9.3

8.833 reviews

English

EN

After the strong rise in the gold price in recent years, we have seen a sharp correction in the gold market in recent months. Is this the beginning of the end, or merely a pause within a larger bull market? This week saw the publication of the new edition of the annual and leading In Gold We Trust Report. This report, running to more than 460 pages, is perhaps the most important publication in the gold industry. We summarize some of its key findings for you.

The title of the report, Back to the Monetary Future, says a great deal about the development gold has undergone in recent years. According to the authors, there is a growing erosion of trust in the political and monetary system. That trust, they argue, is precisely the foundation of every monetary system.

In this context, they refer to Ludwig von Mises, who argued that trust is the invisible infrastructure of every monetary system. Once citizens no longer consider the promises of the state, including the stability of money’s value, to be credible, they hold paper money for shorter periods, seek refuge in tangible assets and demand higher risk premiums.

According to the authors, gold is therefore once again gaining a more prominent role within the monetary system. As they themselves put it: “Trust, in our view, is currently being repriced, and the market is rendering its verdict in ounces.”

An important shift behind this development, according to the authors, is the erosion of Pax Americana: the political, military, economic and, above all, monetary order that has shaped the global system since 1945. According to Stöferle and Valek, that era is drawing to a close. As a result, the dominant role of the dollar is coming under increasing pressure, while gold is gaining importance as a neutral asset outside the Western financial system.

According to the authors, we are currently in a transitional phase. The old world order is losing cohesion, while a new order has not yet clearly taken shape. This order was based on free trade, free movement of capital and globally integrated supply chains, within a framework of American hegemony.

The transitional phase we are now in is characterized by heightened volatility, geopolitical tensions and a shift toward what is known as hard power. By this, they mean tangible strategic instruments of power such as energy, metals, semiconductors and military equipment.

According to the authors, geopolitical tensions feed directly into inflation, but domestic tensions can also contribute to a new wave of inflation. Persistent inflation often arises in periods of ideological struggle and eroding consensus. The central question is often who should foot the bill for higher costs, rising debts and economic headwinds. If there is no broadly supported answer to that question, inflation often becomes the way out: the pain is spread across everyone through currency debasement.

As a result, the independence of central banks is coming under increasing pressure. Fiscal and monetary policy are becoming ever more closely intertwined. According to the authors, this further erodes trust in institutions. It is precisely then that the need arises for new, or indeed proven, monetary anchors. Gold, they argue, can once again take on that role.

In a world of high debt, tight budgets and declining trust in the dollar, gold can once again take on an active role on the balance sheets of states and central banks. According to the authors, gold reserves could be revalued. They therefore see the accumulation of gold by central banks in Asia and the Middle East not merely as diversification, but as a strategic positioning race. Countries with large gold reserves would be in a stronger position if gold were ever to play a larger role in a new monetary system.

The spectacular gold rally of recent quarters was driven, according to the authors, by the continued appetite for gold among countries outside the Western sphere of influence, such as China and India, and by declining trust in the international order.

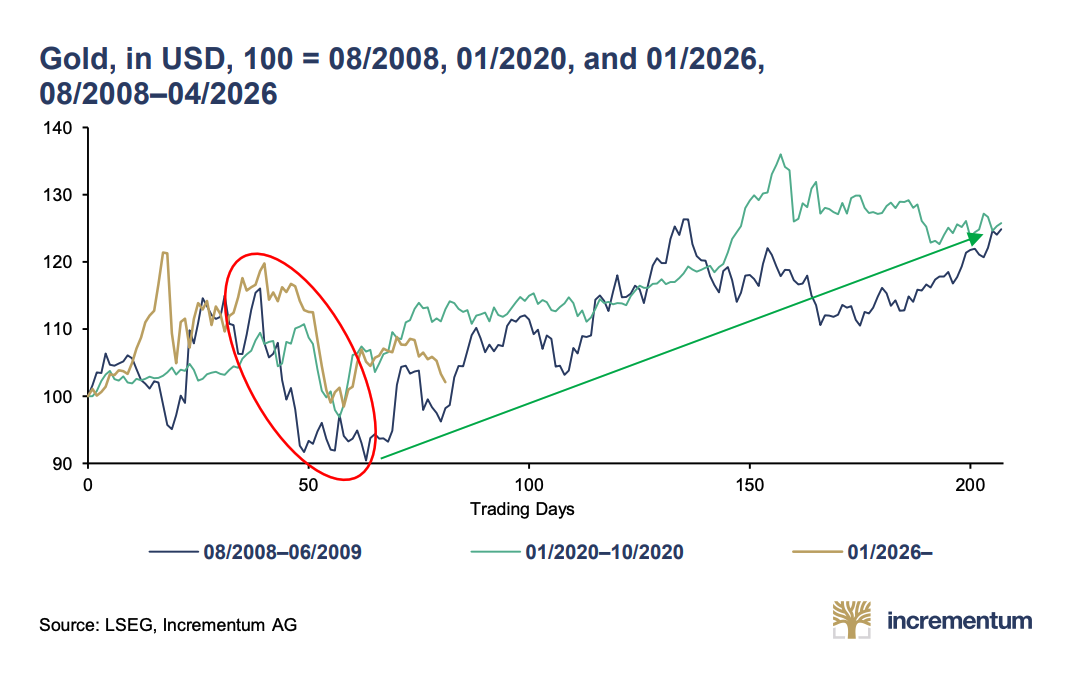

At the same time, a consolidation phase was, in their view, not only likely but even necessary from a technical perspective. The war in the Middle East did not become a new catalyst for further price increases, but rather the trigger for a healthy correction. After all, no chart in a bull market moves upward in a straight line.

Gold was sold in March because of its high liquidity. Various market participants needed cash quickly. This was partly because the closure of the Strait of Hormuz cut off cash flows to oil producers in the Gulf region, who had been reinvesting their dollar surpluses in gold for years. In addition, the escalation led to a wave of deleveraging, as rising bond yields, increasing interest rate expectations and a stronger dollar triggered margin calls.

A correction during a gold rally is common (source: IGWT)

We saw this pattern before in October 2008, when gold fell by 29% after the collapse of Lehman Brothers triggered margin calls across virtually all asset classes. A more recent example is March 2020, when a wave of liquidation swept through markets in the early stages of the coronavirus pandemic and gold fell by 12%.

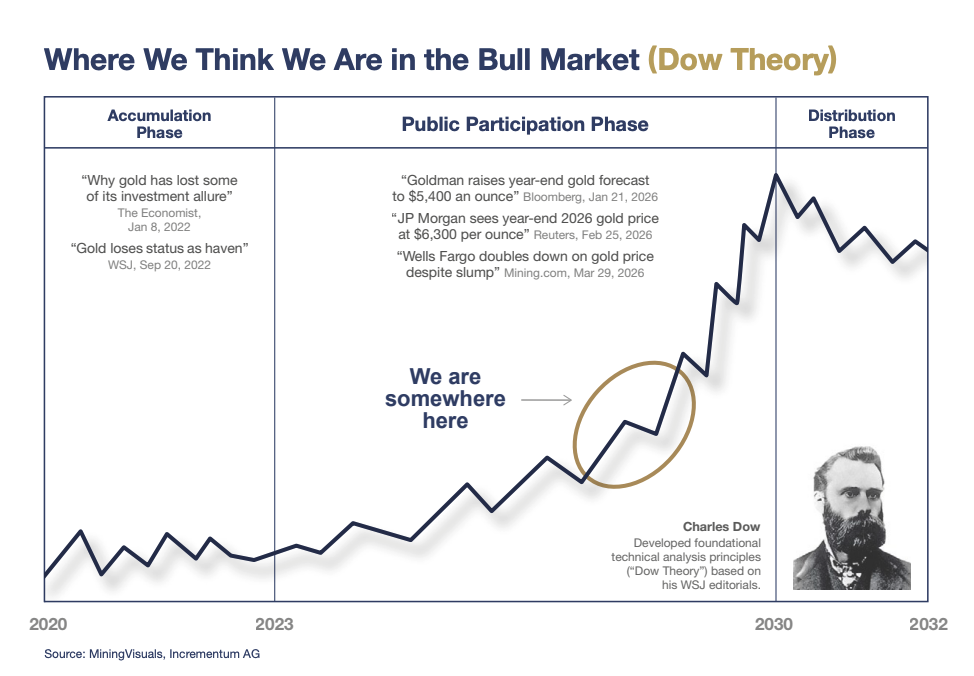

Those corrections did not mark the end of the gold rally, but rather the beginning of the next upward phase. According to the authors, this is because policymakers tend to respond to crises in the same way every time: with stimulus and additional liquidity. They expect central banks and governments to ultimately resort to such measures again this time.

This is in line with what economist Han de Jong said in our podcast this month. According to him, governments will ultimately take on more debt and we can expect a new wave of inflation. Jeroen Blokland also indicated in our podcast this week that he expects more inflation and money creation. In his view, this will ultimately cause the gold price to rise again.

This is in line with what economist Han de Jong said in our podcast this month. According to him, governments will ultimately take on more debt and we can expect a new wave of inflation. Jeroen Blokland also indicated in our podcast this week that he expects more inflation and money creation. In his view, this will ultimately cause the gold price to rise again.

According to the authors, we are therefore not in a gold bubble, but can instead expect a further rise in the gold price: “Gold is anything but a crowded trade. On the contrary: it is a party where the first guests are just starting to arrive.”

Read the full IGWT report here.

Be sure to take a look at our YouTube channel

On behalf of Holland Gold, Paul Buitink and Yael Potjer interview various economists and macroeconomic experts. The purpose of the podcast is to give viewers a better understanding and more guidance in an increasingly fast-changing macroeconomic and monetary landscape. Click here to subscribe.