9.3

8.735 reviews

English

EN

Precious metal prices came under pressure this week in the run-up to several monetary policy meetings. Nevertheless, the structural factors behind the precious metals market remain intact.

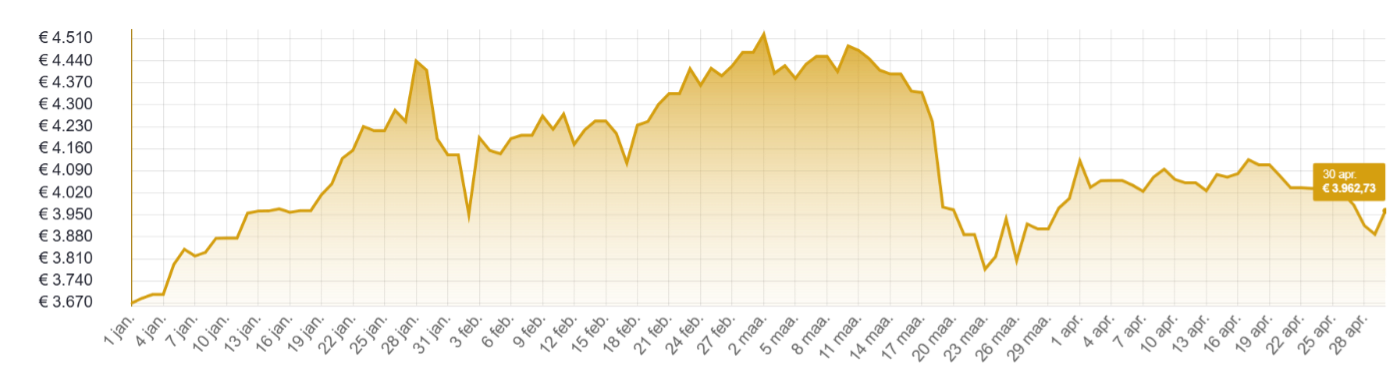

The gold price had risen again from its low on 23 March to almost $4,900, but fell back to just above the $4,500 mark. As a result, its return since the start of 2026 declined to just 5%. Silver had also climbed from just over $60 at the end of March to $82.50. The most recent correction pushed silver back to just above the $70 mark. The silver price is still trading a fraction higher than at the start of 2026.

In euros, the decline was somewhat more limited because the dollar strengthened over the past two weeks as a result of rising long-term interest rates.

Gold price since 1/1/26, in EUR per troy ounce (Source: HollandGold)

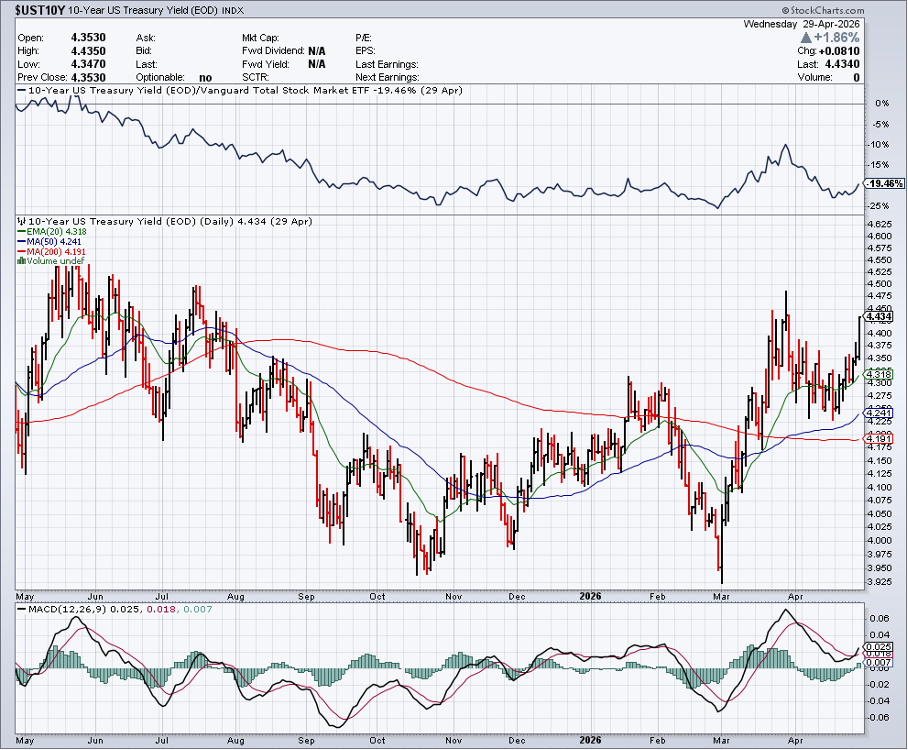

Part of the reason for the renewed pessimism can be found in rising inflationary pressure, particularly as a result of higher energy prices. In its Commodity Markets Outlook, the World Bank forecast a 24% increase in global energy prices for 2026. This is the highest figure since 2022, when Russia invaded Ukraine. Long-term interest rates have risen sharply, and that is not favourable for precious metals.

Ultimately, the Federal Reserve, the European Central Bank and the Bank of England all kept their policy rates unchanged, after which both gold and silver were able to regain some ground. Jerome Powell stated in his final meeting as chair of the Federal Reserve that the monetary committee is not in a hurry to change policy quickly.

The Fed was notably divided, however, as three of the twelve voting members objected to the hint that further rate cuts may still follow. Stephen Miran, who was nominated by Trump last year, even argued for an immediate 25-basis-point rate cut. It was the first time since 1992 that there were four dissenters on the Federal Reserve Board.

Higher inflation makes it difficult to lower interest rates, although rate hikes are not in the pipeline either given the high debt position. The Fed estimated inflation at 3.5% in March, far above its internal target of 2%. At the next monetary policy meeting, it is in principle Kevin Warsh’s turn, unless the Senate still throws a spanner in the works. The final vote is on 11 May, and the next meeting of the Fed’s monetary policy committee is scheduled for 17 June. According to the CME FedWatch Tool, no rate cut should be expected then either.

Chart: US long-term interest rate over twelve months, US 10Y Treasury yield (Source: Stockcharts.com)

Meanwhile, most major banks remain positive on gold because fundamentally nothing has changed. The structural factors, namely protection against loss of purchasing power, the process of de-dollarisation in global financial capital flows and diversification by central banks, all remain intact.

Goldman Sachs has taken a relatively cautious stance and reiterated an earlier forecast that the gold price will rise to $5,400 by the end of 2026. The American investment bank does warn of short-term risks and points to the possibility of forced liquidations of gold positions. This could happen if the bond or equity markets were to correct as a result of disruptions around Hormuz. JP Morgan maintains its target of $6,300 by the end of this year.

From a technical perspective, the 200-day exponential moving average (200d EMA) on the spot price chart is currently just above $4,300, which is a crucial technical support level. A weekly close below this threshold would put the rising long-term trend at risk.

The global silver market is heading for its sixth consecutive supply deficit in 2026. This was revealed in the Silver Survey, which is published annually by the Silver Institute. This deficit is even expected to be 15% higher than in 2025. The cumulative deficit since 2021 has now risen to 762 million troy ounces, putting above-ground inventories under increasing pressure.

On the demand side, industrial silver consumption is expected to fall by 3% in 2026. This decline is mainly due to the solar sector, which is expected to use 19% less silver this year. This can be explained by the phenomenon of ‘thrifting’, whereby the silver content in solar panels declines. No fewer solar panels are being produced than last year, but due to the sharply higher price, silver is being replaced by other metals such as copper, nickel and aluminium.

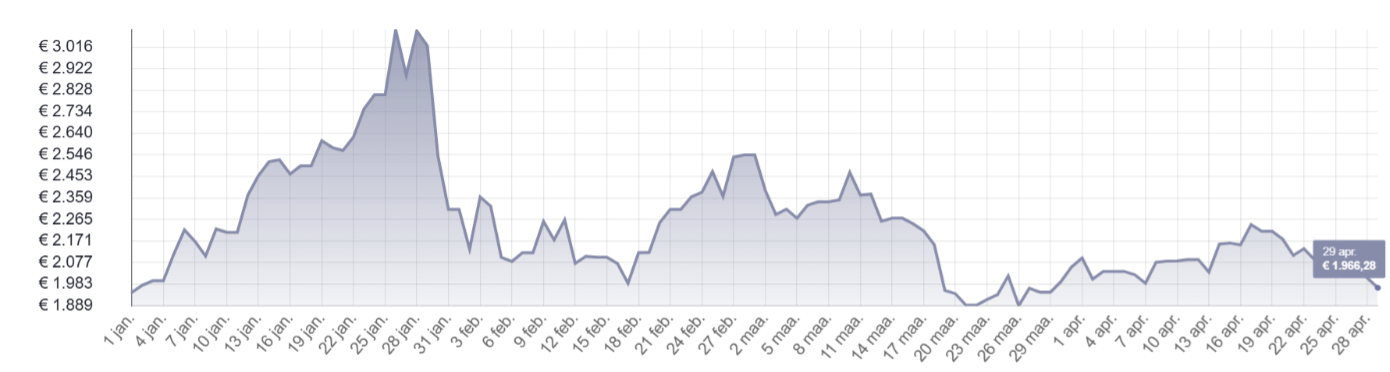

Chart: silver price since 1/1/26, in EUR per kilogram (Source: HollandGold)

This development within the solar sector is partly offset by the broader electrification trend, which requires increasing amounts of silver. In the construction of data centres, among other things, large quantities of silver are needed for servers and semiconductors. On the supply side, the amount of recycled silver will increase, but this will not be enough to restore market balance.

More important for price formation is investment demand. In 2025, inflows into physical silver ETFs reached a new record level. Assets under management in physical silver ETFs had never been this high before. Further growth is expected this year, albeit at a more moderate pace than in 2025.

Also take a look at our YouTube channel

On behalf of Holland Gold, Paul Buitink and Yael Potjer interview various economists and macroeconomic experts. The aim of the podcast is to give viewers a better understanding and a stronger footing in an increasingly fast-changing macroeconomic and monetary landscape. Click here to subscribe.