9.3

8.682 reviews

English

EN

Gold has replaced US Treasury bonds as the largest reserve asset held by central banks, now confirmed by the ECB itself. Strong gold purchases by central banks are a key driver of rising gold prices — a significant factor now that the gold price has been trading sideways for some time as markets await a resolution to the Middle East conflict.

"Geopolitical tensions are sustaining demand for gold among central banks," writes Christine Lagarde, President of the ECB, in the report published yesterday.

.png)

Left axis: gold purchases in tonnes by central banks worldwide. Right axis: gold price performance. Despite the rapidly rising gold price, purchase volumes have remained fairly stable. Purchases in the first quarter of 2026 are broadly in line with those of the first quarter of 2025. (Source: ECB).

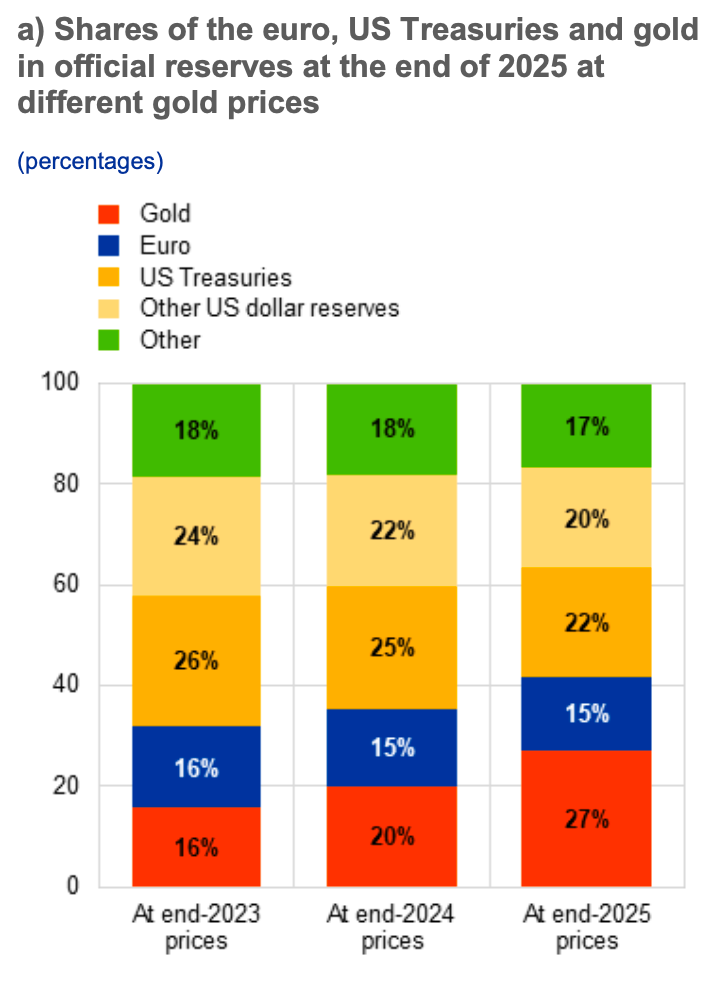

The European Central Bank's analysis found that gold took on a greater role for central banks in 2025. That year, central banks' gold reserves exceeded their dollar reserves in the form of US Treasury bonds for the first time. Gold now accounts for 27% of total central bank reserves worldwide.

Composition of global central bank reserves over the past three years. Red = gold reserves, Blue = euro reserves, Orange = US Treasury bonds, Light orange = other dollar reserves, Green = other (currencies). (Source: ECB).

Central banks hold these highly liquid reserves to support their own currencies. The shift from dollar reserves to gold reflects an effort by countries to move away from the dollar, according to the Financial Times. This is also known as the de-dollarization trend — a multi-year trend in which the dollar is gradually losing its status as the world's reserve currency, while other currencies and gold are gaining in importance.

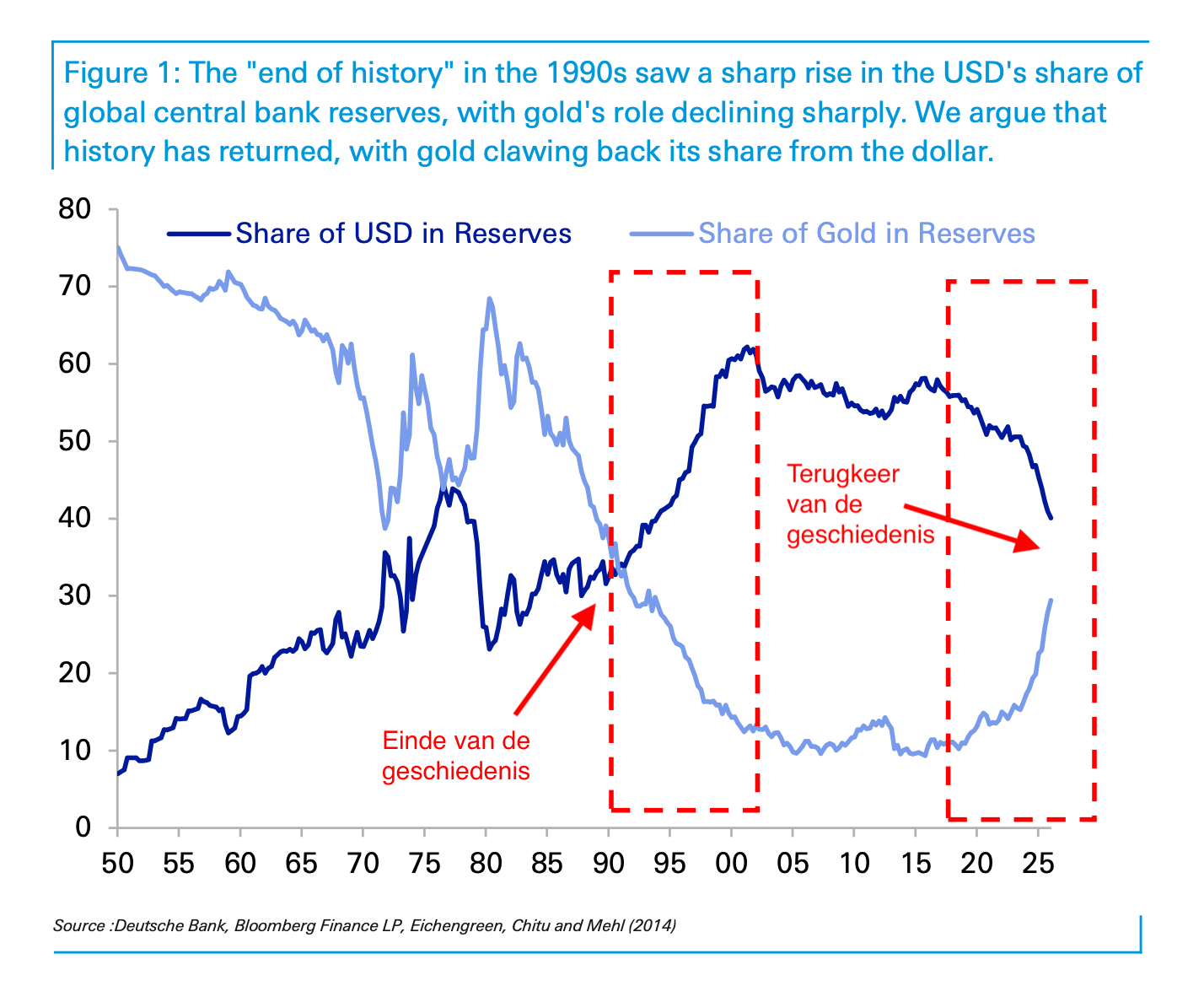

Global central bank reserves since the 1950s, based on IMF data. The light blue line shows the percentage of dollars in total reserves, the dark blue line shows gold. (Source: Deutsche Bank).

Gold purchases by central banks are a driving force behind the gold price. A comprehensive Deutsche Bank analysis we covered previously not only confirms this relationship but also outlines the long-term trend. Historically, gold was always the primary reserve asset of central banks. Following the fall of the Berlin Wall, easing geopolitical tensions increased confidence in a dollar-dominated financial system. That trend is now reversing.

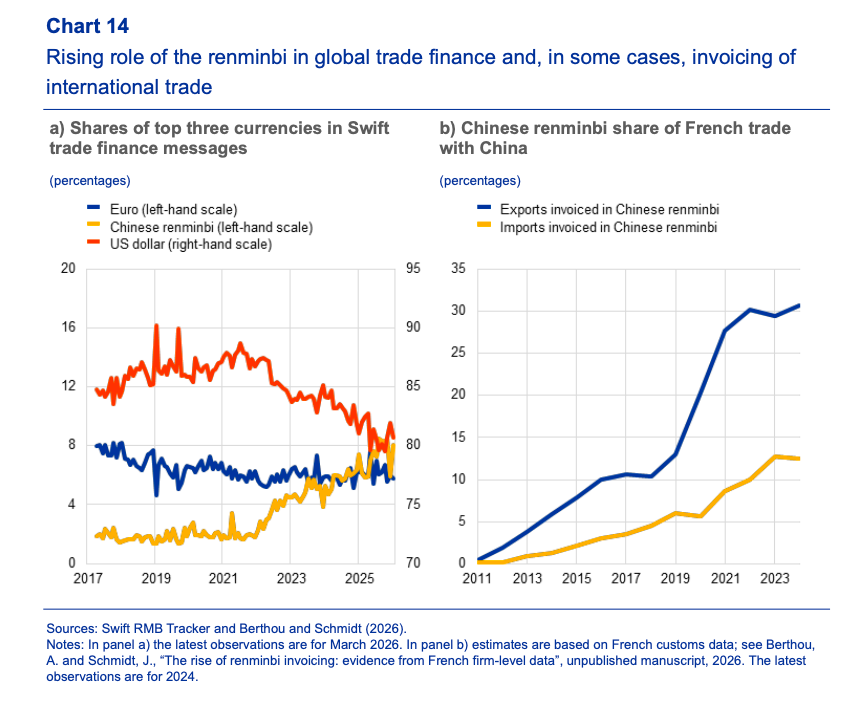

The de-dollarization trend is not visible across all domains. The dollar still leads in international currency trading and the world of stablecoins. However, the ECB report identifies two areas where the dollar is losing ground: international trade and debt issuance.

Left chart: currency shares in global trade processed through the SWIFT payment system. The declining red line shows the dollar's share, the blue line shows euro transactions, and the rising yellow line shows the Chinese renminbi. Right chart: specifically for France, the share of trade payments with China settled in renminbi, blue for exports and yellow for imports. (Source: ECB).

In international trade, the dollar is losing ground, the euro is holding steady, and the Chinese renminbi is rising significantly. International trade payments refer to the currency in which imports and exports of goods and services are settled. For example, whereas European imports of goods from China were previously paid in dollars, this is increasingly happening in Chinese renminbi. A major threat to the dollar would be if the renminbi gains ground in international oil trade.

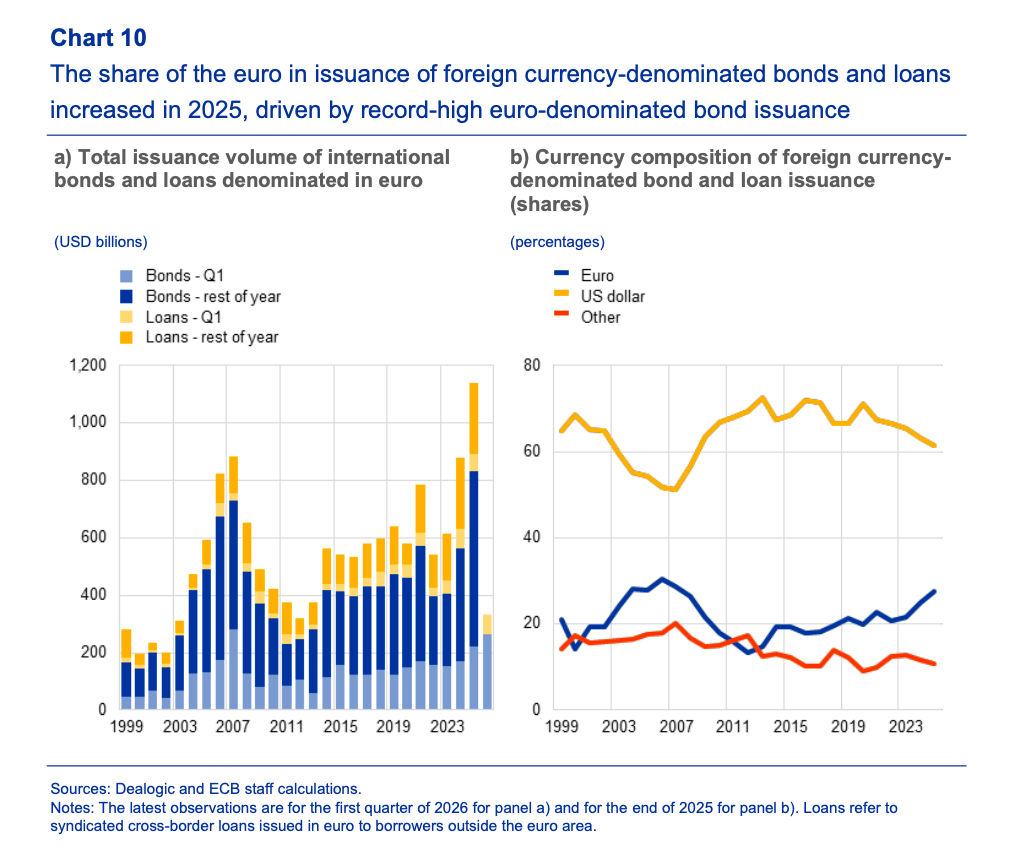

Left chart: total international bonds and loans issued in billions of euros. Right chart: share of currencies in bonds and loans expressed in percentages. Yellow downward line for dollars, upward blue line for euro, red line for other currencies. (Source: ECB).

Notably, the euro is playing a growing role in international debt issuance and equity markets. In 2025, 30% more international corporate bonds and loans were issued in euros than the year before. Foreign interest in European stocks and bonds also reached its highest level since the introduction of the euro.

The ECB's report addresses the euro's growing role, the opportunities for the currency, and the associated risks, as European policymakers are seeking to push back against Trump. There is a perceived unique opportunity for the euro to emerge as an alternative to the dollar. The question is how much Europe itself is contributing to this shift, versus how much is simply an international reaction to Trump's unpredictable policies.

The Trump administration has, on one hand, placed enormous pressure on international trade through a tariff war and the Iran conflict, which led to the closure of the critical Strait of Hormuz. On the other hand, international relations have been rattled by Trump's claim on Greenland earlier in 2026 and the broader pressure on NATO. Earlier this year, there were briefly multiple 'sell America' signals, indicating that international investors were swapping US assets for European ones for these very reasons.

Notably, the ECB identifies central banks' strong appetite for gold as a challenge to the euro's growing role, alongside initiatives from BRICS nations to develop alternatives to the SWIFT payment system.

It seems clear that central banks worldwide have more confidence in gold than in the euro. Gold now accounts for 27% of global central bank reserves — nearly double the share of euro reserves, which stands at 15%.

The gold price continues to trade sideways as markets await a peace deal between Iran and the United States. Fresh exchanges of attacks are putting further pressure on gold by pushing inflation expectations higher. Negotiations are currently stalling, as Iran is demanding an end to Israeli attacks in Lebanon before progress can be made.

Meanwhile, stronger-than-expected jobs data are opening the door to a potential rate hike by the Fed (the US central bank). Beth Hammack, president of the Cleveland Fed, indicated that the Fed may soon need to shift its focus toward combating inflation. Inflation has remained above target for five years and shows little sign of declining quickly given elevated oil prices. Her remarks were widely read as a hint at a possible rate increase.

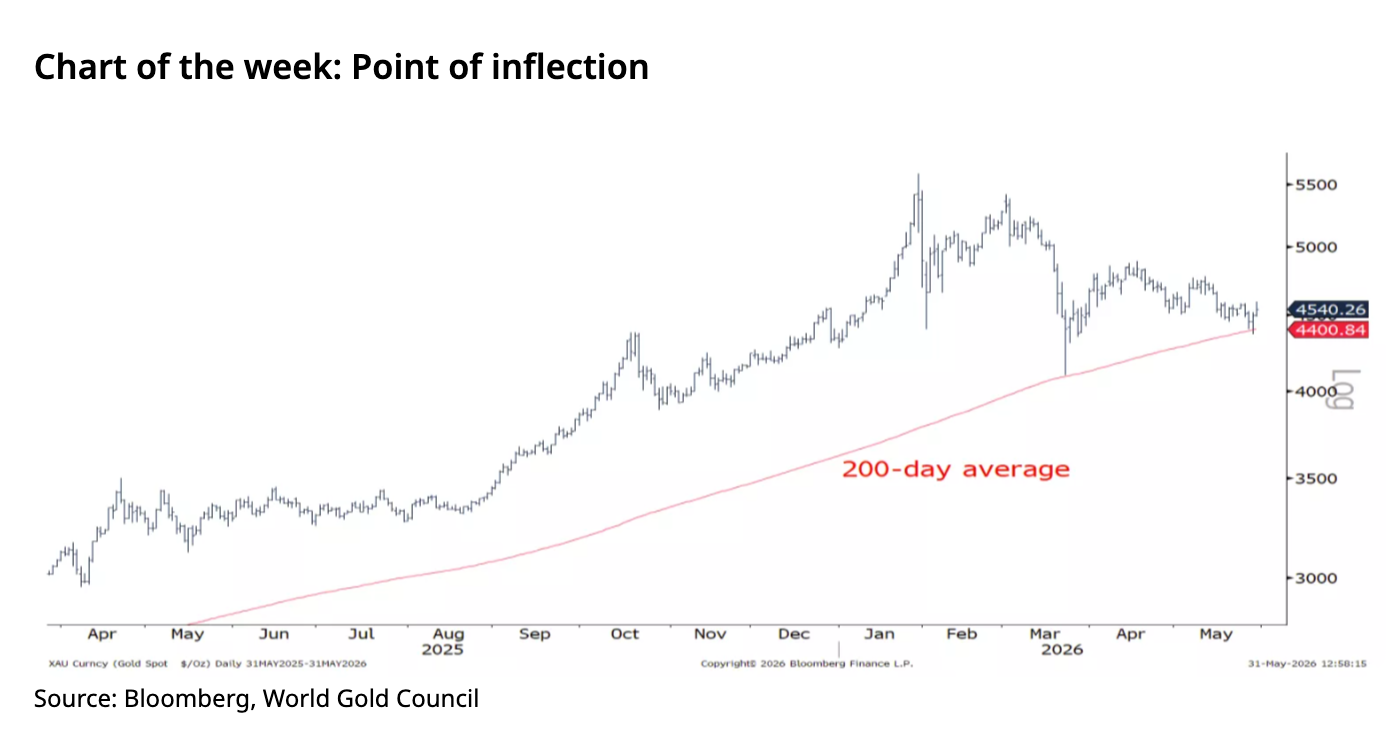

Gold price in dollars over the past 12 months, with the red line representing the 200-day moving average. Source: World Gold Council.

Despite these headwinds, gold continues to hold above the key technical support level of $4,401 per troy ounce (€3,790), according to the World Gold Council. This support level is derived from the 200-day moving average of the gold price. If the price repeatedly falls below this level, there is a technical risk of further declines as it could trigger sell orders. The reverse also applies: if gold consistently closes above $4,607 (€3,966), further price gains become more likely, the World Gold Council's analysts write.

In the near term, attention remains on how US inflation will influence the Fed's interest rate policy. Today (Wednesday, June 3), markets are watching for new talks between Israel and Lebanon, as well as the publication of the Fed's Beige Book, which could offer further insight into the state of the US economy.