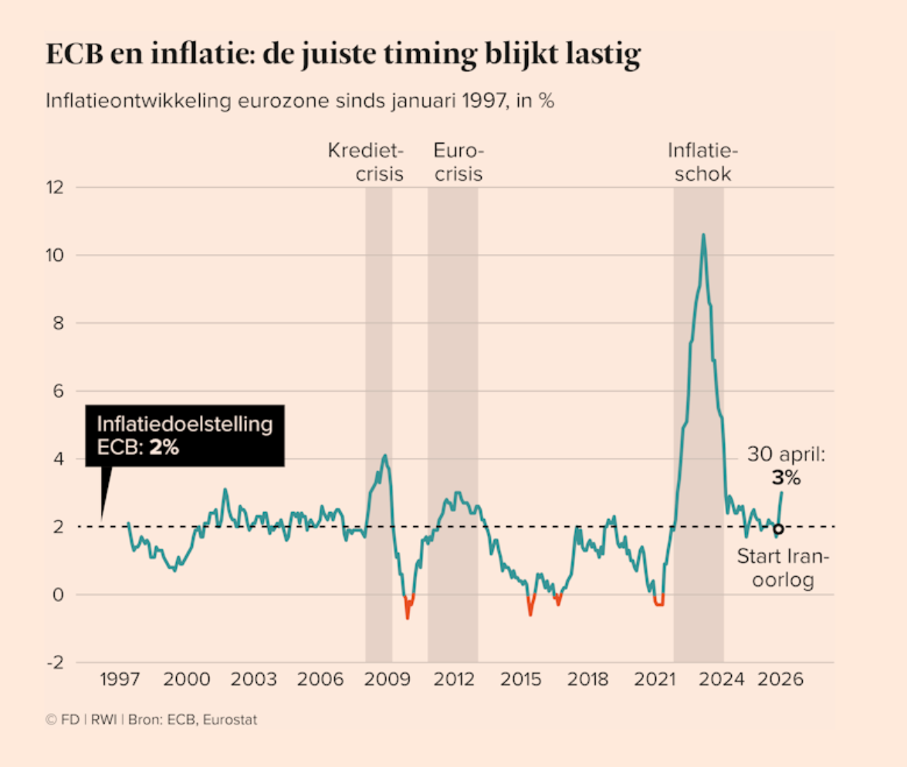

The question now is whether the ECB has learned the lessons from 2022, and whether it can raise rates quickly enough to fight inflation. It has proven difficult to bring inflation back toward the ECB’s 2% target. “Inflation was already persistent before recent geopolitical tensions pushed energy prices higher,” says investment strategist Roelof Salomons of BlackRock Netherlands: “What we are seeing now is not a temporary disruption, but a system that fundamentally operates differently. For central banks, this is an uncomfortable reality. Fighting inflation means slowing the economy. Supporting growth means tolerating inflation.”

Inflation in the eurozone (green line) versus the ECB’s 2% target, source: Financieel Dagblad.

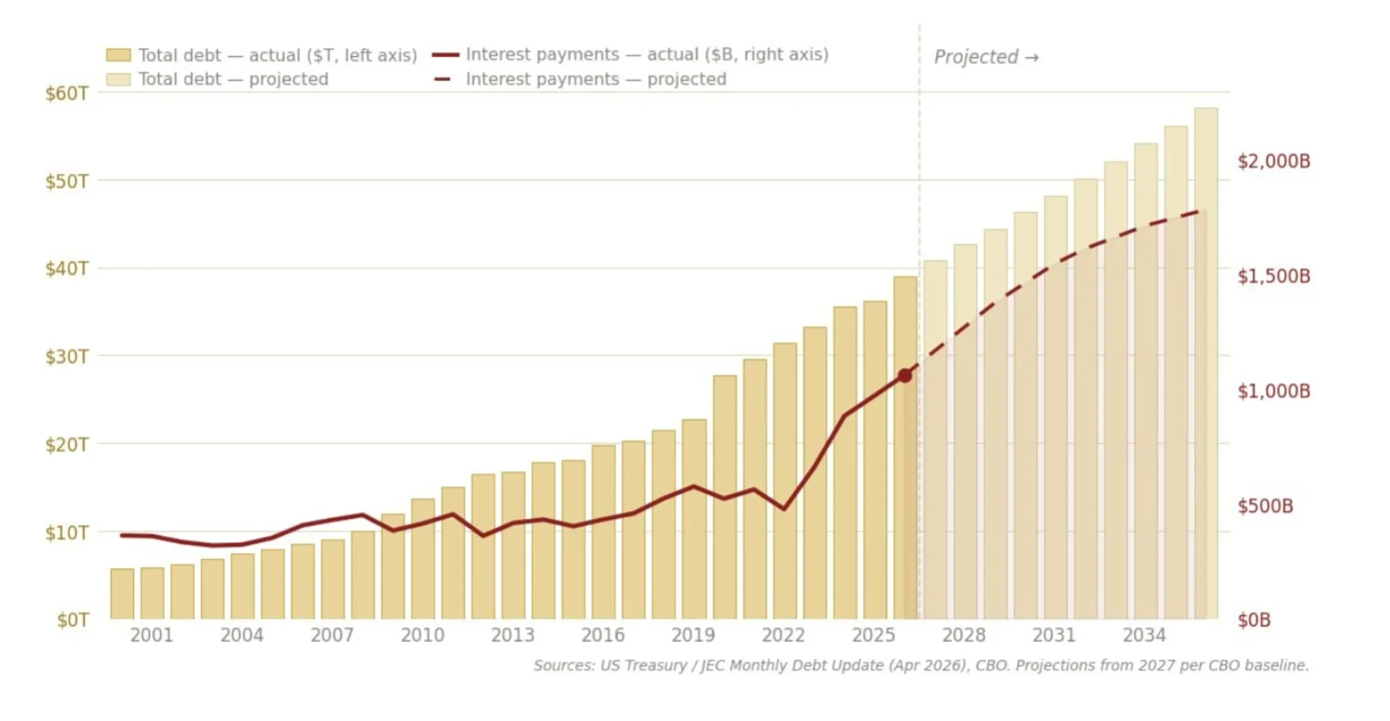

According to Nomi Prins, central banks are also struggling with interest rate policy. According to the former hedge fund employee and analyst, the Fed and ECB cannot raise rates because higher rates also mean higher costs for governments. Governments need to finance rising budget deficits by borrowing money, and this ever-growing national debt also leads to rising interest expenses.

US national debt (yellow bars) and annual interest payments on that debt (red line) through 2026 and future projections, source: Silverbullion

In the US, national debt has climbed to $39 trillion, that is 39,000,000,000,000 dollars. Annual interest costs for the US government have risen to $1 trillion, surpassing the defense budget for the first time in history, normally the largest expenditure on the US budget. The Fed (US central bank) has for some time been purchasing $40 billion in US Treasuries (government debt) per month. According to Nomi Prins, the Fed simply cannot afford to raise rates with figures like these, as doing so would saddle the US government with immense additional costs.

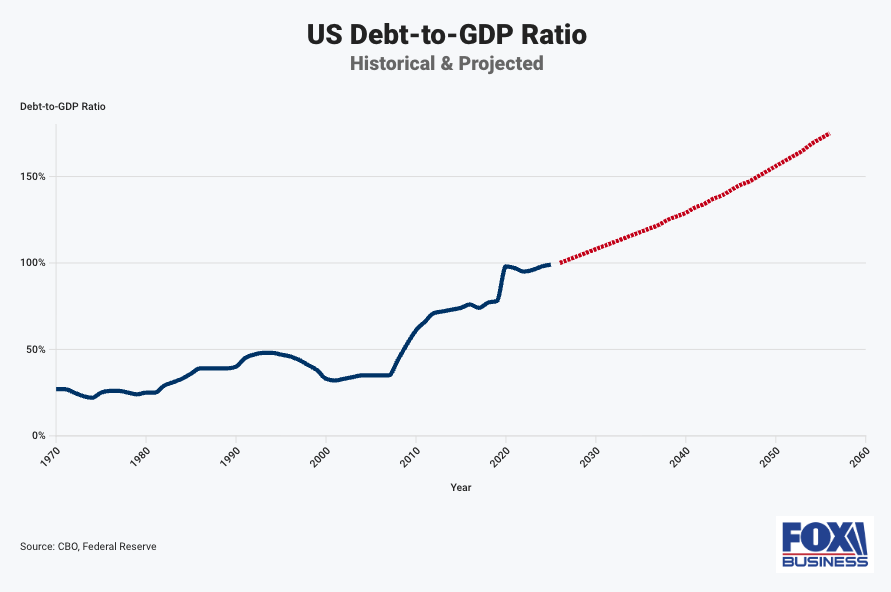

Ratio of US national debt to the American economy (GDP), source: Fox Business.

These staggering figures need to be placed in perspective. As long as the US economy grows faster than the debt burden, there is no immediate issue. Expectations, however, are unfavorable. It is projected that US national debt and the economy will become equal in size starting in 2026. Debt is expected to reach as much as 108% of the economy by 2030 and even 120% by 2036. According to many analysts, this is unsustainable and Trump appears unlikely to fulfill his earlier promises of reducing national debt.

What does this mean for gold? In the short term, we see that higher interest rates by central banks such as the Fed and ECB will put pressure on gold prices. Higher oil prices reduce the likelihood of rate cuts and make interest-bearing bonds relatively more attractive than gold. But how likely is it that central banks will actually raise rates during stagflation? Central banks can attempt to combat inflation that way, but a stagnating economy instead calls for lower rates. Jessica Tan of Silverbullion also argues that the combination of stagflation and high sovereign debt makes it especially difficult for central banks to raise rates.

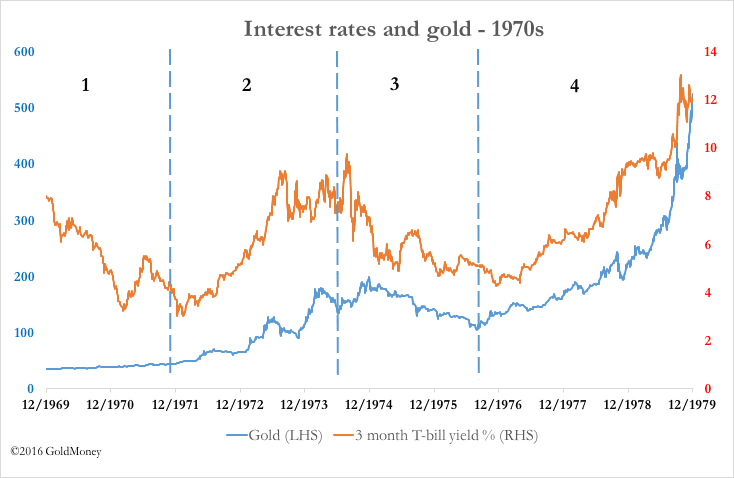

Short-term government bond yields (orange line) versus the gold price (blue line) from 1969 to 1979, source: Gold Money.

In addition, higher rates by the Fed do not automatically mean that gold prices will fall. During the major stagflation periods of the 1970s, gold actually experienced enormous price increases:

- 1971 – 1974: Gold price rose +470% during the Nixon Shock and OPEC embargo

- 1976 – 1980: Gold price rose +750% during the Iranian Revolution and the Iran-Iraq War

Whether we will see a repeat of this remains uncertain, but looming stagflation and high sovereign debt place central banks in a dilemma. While the Fed and ECB are trapped by this situation, central banks in oil-exporting countries are actually lowering rates, according to Nomi Prins: “The question is what happens when diverging monetary policies among central banks push capital away from the dollar toward assets that central banks themselves are buying. That is where strategic investors should focus their attention.”

“Central banks and governments will continue reducing their dependence on US government bonds in favor of gold,” explains Philippe Gijsels, chief investment strategist at BNP Paribas: “In an environment of structurally higher inflation, it is necessary to hold physical and scarce investments. Precious metals are clearly part of that. And once the fog surrounding the war [in Iran] clears, investors will return to the gold and silver markets.”