9.3

8.887 reviews

English

EN

At the beginning of this year, financial markets resembled a bubble in search of a pin. The Iran crisis has become the pin that bursts that bubble. But what does this mean for investors in precious metals?

At the start of the year, precious metal prices were still rising almost vertically. Global equity markets were hitting record highs, both in Europe and in Asia. Japan’s Nikkei and South Korea’s Kospi attracted many investors during a rapidly rising phase. The sky was the limit. President Trump confidently stated in early February that the U.S. Dow Jones index, after reaching the 50,000-point milestone, would double again over the next three years. Non-listed investments in private equity and private credit also saw a massive influx of new investors over the past year. At the beginning of this year, institutional fund managers held the lowest cash positions in the past 25 years!

It was as if almost everyone believed that financial markets could no longer fall, whether in gold, Korean equities or private equity. But when nearly all experts and forecasts agree on the direction of the market, something else tends to happen. That is one of Bob Farrell’s famous market rules.

And so something else has indeed happened. The war with Iran has forced investors worldwide to reassess and rebalance their portfolios. The core problem was that too many investors held too little cash and too few liquid positions. I warned about this issue earlier in the Holland Gold podcast of February 5. In such a situation, investors are forced to sell in a declining market to rebuild cash levels, a self-reinforcing process that creates a vicious cycle.

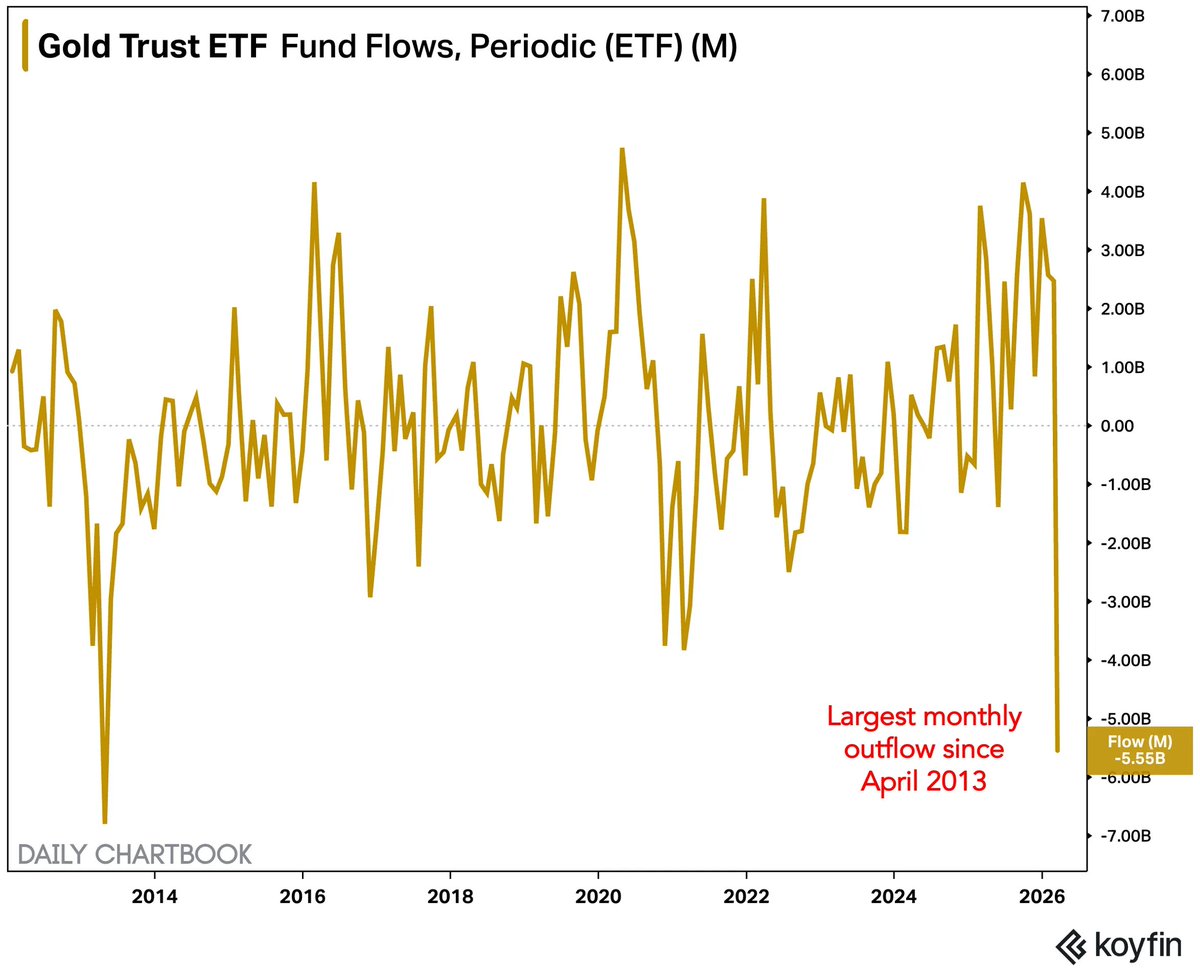

Many investors find it counterintuitive that the gold price declines during a geopolitical event such as the Iran war, and they sometimes struggle to understand who is selling gold. Yet the world’s largest gold ETF, the SPDR Gold Trust, saw its largest outflow of assets since April 2013. (April 2013 was also one of the worst months ever for gold. Prices continued to weaken for the remainder of that year.)

Monthly inflows and outflows of the SPDR Gold Trust ETF (Source: Koyfin)

Monthly inflows and outflows of the SPDR Gold Trust ETF (Source: Koyfin)

Investors are selling gold for several reasons. As Yael Potjer recently wrote, this is because investors expect rising interest rates and because precious metal positions are being sold due to liquidity constraints and the need to increase cash positions. Another factor is the strength of the dollar. During market panic, a flight to liquidity often means a flight into the dollar. Gold is typically negatively correlated with the dollar and therefore weakens when the U.S. currency strengthens.

A second market rule is that extreme movements in one direction tend to be followed by extreme movements in the opposite direction. In December and January, precious metals such as gold, silver and platinum moved sharply higher. Strong corrections as counter-movements are therefore logical, like a pendulum that swings too far to one side before moving back in the opposite direction.

The gold and silver markets experienced another flash crash on Monday morning, March 23, with gold briefly falling to $4,100 per ounce and silver briefly touching $61 per ounce. Both metals are still trading above their technical 200-day averages, which stand at $4,075 for gold and $56 for silver respectively. The possibility remains that these levels will be tested again in the future. The platinum price also weakened, falling to between $1,800 and $1,900. It is notable that platinum is not declining more than gold in the current volatility.

What should precious metals investors do now? First and foremost: do not panic and do not hit the sell button during one of these heavy waves of selling. If necessary, wait for a price recovery—such as the one seen at the end of February—if you believe your precious metals position has become too large and you wish to reduce it. Positive news about a ceasefire in the Middle East could quickly trigger a recovery phase.

The arguments for investing in precious metals over the long term remain more valid than ever. The debasement trend and the growing debt burdens have not suddenly disappeared. Investing in gold is also a way to hedge against poor government policy. And there has been no shortage of that in recent years. The Iran crisis once again exposes several painful policy failures. In the United States, one may question whether starting this war was a wise decision. In Europe, it is once again clear that it was poor governance to tie energy dependence first to Russia, then to the Middle East, and now to the U.S.

The declining gold price has also put pressure on gold mining stocks. The GDX gold miners index has fallen 30% from its peak. Combined with lower gold prices, higher energy costs (a key input for mining operations) will also weigh on profit margins. The BPGDM sentiment index for gold mining stocks has dropped in a short period to one of its lowest levels since 2020. This is comparable to the level seen in October 2022, which at the time coincided with an important bottom for the gold mining sector.

Performance since 2020 of the BPGDM Gold Miners Bullish Percent Index. A sentiment index for gold mining stocks. The index has fallen rapidly from 95 to below 20 points. This is one of the lowest levels in recent years and suggests the potential for at least a temporary bottom in gold mining stocks. (Source: stockcharts.com)

This suggests that the first buying opportunities are emerging. Given the increased risk of a global recession, it remains important to consider diversification across high-quality equities.

Jeroen Vandamme is the driving force behind Analyse, one of Belgium’s most established investment publications. For more than twenty years, he has closely followed the markets with a particular expertise in precious metals. In addition, he provides in-depth insights into mining stocks, critical minerals and royalty companies, making his analyses highly valued by both private and professional investors. Read more from Jeroen Vandamme.