9.3

8.833 reviews

English

EN

Since the outbreak of the war in Iran, the gold price has fallen by 15%. Why is the gold price falling now of all times? However, banks are looking beyond the short-term dip in gold prices and expect higher gold prices later this year.

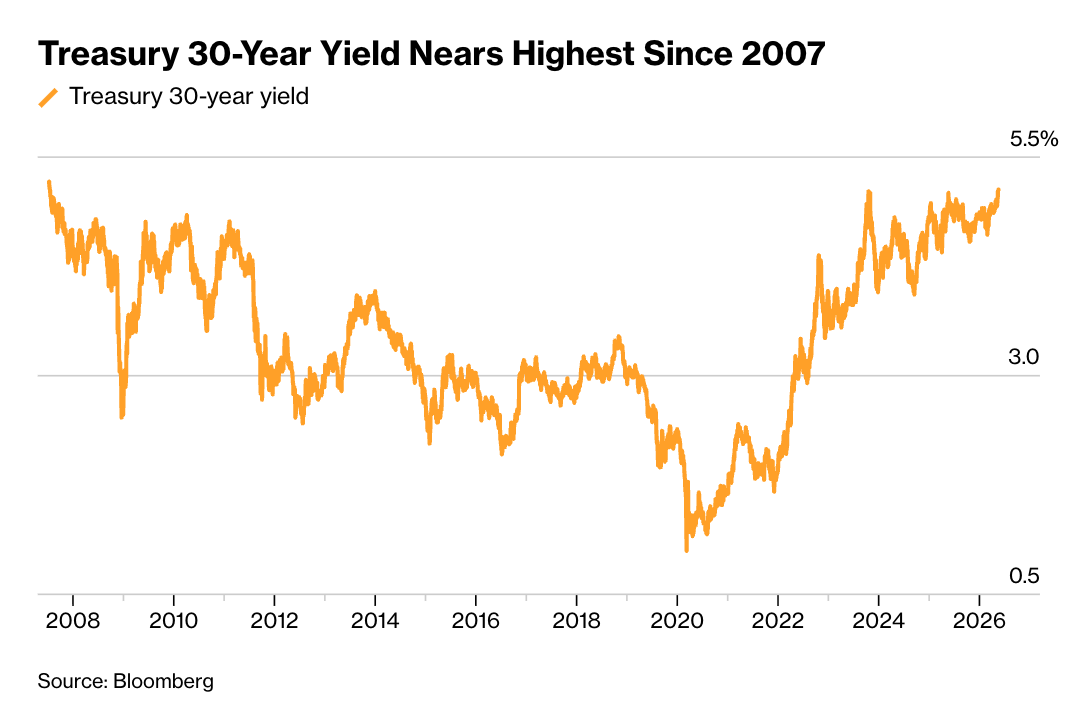

It is precisely in the market for long-term government bonds that investors are losing confidence, now that yields on 30-year US government bonds have risen to 5.2%. This is the highest level in almost 20 years. Yields on government bonds rise when demand for these bonds declines. When demand is lower, governments must offer higher interest rates to attract investors. These bonds are a crucial macroeconomic barometer and can strongly influence interest rates in other sectors, such as mortgage rates or rates on corporate loans. In last Friday’s weekly selection, we already discussed the current high interest-rate environment worldwide in more detail.

Yield on 30-year US government bonds rises to highest level since 2007 (Source: Bloomberg)

Why are investors moving away from US government bonds now, even though they normally serve as a safe haven in uncertain times? Here too, the Strait of Hormuz is the bottleneck. Uncertainty about the outcome of the war between the US and Iran means markets expect the oil crisis to last longer. This raises inflation expectations. The higher inflation is, the lower the real return investors retain on their bonds. They therefore seek compensation in the form of higher yields.

Investment strategists at Goldman Sachs, Barclays and Citigroup warn that yields could rise to 5.5%. The head of BlackRock’s research division is warning investors to stay away from these bonds for the time being. “The forces driving the bond sell-off,” says Ajay Rajadhyaksha, global head of research at Barclays, “are the deteriorating fiscal situation, high defence spending, persistent inflation and central banks that appear paralysed.”

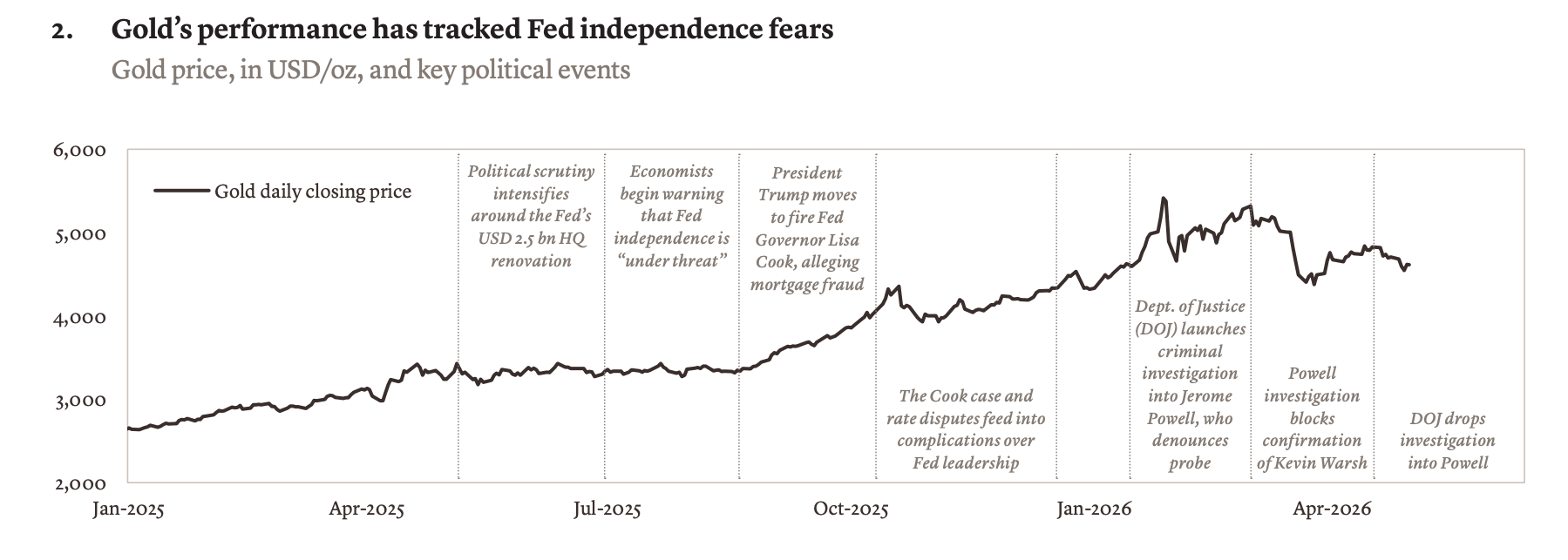

With the latter comment, he appears to be referring to the complex situation facing the Federal Reserve, the US central bank. Jerome Powell has stepped down as chair and his successor, Kevin Warsh, has been accepted by the Senate. The question now is what direction Warsh will take. In last week’s podcast, we discussed his expectations with Han de Jong. The Fed currently appears divided between the risks of high inflation, which would call for rate hikes, and forces that are instead calling for rate cuts.

Since April 2025, pressure on the Fed has steadily increased. Only recently were the lawsuits against Powell temporarily paused, which was necessary for the Senate to approve Warsh’s appointment after all. (Source: Lombard Odier)

There has been much debate surrounding his appointment, as markets previously interpreted Trump’s choice of Warsh as an attempt to put pressure on the Fed. Trump would like to see interest rates fall, while everything in the world seems to point to the need to keep rates stable or even raise them. The earlier indictments against Fed governor Lisa Cook and former chair Powell were among the factors that helped drive gold prices higher, according to Swiss bank Lombard Odier.

Normally, higher interest-rate expectations mean that gold declines, but this is not set in stone. Sometimes we first see a fall in the gold price, followed by a rise even as interest rates continue to climb. As we have already explained in previous articles, the historical relationship between interest rates and gold has broken down since 2022.

In the short term, we are indeed seeing gold correct, as shown by the 2% price decline on Tuesday, 19 May. This could mean that the gold market is shifting from a bull market to a bear market. Such a shift usually only occurs when interest rates rise as a result of economic growth and confidence in financial markets. When interest rates rise amid macroeconomic conditions marked by fiscal pressure, high government debt, rising inflation or geopolitical uncertainty, gold often recovers more quickly. The current turmoil in the bond market reflects how the oil crisis is feeding through into the financial world, with all the possible consequences that entails. This creates a murky picture that could actually benefit gold, albeit with a delay.

Development of the gold price over the past 5 years

Both Goldman Sachs and Lombard Odier expect the gold price to reach $5,400 per troy ounce over the next 12 months, compared with the current price of $4,500. That would imply a price increase of 20%. Both banks expect gold purchases by central banks to remain one of the main drivers of price development. Swiss bank Lombard Odier is looking beyond the current oil crisis and argues that gold’s structural drivers remain firmly intact. The real risk for gold lies in a structural decline in purchases by central banks and private investors, which, according to its analysis, is not currently taking place.

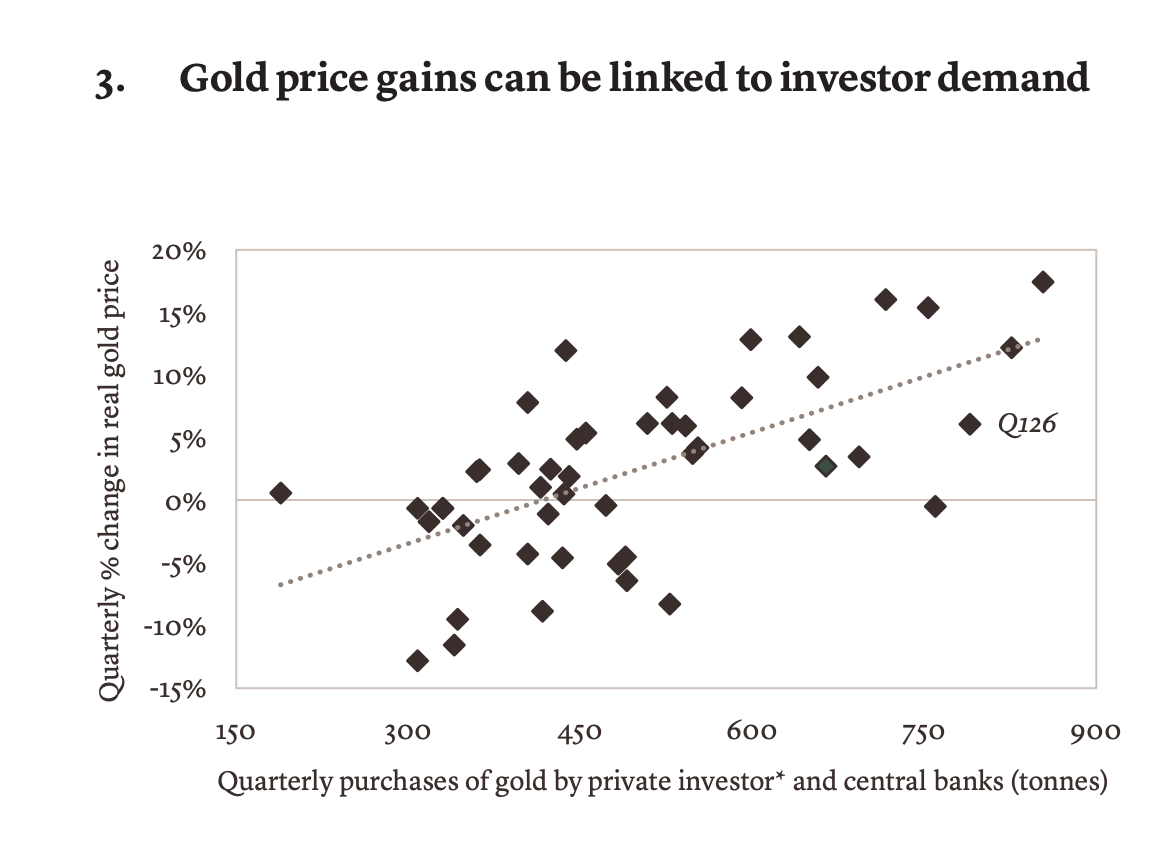

The chart above shows the correlation between quarterly gold purchases and price developments over the past ten years, with each point representing one quarter. Source: Lombard Odier

The bank sees a clear relationship between physical demand for gold and price increases in the yellow precious metal. This analysis looked at total demand from central banks and private investors. At demand of 400 tonnes of gold per quarter, the price generally remains stable. For every additional 100 tonnes, the gold price can rise by as much as 3%. While the quarterly average over the past ten years was still around 450 tonnes, this has risen to 620 tonnes since 2023. In the first quarter of 2026, demand even peaked at 790 tonnes of gold, a sharp increase driven mainly by central banks and Chinese investors.

According to these reports, the decline in gold therefore appears to be mainly a reaction to rising interest rates, rather than a deterioration in gold’s structural outlook. Banks therefore see the recent correction more as a temporary pullback.

Viewing tip: in this week’s Holland Gold podcast, Jeroen Blokland shares his view on the development of the gold price.