9.3

8.775 reviews

English

EN

Europe is heading towards a new energy crisis. As we have written in recent weeks, the war in Iran is currently decisive, not only for precious metals but for the global economy as a whole. The key factor in this is energy. Is a rapid recovery in energy prices realistic, or are we entering a prolonged period of scarcity? And what will happen to the gold price?

There is ample room for the war with Iran to escalate, but no clear path to ending it, writes the influential British weekly The Economist. According to the magazine, Iran has launched an energy war against the global economy, hoping to force the United States to halt its air campaign and deter future similar attacks.

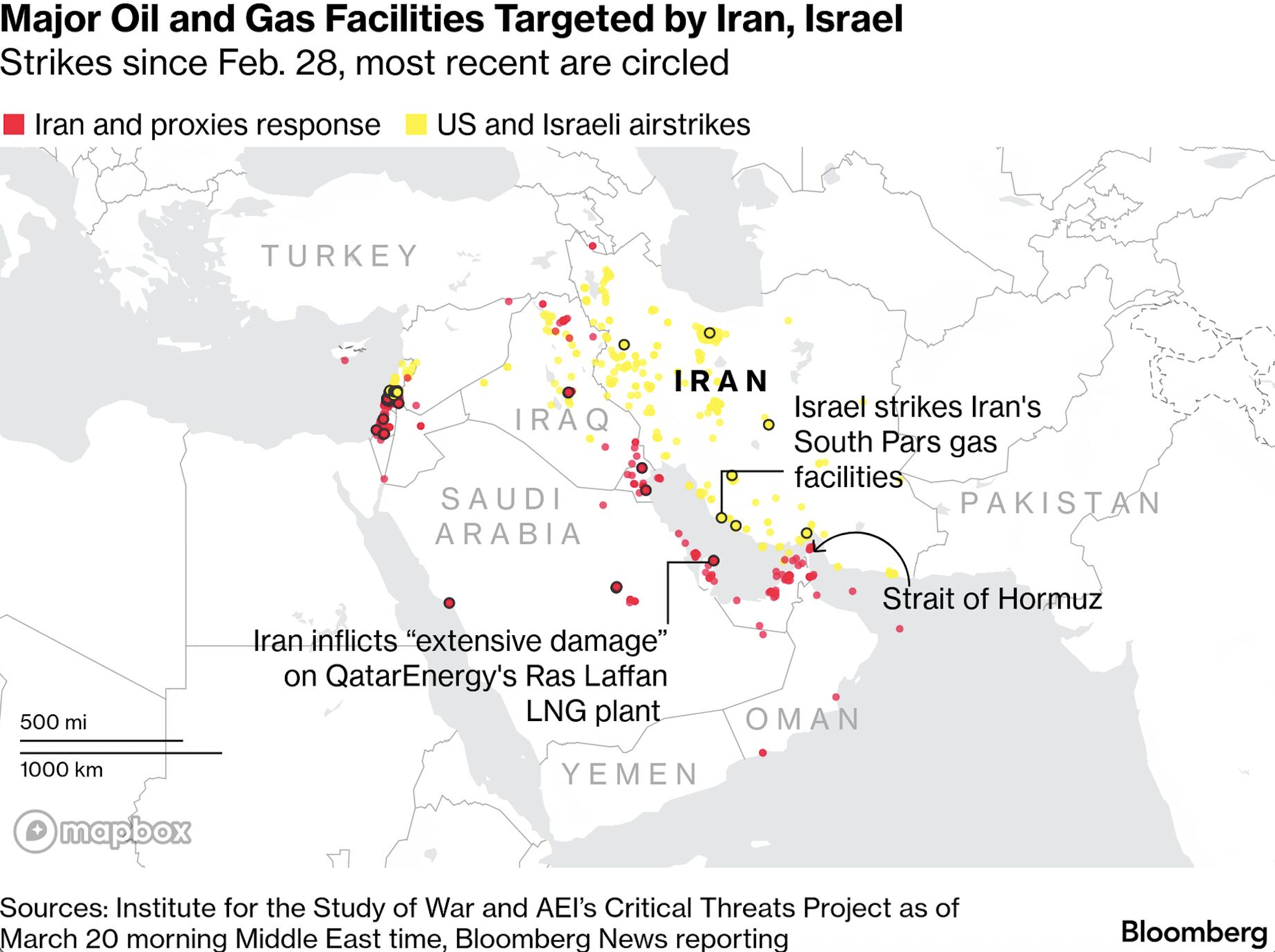

Overview of attacks in the Iran war (source: Bloomberg)

So far, this appears to be bringing Israel, the United States and the Gulf states closer together, with a growing consensus that the regime must be removed. Attacks on energy infrastructure in the region increase the likelihood that other countries will become involved in the conflict. Saudi Foreign Minister Prince Faisal bin Farhan Al Saud warned on Thursday that the kingdom’s restraint is not “unlimited” and that military intervention remains a possibility.

Some of the oil from the Gulf states still flows through two pipelines that bypass the Strait of Hormuz. The Saudi pipeline can transport up to 7 million barrels per day to ports on the Red Sea, while the UAE pipeline carries roughly half that amount. This week, Iran launched dozens of drones at Saudi oil fields and also struck energy facilities in the UAE and Qatar. Iran is therefore not only targeting shipping, but increasingly the sources of energy supply themselves. In addition, shipping in the Red Sea could once again, as in 2024, be severely disrupted by attacks from the Houthis in Yemen, an Iran-backed militia.

Breaking the blockade of the Strait of Hormuz, which at its narrowest point is approximately 33 kilometers wide, is particularly difficult. Even outside the strait, vessels remain within range of Iranian drones and missiles. Naval ships have only seconds to respond to an attack, while securing the coastline with troops does not appear to be a realistic option due to the scale required. Moreover, Iran can easily continue launching attacks from inland.

According to The Economist, Trump could therefore shift his focus to Kharg Island, where around 90% of Iran’s oil exports are loaded onto tankers. Capturing this island appears feasible and could be used as leverage against Iran. In such a scenario, oil prices are likely to rise further, both due to the loss of supply, as Iran still exports around 1 million barrels per day to China, and the prospect of a prolonged conflict.

Even if a ceasefire were reached tomorrow and the Strait of Hormuz reopened, oil prices would remain elevated due to infrastructure damage and the shutdown of oil production, says Ole Hansen, Head of Commodity Strategy at Saxo Bank. And it is not just oil: this week Iran damaged a crucial gas facility in Qatar. According to Saad al-Kaabi of QatarEnergy, it will take three to five years to repair the damage.

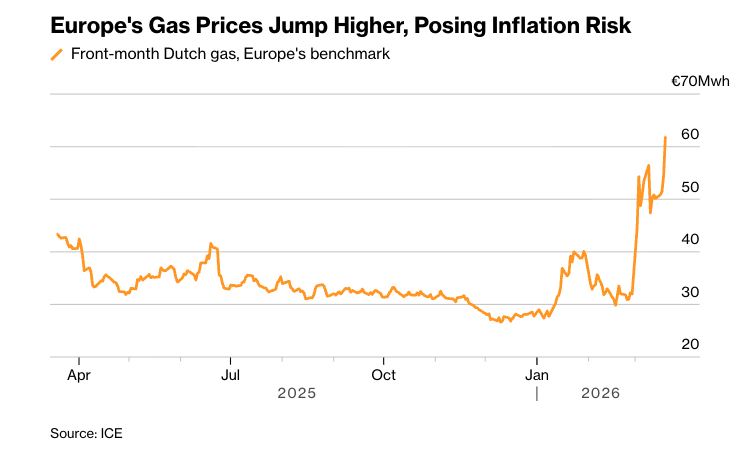

European gas prices are rising (source: Bloomberg)

In an opinion piece in the Financial Times, Michael Stoppard, a prominent gas strategist and former Chief Strategist for Global Gas at S&P Global, argues that Europe must now prepare for a prolonged energy shock. According to Stoppard, the severity of the energy crisis is still being underestimated and we should prepare for the worst. He emphasizes that managing demand will be crucial, as governments cannot quickly increase supply in the short term.

The International Energy Agency (IEA) also warns of a global energy crisis and calls for demand reduction. The IEA recommends measures such as lowering speed limits and implementing license plate restrictions so that not all cars are allowed on the road at the same time.

The ECB warns of rising inflation and states that Europeans will feel the impact in their wallets this year. Inflation in the eurozone is expected to rise to 2.6 percent, up from an earlier forecast of 1.9 percent. At the same time, economic growth will slow as households are forced to spend a larger share of their income on essential costs such as energy. The longer the conflict persists, the greater the risk of stagflation, as we already noted in the March 6 weekly selection.

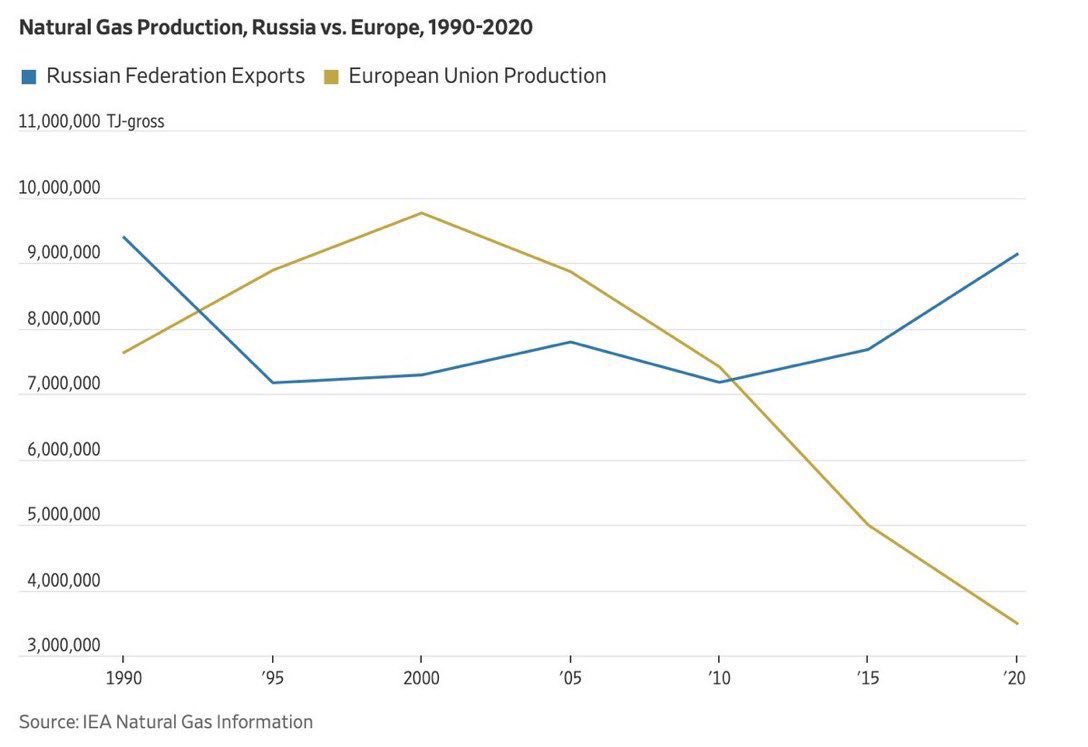

EU gas production vs. Russian gas exports (source: Michael Arouet)

EU gas production vs. Russian gas exports (source: Michael Arouet)

The EU is vulnerable due to its heavy dependence on energy imports. This is partly the result of the closure of German nuclear power plants and the reduction of domestic gas production, for example in Groningen. European, and particularly Dutch gas storage levels, are low and must soon be replenished ahead of next winter, precisely at a time when the energy market is highly disrupted.

In a widely shared video, Putin sharply criticizes European leaders in this context. According to him, Europe lacks “brains,” not due to a lack of intelligence, but because economic decisions are being made by politicians disconnected from economic reality.

Politico is also critical of EU leaders, describing them as “incapable of action.” The outlet portrays a picture of inaction, internal division, and largely empty rhetoric. At the same time, according to Politico, there was ample time to discuss climate policy, including the ETS (Emissions Trading System), under which companies must pay for their CO₂ emissions through tradable allowances.

Hungarian Prime Minister Viktor Orbán sharply criticized European policy. “The behavior and strategy of Europe are simply insane,” he said, adding that the EU must buy Russian oil to “survive.” Orbán is currently blocking a €90 billion EU loan to Ukraine with his veto, due to a dispute over a damaged pipeline for Russian oil.

The wars in Ukraine and Iran thus appear to be converging. According to Orbán, Europe cannot do without cheap Russian energy in this crisis. He is supported by Belgian Prime Minister Bart De Wever: “We must normalize relations with Russia and regain access to cheap energy. That is simply common sense.” He advocates ending the conflict with Russia in Europe’s interest, without being naïve about Putin. The Germans appear to take a different view.

In last week’s weekly selection, we concluded based on statements from various experts that the gold price could still face short-term headwinds. As you have seen, this indeed occurred this week. Over the longer term, however, gold is expected to maintain strong support.

Economist Daniel Lacalle appears to agree and writes: “A decline in the gold price based on fears that central banks will raise rates and sell reserves is based on a misunderstanding of how the monetary system works. A fall in gold due to fears of a recession is even less justified. Any response to current risks will involve more money creation, not tighter monetary policy.”

Also Jeroen Blokland reaches a similar conclusion. European countries are likely to subsidize energy costs while already facing structural budget deficits. Taxes will therefore rise, meaning households will ultimately pay for these subsidies themselves. In the longer term, central banks will be forced to absorb the additional debt and expand the money supply. Von der Leyen has already called for such subsidies. He therefore expects the gold price to rise further. To be continued!

Also take a look at our YouTube channel

On behalf of Holland Gold, Paul Buitink and Yael Potjer interview economists and macro experts. The aim of the podcast is to provide viewers with better insight and guidance in an increasingly fast-changing macroeconomic and monetary landscape. Click here to subscribe.