9.3

8.779 reviews

English

EN

Gold and silver have faced significant headwinds in recent months due to higher interest rate expectations and a stronger dollar. Yet this correction could in fact create a new buying opportunity, now that many investors have exited and sentiment around precious metals has become notably negative.

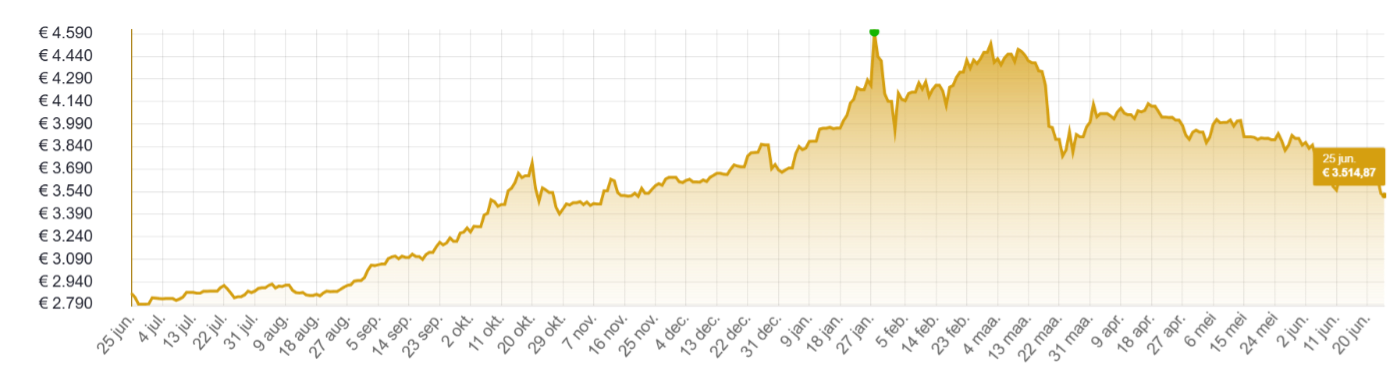

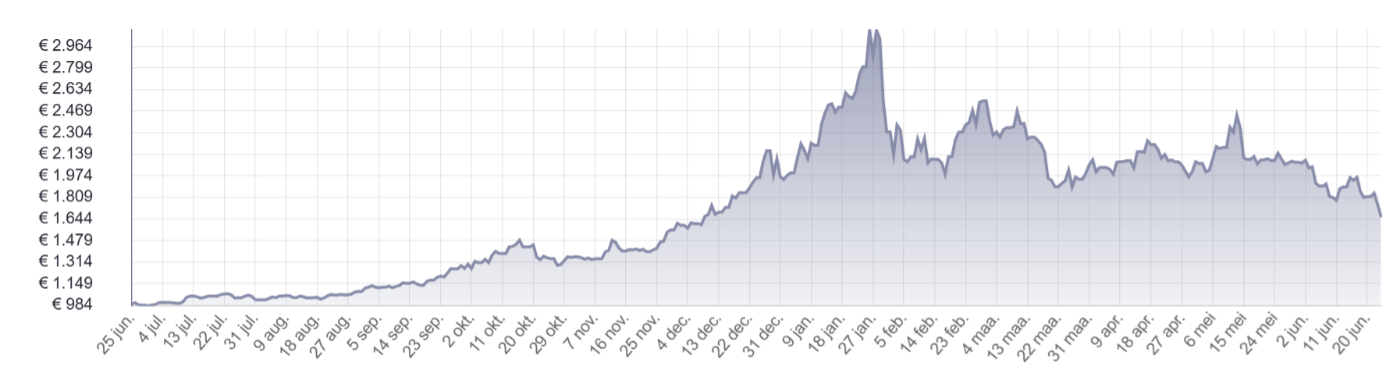

The first half of the year was one of extremes in the precious metals markets, with record prices for gold and silver followed by a sharp correction. Meanwhile, negative sentiment toward precious metals appears to be approaching a peak. After nearly six months in 2026, the returns for gold and silver stand at -7.5% and -19%, respectively. Due to the strong dollar, these figures are slightly lower in euros, at -4.5% and -16%. Over twelve months, however, the return on gold still amounts to almost 20%. For silver, it is as much as 57%.

Chart: gold price over one year with 50-day and 200-day moving averages (Source: StockCharts)

As previously explained, the correction came after market perception made a 180-degree turn since the beginning of this year. Markets are now fully anticipating rate hikes, whereas earlier it was still expected that the new Fed Chair Kevin Warsh would primarily focus on rate cuts. Higher long-term interest rates coincided with a stronger dollar, and both factors are negative for gold in the short term.

The CME FedWatch Tool shows that, for the monetary policy meeting on July 29, a clear majority of 66% still expects the policy rate to remain unchanged. This changes for the remaining Fed meetings in September, October and December. For September, 67% already expects a first rate hike, with 50% expecting 25 basis points and 17% already expecting an immediate jump of 50 basis points. Only a quarter expects rates to remain at their current level in October, and that figure falls further to 16% for December.

An analyst at Bank of America released a report earlier this week arguing that the Federal Reserve would raise rates three more times this year. This would take place at the policy meetings in September, October and December. The policy rate would be increased by 25 basis points each time, bringing it to 4.25% to 4.5%. The analyst points to inflation and the strong labor market. However, the chances that events will move that quickly are small. The oil price has fallen by more than a third in barely a month, from $105 to less than $70 for a barrel of US West Texas Intermediate. That lower oil price will feed through to other goods and services in the coming months, which will also reduce inflation.

Chart: gold price over twelve months, in EUR per oz (Source: HollandGold)

However, there is an even more important reason why multiple rate hikes are undesirable and therefore unlikely: the high debt position of the United States. It currently stands at $39.3 trillion, or $39,320 billion, and more than one trillion dollars in interest costs are paid on it annually, equivalent to roughly one fifth of tax revenues. This year and next year, almost half of this debt will have to be refinanced. Given the ever-higher budget deficits, the debt trend is still upward. Combined with rising interest rates, interest costs will continue to increase, which threatens to become unsustainable over time.

On the Comex futures exchange, open interest, or the number of outstanding futures contracts, is now almost a quarter lower than a year ago. For futures and options combined, the decline is as much as 40%. The cause mainly lies in the reduction of long positions and momentum traders no longer being active in gold. Put differently, there are currently very few people on board the gold train, and this is an excellent setup for the start of a new rise.

Chart: silver price over twelve months, in EUR per kg (Source: HollandGold)

Meanwhile, the major banks are falling over one another to revise their gold price forecasts downward. Deutsche Bank was still maintaining a price target of $6,000 until mid-April. That has now been lowered to an average of $4,300 for the third quarter. ING is slightly more modest and expects an average of $4,600 for the fourth quarter, down from $5,000. And there are several other examples.

In doing so, the major banks once again show that they are hopelessly behind the curve. Last year, the exact opposite happened. After the gold price had doubled in a year and a half, a bidding contest emerged with ever-higher price forecasts, which are now being revised.

The current correction from the peak amounts to 29%, which is slightly higher than the average historical pullback during a bull market in gold. This is no guarantee that the gold price cannot move somewhat lower in the short term, but this pullback is a necessary phase to form a new base for further gains after the parabolic move of late last year and early this year.

Be sure to take a look at our YouTube channel

On behalf of Holland Gold, Paul Buitink and Yael Potjer interview various economists and macroeconomic experts. The aim of the podcast is to give viewers a better understanding of, and more guidance in, an increasingly fast-changing macroeconomic and monetary landscape. Click here to subscribe.