9.3

8.731 reviews

English

EN

After an impressive rise in the gold price in recent years, the gold market has entered a correction phase and a downward trend. What stands out is that this decline is not only being caused by waning interest from Western investors, but also by selling and a sharp drop in demand from several emerging economies. What is going on in Asia?

Beneath the surface, a new Asian financial crisis is simmering. Indonesia’s stock market is down 35% this year and is among the worst-performing markets in the world. The Jakarta stock exchange has fallen back to the levels seen during the lockdowns of 2020. India’s stock market (-11%) has also lost ground in recent months. China, too, has been struggling for some time. Its stock market is not performing as strongly as elsewhere, and the government is running significant budget deficits. Finally, in Japan, the yen is at risk of falling to a new low. All these countries are also being hit hard by the consequences of the Iran war.

Asian countries such as India, Indonesia, Turkey and Pakistan are being disproportionately affected by higher energy prices as a result of tensions in the Middle East. These economies are heavily dependent on energy imports and are seeing their trade balances deteriorate as oil and gas become more expensive. The consequences are visible on several fronts: local currencies are weakening, import costs are rising and foreign exchange reserves are coming under pressure. As a result, gold purchases are being postponed or even scaled back, despite gold’s traditional role as a hedge against economic uncertainty.

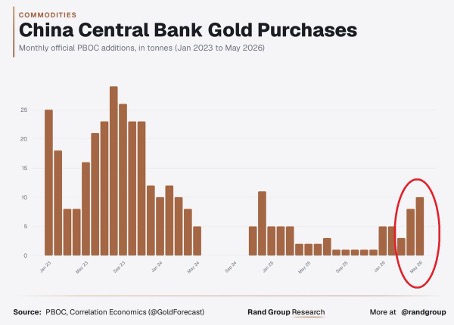

The Chinese central bank (PBOC), however, continues to buy gold at a steady pace. In May, it purchased almost 10 tonnes of gold, the highest level since December 2024. Over the past year and a half, the PBOC usually bought between 1 and 5 tonnes per month. However, a few years ago, in 2023, there were much larger peaks, with China purchasing 20 to sometimes 30 tonnes of gold per month. The PBOC also prefers to buy gold at low market prices. It can be assumed that Chinese gold purchases will increase further if the gold price falls more deeply.

Monthly gold purchases (in tonnes of gold) by the Chinese central bank (Source: Rand Group Research)

Developments in India are less encouraging. After China, the country is traditionally the world’s largest gold consumer. But Indian gold imports fell in April to just 15 tonnes, one of the lowest levels in recent decades. Only during the lockdown year of 2020 were imports even lower.

By comparison, in 2025 monthly Indian gold imports generally fluctuated between 30 and 100 tonnes. Even since the late 1990s, imports usually amounted to 40 to 60 tonnes per month.

To limit the outflow of foreign currency, the Indian government doubled import duties on gold and silver again in mid-May. The rates rose to 15% and 6% respectively, in a clear attempt to curb demand for imported precious metals. And it has worked.

These measures are pushing local gold demand even lower. The Times of India reports that, according to initial estimates, gold demand in May fell by 70% year-on-year. As a result of the new import duties, Indian gold demand has dropped to just 7.5 tonnes. That is even worse than the historically low level of April 2026. According to Reuters, gold demand is so weak that dealers are offering discounts of up to 87 dollars per ounce compared with the local price.

The current decline in Indian gold demand is mainly being caused by a sharp fall in physical imports, not by mass selling of financial gold products. Indian gold ETFs remain relatively stable and also represent only a smaller part of the overall gold market. This suggests that the traditional gold consumer is temporarily standing on the sidelines because of high energy prices and pressure on the rupee, but has not necessarily lost confidence in gold as a long-term savings vehicle.

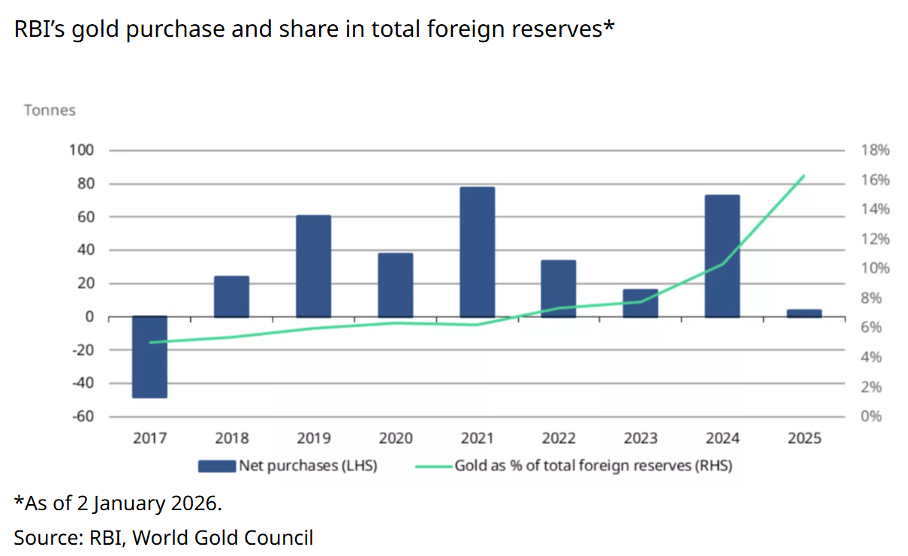

The Indian central bank, the Reserve Bank of India (RBI), was for a long time a large and consistent buyer of gold, especially between 2018 and 2024. In the first months of 2025, the RBI still bought some gold, but since then new purchases have fallen to zero. Indian gold reserves therefore remained stable in terms of volume, but are now suddenly being questioned.

Annual gold purchases by the Indian central bank. Since 2025, hardly any gold has been purchased (Source: World Gold Council.)

In early June, controversy arose after a Bloomberg analysis suggested that the Reserve Bank of India may have sold around 12 billion dollars’ worth of gold to ease pressure on its currency, the Indian rupee, and on its foreign reserves.

If the Indian central bank had indeed sold 12 billion dollars’ worth of gold, then at a gold price of 4,400 dollars per ounce this would amount to roughly 85 tonnes of gold. That represents almost 10% of India’s official gold reserves and would have been one of the largest gold sales by a central bank in recent years.

However, the Indian central bank responded immediately and formally denied the report. According to the RBI, its physical gold holdings remained unchanged at 880.5 tonnes and no gold reserves had been sold. The Indian government also described the reports as incorrect.

There was also speculation that New Delhi might want to mobilise gold holdings from Hindu temples. The Indian government again responded unusually sharply to these reports. Both the alleged gold sales by the central bank and the plans to monetise temple gold were officially denied. The Ministry of Finance even called the reports about a possible use of temple gold “completely false, misleading and without any factual basis”.

But where there is smoke, there is sometimes fire. The rumours, even if they are currently incorrect, do show the extent to which India is in a financial crisis atmosphere.

Turkey is also contributing to the current gold correction. According to market data, the country has sold or swapped around 120 tonnes of gold since the outbreak of the conflict with Iran in order to relieve pressure on the Turkish lira. Such transactions temporarily create additional supply in the market and weigh on the gold price. What India is denying for now, Turkey has already done.

The Japanese yen is now moving dangerously close to floor levels. In recent weeks, the Japanese central bank has been trying to prevent a new, sharp decline in the currency through interventions. In 2022, a sharp decline in the yen coincided with a poor year for markets in general, both for equities and bonds.

Performance of the Japanese yen. Chart source: www.stockcharts.com

Performance of the Japanese yen. Chart source: www.stockcharts.com

A falling yen can indirectly have a negative impact on the gold price, especially through a stronger US dollar and a broader market dynamic in which risks are avoided. In the event of a sudden sharp decline in the yen, as in 2022, Japanese investors may sell gold to cover losses elsewhere.

There is also the factor of the Japanese carry trade. Investors often borrow in yen to buy gold or other assets. But when the yen suddenly becomes volatile or weakens, other positions, including in gold, may be reduced or sold. That creates additional selling pressure in the market.

Finally, a strong dollar makes gold more expensive for non-US buyers. Or, as is currently the case, while the gold price is falling in dollars, it remains relatively higher in local Asian currencies.

Still, the current decline in precious metals does not necessarily mean that the structural bull market in gold is over. The decline in demand in countries such as India is mainly being caused by exceptional circumstances: high energy prices, pressure on currencies and temporary policy measures.

If the energy crisis escalates further and inflation accelerates again, there is a strong chance that demand for gold in these countries will actually return despite higher import duties. As in the past, traders will then try to smuggle a larger share of gold into the country through alternative channels. After all, gold remains one of the most important forms of wealth protection for millions of families in Asia.

In addition, a normalisation of the situation around the Strait of Hormuz would significantly reduce pressure on oil prices, trade balances and currencies. In that scenario, countries such as India could once again become major buyers of physical gold. The current correction therefore appears to be more a consequence of temporary economic stress in emerging markets and a logical correction after the huge price increase of recent years. The long-term case for gold remains intact. The global problems surrounding government debt, inflation and currency debasement will remain a theme for a long time to come.

What should European investors in precious metals do now? Above all, do not panic. Investors with a precious metals savings plan would do well to continue making their regular purchases. Investors who want to time the market a little more should also take advantage of this correction by investing gradually in several steps. Due to the simmering crisis in Asia and other factors, the price correction in precious metals may continue for a while yet. So also keep some cash on hand to be ready for new buying opportunities.

Jeroen Vandamme is the driving force behind Analyse, which is known as one of Belgium’s most established investment publications. For more than twenty years, he has closely followed the markets, with particular expertise in precious metals. He also provides in-depth insights into commodity stocks, critical minerals and royalty stocks, which means his analyses are widely appreciated by both private and professional investors. Read more from Jeroen Vandamme.