9.2

8.899 reviews

English

EN

Has the second wave of inflation begun? This week, the ECB raised interest rates for the first time since 2023 because of rising inflation figures. But what will the consequences be for the economy? And will the ECB ultimately simply accept higher inflation, now that EU member states already spent €358 billion on interest payments last year? That is nearly two-thirds of the new debt taken on annually.

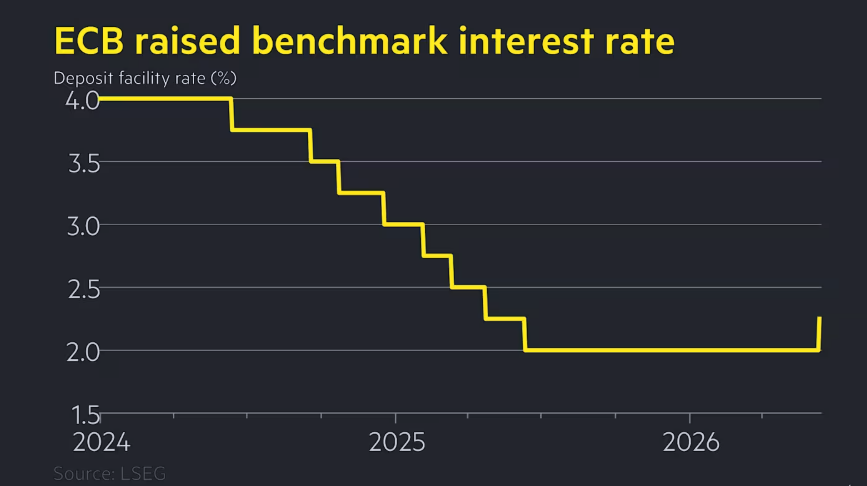

The European Central Bank (ECB) raised interest rates by a quarter percentage point to 2.25 percent on Thursday. It is the first rate hike since 2023. According to ECB President Christine Lagarde, the move is necessary because of the war in the Middle East, which is driving up energy prices and threatens to push the inflation rate further above the 2 percent target. The ECB is the first major central bank to raise interest rates because of the consequences of the conflict.

Higher interest rates make borrowing more expensive and saving more attractive. This reduces demand in the economy, which can temper upward pressure on prices and, in theory, help bring the inflation rate back down.

First ECB interest rate hike in three years (source: FT)

Lagarde said the decision to raise interest rates was “pretty obvious”. The conflict in the Middle East has caused a major energy shock, and its consequences are now beginning to feed through into the broader economy. “We are beginning to see a broadening of inflation across the economy,” Lagarde said.

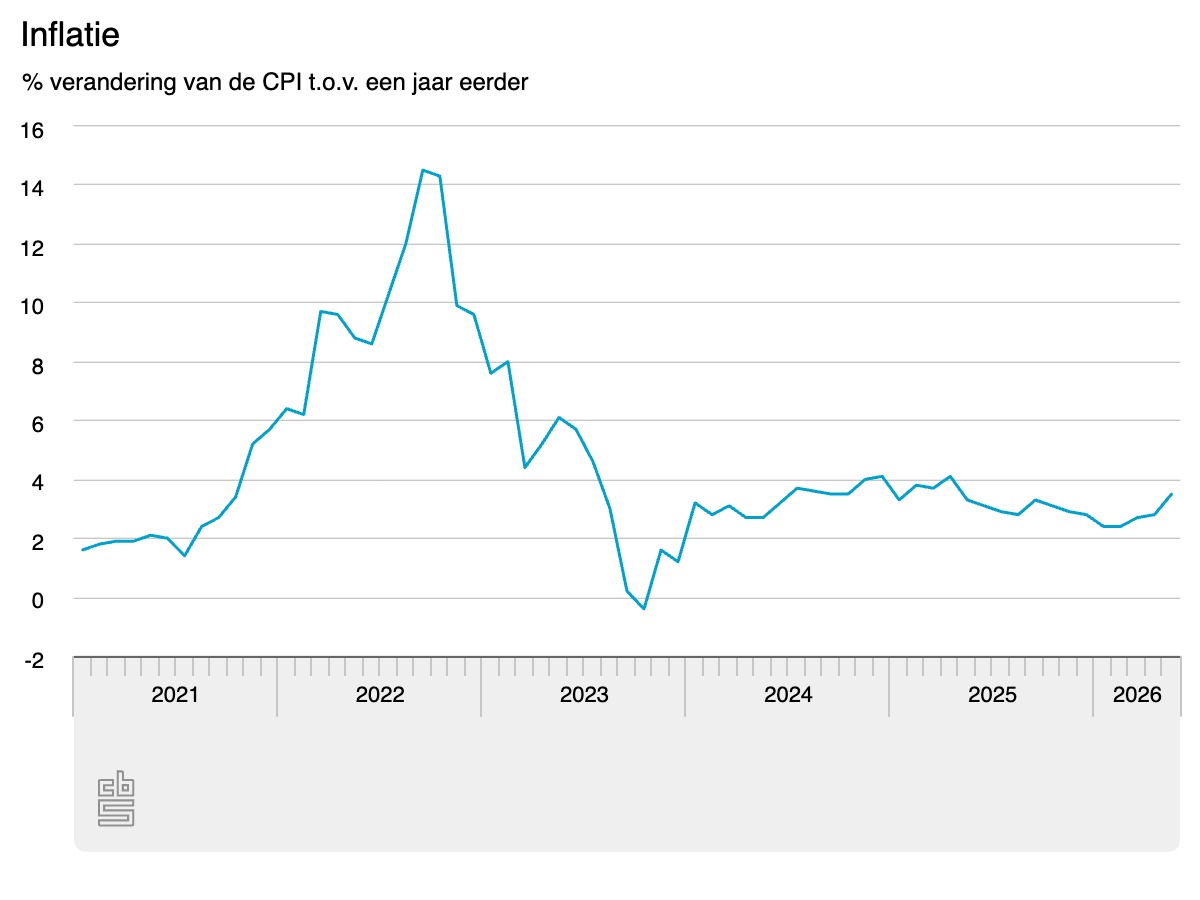

This development is also visible in the Netherlands. On Monday, CBS reported that in May 2026 consumer goods and services were 3.5 percent more expensive than a year earlier. In April, the inflation rate was still 2.8 percent. In the eurozone as a whole, inflation also rose, from 3.0 percent in April to 3.2 percent in May.

Development of CPI in the Netherlands (source: cbs.nl)

The fear is that a second wave of inflation is emerging. Higher energy and transport costs are now beginning to feed more broadly through the economy, wrote Thomas van Galen, whom you may remember from this podcast. This means that it is no longer only energy and transport prices that are rising, but that the prices of all kinds of other goods and services are also coming under upward pressure.

Van Galen sees an inflation battle emerging that has been set in motion by the energy shock. Companies are trying to protect their margins by passing higher costs on to their customers, while workers are seeking compensation for the rising cost of living through higher wages. In this way, everyone tries to pass on the bill, and inflation can become very persistent through the wage-price spiral.

Lagarde now expects total inflation in the eurozone to average 3 percent this year and to fall to 2.3 percent next year. But this forecast depends heavily on the development of oil prices. In an unfavourable scenario in which oil prices were to average above $165 per barrel in the third quarter, inflation could rise to 5.3 percent in 2027. The market expects the ECB to implement at least one more quarter-percentage-point rate hike this year.

Christine Lagarde (source: ECB)

An interest rate hike can further slow economic growth, while growth in the eurozone is already weak. Reactions to the rate decision are therefore divided.

Those who support the decision point to 2022 and hope that the ECB will not repeat the mistake it made then. In response to the war in Ukraine and the pandemic, it did not intervene forcefully enough, allowing inflation to rise into double digits. In an article by Politico, we read that economist Friedrich Heinemann praised the ECB’s move: “Faced with the trade-off between supporting growth and maintaining price stability, the Governing Council is clearly choosing price stability. That deserves praise.”

Others fear that the ECB is repeating a mistake from 2011 by tightening policy at a time when the economy is already weakening. Back then, too, the central bank raised interest rates, only to be forced into a policy U-turn a few months later when the economy slumped. “If the ECB were to go beyond the June rate hike, the eurozone could end up in an even worse position, with the risk that it even falls into an unnecessary recession,” warned Holger Schmieding, chief economist at Berenberg.

If the ECB reacts too slowly or too cautiously, there is a risk that higher energy costs will seep into inflation expectations, wage demands and broader price increases. If the central bank reacts too aggressively, it risks further slowing an already weak economy. “When I look at the ECB, it seems more concerned about a repeat of the 2022 period (an inflation wave) than, for example, a repeat of 2011,” said Paul Hollingsworth, chief economist at BNP Paribas.

ECB expectations adjusted (source: Bloomberg)

ECB officials have indicated that the next rate hike could come as soon as their next meeting in July. The market, however, expects the increase to take place only in September.

Yet there is another side to the story. Not everyone is convinced that price stability and fighting inflation are still the ECB’s highest priority. For example, Jeroen Blokland questions the independence of central banks. According to him, much of their policy today appears to be aimed not primarily at price stability, but at keeping the debt burden sustainable.

In May, we discussed this with him in our podcast. Blokland said at the time that central banks do have to raise interest rates in order to maintain their credibility. Ultimately, however, he believes it will become clear that the highest priority is not price stability, but the sustainability of debt. This may mean that central banks are eventually willing to accept a higher inflation rate.

We discuss in detail in the podcast why debt sustainability plays such an important role. To illustrate this, we can turn to an article from FAZ this week. It describes how steadily rising public debt, combined with higher interest rates, is causing interest costs to swallow up an ever-larger share of government spending. According to calculations, the member states of the European Union spent €358 billion on interest payments last year. That amount equals 62 percent, or nearly two-thirds, of the new debt taken on annually. For governments, a little inflation is therefore not unwelcome.

Be sure to also check out our YouTube channel

On behalf of Holland Gold, Paul Buitink and Yael Potjer interview various economists and macroeconomic experts. The aim of the podcast is to give viewers a clearer picture and guidance in an increasingly fast-changing macroeconomic and monetary landscape. Click here to subscribe.