9.3

8.887 reviews

English

EN

This article has been automatically translated from Dutch. Click here to see the orginal article including all links to sources.

It will hardly have escaped your notice: precious metals continue to rise and keep breaking records—again this week. How is it that all precious metals are rising simultaneously? And what are the biggest market risks in the year ahead?

The silver price broke new records and climbed above $66 per ounce for the first time, delivering an exceptional year-to-date return of more than 125 percent. Silver is also performing strongly in euro terms: this week, more than €1,800 was paid for a kilogram of silver for the first time, a doubling since the beginning of the year.

Gold approached $4,400 per troy ounce for the first time, representing a return of roughly 65 percent in dollar terms this year. In euros, the gold price is once again nearing €120,000 per kilogram, equivalent to a return of approximately 45 percent.

Platinum prices rose this week to their highest level in 17 years in dollar terms, according to Bloomberg. An ounce of platinum now costs more than $1,900—more than double its level at the start of the year. This brings the platinum price in dollars close to its 2008 peak, when prices remained just below $2,100. In euro terms, that peak has already been surpassed.

Bloomberg points to increasing tightness in the platinum market and sharply rising trading activity in China. Silver and gold are also being driven by specific factors unique to each metal. But what overarching force explains why all precious metals have risen so exceptionally strongly this year?

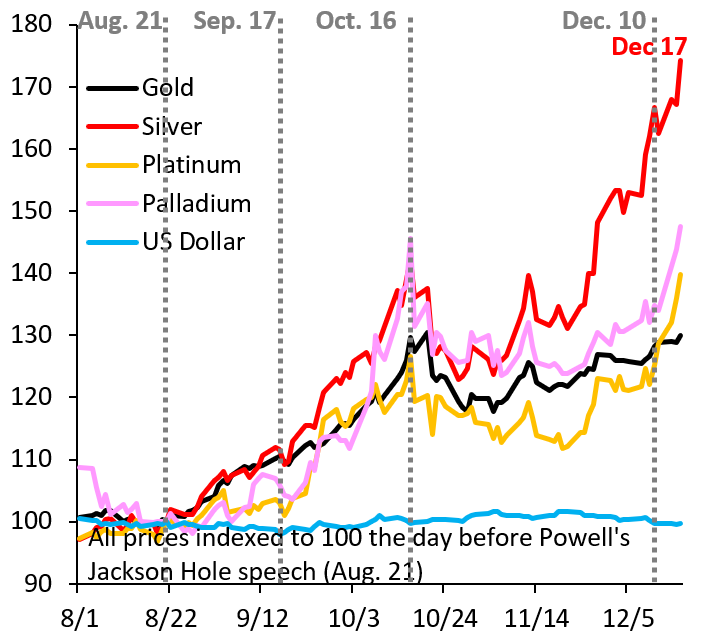

According to prominent economist Robin Brooks, the answer is clear: markets are fleeing fiat currencies and seeking refuge in precious metals. Brooks sees Jerome Powell’s speech at Jackson Hole on August 22 as a key turning point. With that speech, the Federal Reserve effectively gave the green light for further monetary easing.

According to Brooks, investors are seeking safe havens that offer protection against debt monetization—the financing of government debt through money creation—and inflation. Last week’s interest rate cut poured further fuel on the fire, as shown in the chart below.

Precious metals and the dollar (Source: Robin Brooks)

In the chart above, the blue line represents the dollar, measured by a trade-weighted dollar index against other G10 currencies such as the euro, Swiss franc, Japanese yen, and British pound. The fact that this line remains largely flat, according to Brooks, shows that this is not merely about declining confidence in the dollar, but about a broader loss of confidence in fiat currencies as a whole.

Brooks issues a warning to policymakers and politicians: “For all policymakers who think that more debt is the answer to every problem, this chart is the ultimate wake-up call. You may believe that more debt is the solution, but investors no longer do. Markets are exiting fiat currencies and shifting toward precious metals.”

At the same time, his choice of words also appears to caution investors, given the exceptionally rapid price increases of recent months. Brooks refers to a “crazy rally” and points to the risk of a bubble. At the same time, he notes that the precious-metals rally could continue further for now.

Albert Edwards of Société Générale is outspokenly positive on precious metals. According to him, there is no bubble and we are still only at the beginning of the rise in the gold price. He argues that investors are simply anticipating further quantitative easing and yield-curve control. Edwards points out that typical signs of a bubble are absent: banks remain cautious with price targets, and speculators are primarily focused on crypto.

In this week’s podcast, Jeroen Blokland also addresses this issue. He sees central banks creating conditions under which inflation could suddenly accelerate again. He considers a second wave of inflation possible and expects that prices of inflation-sensitive assets, such as precious metals, would be the first to rise in such a scenario. Watch the conversation here.

Not entirely coincidentally, a video of Ray Dalio from earlier this year circulated widely on social media this week, in which he warned of a breakdown of the monetary order, partly as a result of the enormous global debt burden. A recommended watch and read.

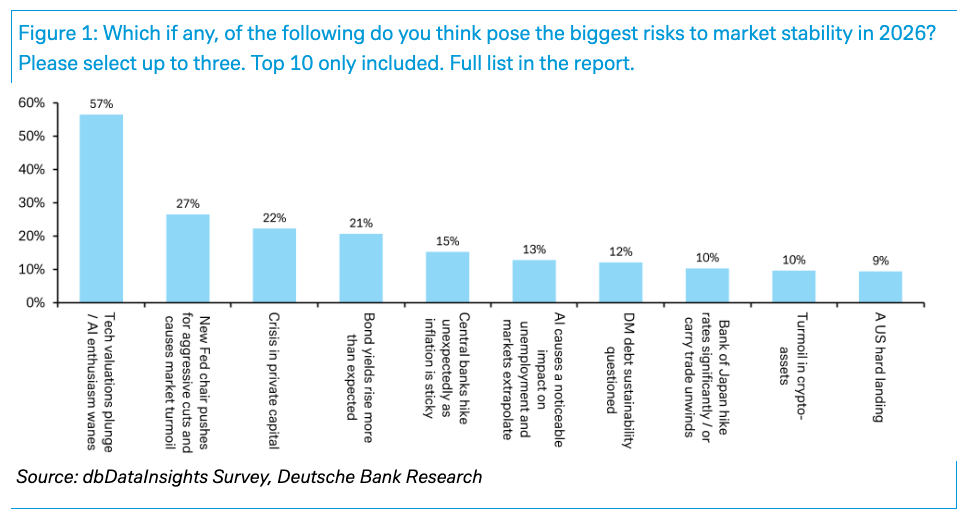

What are the biggest market risks for the coming year? Deutsche Bank put this question to 440 asset managers, and the outcome is striking. The bank notes that it has never before seen one risk stand out so clearly above the rest.

The biggest risks in 2026 (Source: Deutsche Bank)

According to 57 percent of participating asset managers, the bursting of the AI and technology bubble represents the single largest market risk for 2026. In second place, with 27 percent, is the risk that a new Fed chair will pursue aggressive interest-rate cuts. We discussed this in detail in last week’s selection. Rising interest rates, inflation, and debt sustainability—topics we regularly address—also rank high on the list. In last year’s survey, a global trade war topped the list at 39 percent, with the technology bubble in second place at 36 percent.

MarketWatch notes that it may be even more striking what these professional investors are not worried about. The risk of a global trade war has fallen to just 3 percent. An escalation of tensions in the Middle East is cited by only 1 percent, while geopolitical tensions around Taiwan come in at 5 percent. A major political or financial crisis in France also ranks surprisingly low on the risk list.

Anyone who speaks about risk is inevitably also speaking about returns. According to the survey, the average expected return for the S&P 500 in 2026 is 6.9 percent. By comparison, returns achieved so far in 2025 are around 15 percent.