9.3

8.923 reviews

English

EN

The gold price recovered quickly on Monday after it became known that Iran and the US had reached a peace agreement. On Wednesday evening, the US central bank left interest rates unchanged, but the much-discussed, newly appointed Fed chair Kevin Warsh struck a hawkish tone. Stocks and gold both moved sharply into the red. Meanwhile, research by the World Gold Council removes the last doubts: central banks expect to further expand their gold reserves, the FD reports. In this market update, we discuss the three most important developments for gold.

The gold price rose by 3.6% in a single trading day after mediator Pakistan announced that a peace agreement between Iran and the US had been reached. The agreement would also mean the full reopening of the Strait of Hormuz, through which roughly one fifth of global oil transport passes. The oil price promptly fell on the news.

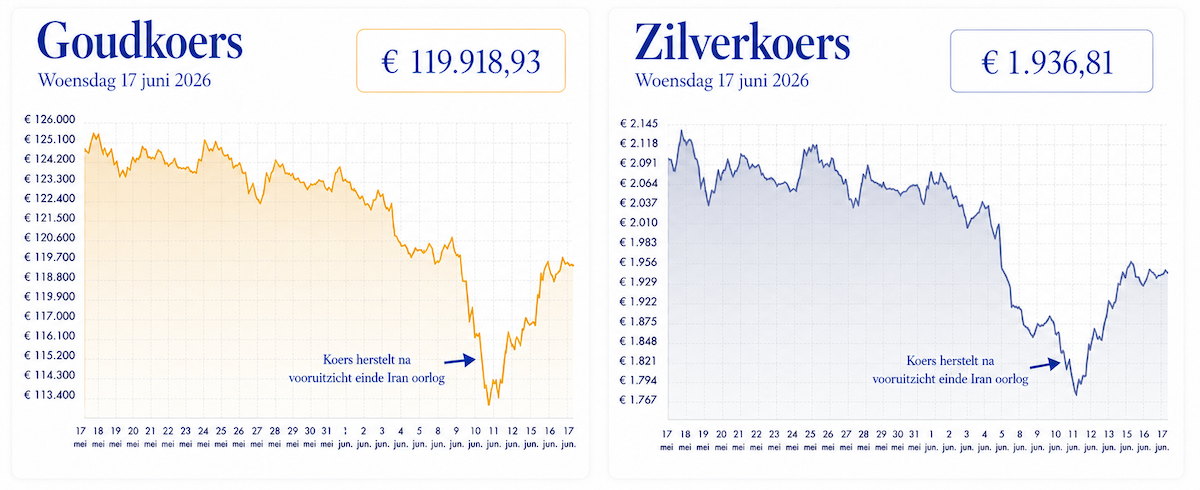

Gold price and silver price in euros per kilo over the past month. The recovery started after the low on 10 June and accelerated on Monday 15 June, after the peace agreement was announced.

An important caveat to this news is that the agreement is not yet final and is mainly a declaration of intent. The so-called ‘memorandum of understanding’ is a step towards a final peace agreement, and the two countries have given each other 60 days to reach one. According to BNR commentator Bernard Hammelburg, Iran is the clear winner in this ‘deal’. For now, however, the 14-point memorandum does mean an end to the war.

Gold price over the past twelve months in dollars, with Barclays’ price forecast shown as the red line. Source: Investinglive

This raises the question of what effect a possible end to the conflict in the Middle East will have on the gold price. According to British bank Barclays, gold could rise to $4,900 per troy ounce over the course of the year. That would imply a gold price of approximately €135,700 per kilo at current exchange rates. The bank sees the 20-25% price correction in gold since the outbreak of the war with Iran as a temporary repositioning in the market, not as a trend reversal.

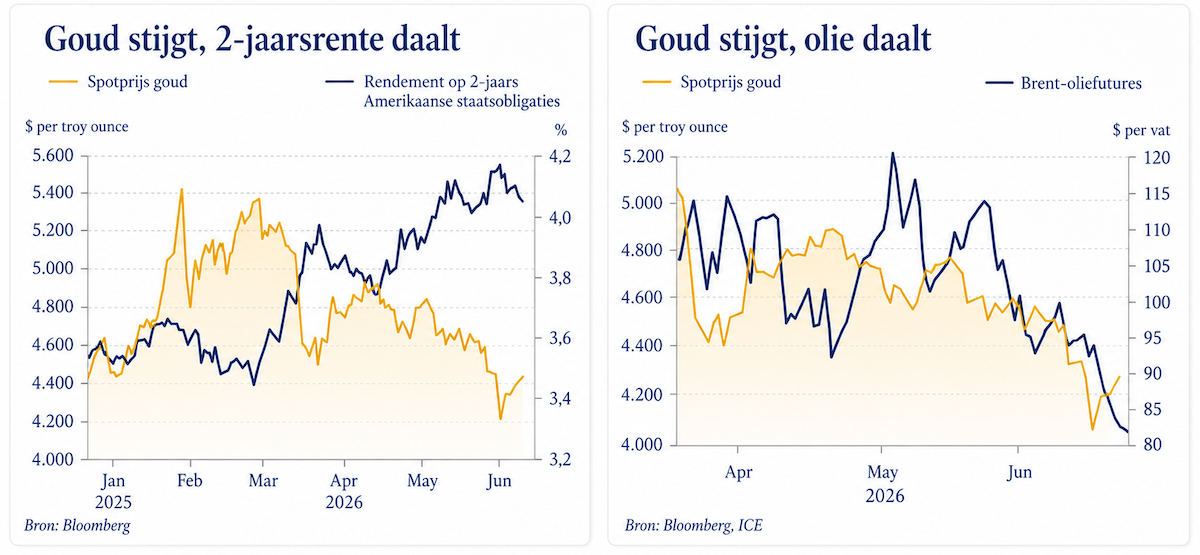

Left chart: Gold price versus the yield on US 2-year Treasury bonds over the past six months, source: Bloomberg. Right chart: Gold price versus oil price over the past three months, source: Bloomberg.

Over the past few months, gold has shown an unusual correlation with the oil price and with US bond yields. The reason is as follows: high energy prices push up inflation, which increases the likelihood that the US central bank (Fed) will keep interest rates unchanged or even raise them. Higher interest rates make government bonds a more attractive safe haven than gold, which does not pay interest. Because of this relationship, a falling oil price leads inflation expectations, and therefore also the likelihood of an interest rate hike, to be revised downwards. That is when the gold price starts to climb again.

All eyes were therefore on the interest rate decision of the US central bank (Fed). On Wednesday 17 June, at 20:00 Dutch time, it was announced that the Fed had left interest rates unchanged. Although markets had already expected rates to remain unchanged, the hawkish tone of the statement came as a shock.

What does hawkish mean? The Fed can act like a dove (dovish), lowering interest rates to stimulate the economy and the labour market, or like a hawk (hawkish), raising interest rates to cool the economy and inflation. The Fed now appears to be choosing a hawkish route, and any hope markets had for an interest rate cut has therefore evaporated.

The brand-new Fed chair Kevin Warsh held his first press conference and immediately announced several changes. Unlike his predecessor Powell, Warsh wants to provide fewer forecasts. In Warsh’s view, markets have become too accustomed to waiting for hints from the Fed about possible future interest rate decisions. Warsh would rather let financial markets do their own homework, so that the Fed can see how markets interpret economic news.

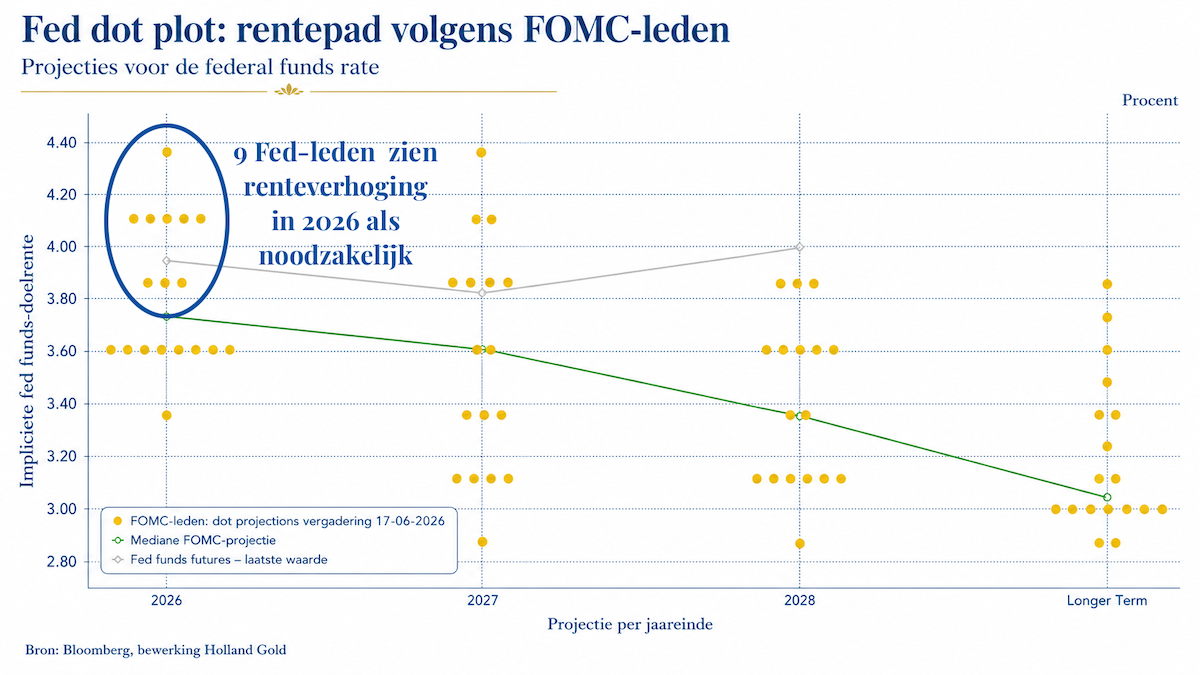

Dot plot (Source: Bloomberg, edited by Holland Gold)

The dot plot that the Fed publishes alongside its interest rate decisions shows what Fed members themselves consider necessary in terms of monetary policy. Each dot represents one of the 18 Fed members. What alarmed markets in particular was the fact that 9 of the 18 members consider an interest rate hike necessary this year. According to Bloomberg, markets now expect an interest rate hike in October.

One dot is missing: that of Warsh himself, who deliberately abstained from the dot plot because he wants to provide fewer forecasts. It is possible that under Warsh, the Fed may even stop publishing the dot plot altogether.

Warsh proceeded cautiously during his press conference, but still appeared to focus mainly on US inflation. Over the past five years, US inflation has been well above the Fed’s 2% target, something Warsh clearly pointed out. In recent months, Trump put a great deal of pressure on Warsh’s predecessor Powell to cut interest rates. There had been speculation over whether Warsh, who has a good relationship with Trump, might be too sympathetic to Trump’s position. This could also undermine the independence of the Fed. With this decision, Warsh has shown himself to be independent and appears not to be yielding to Trump’s pressure.

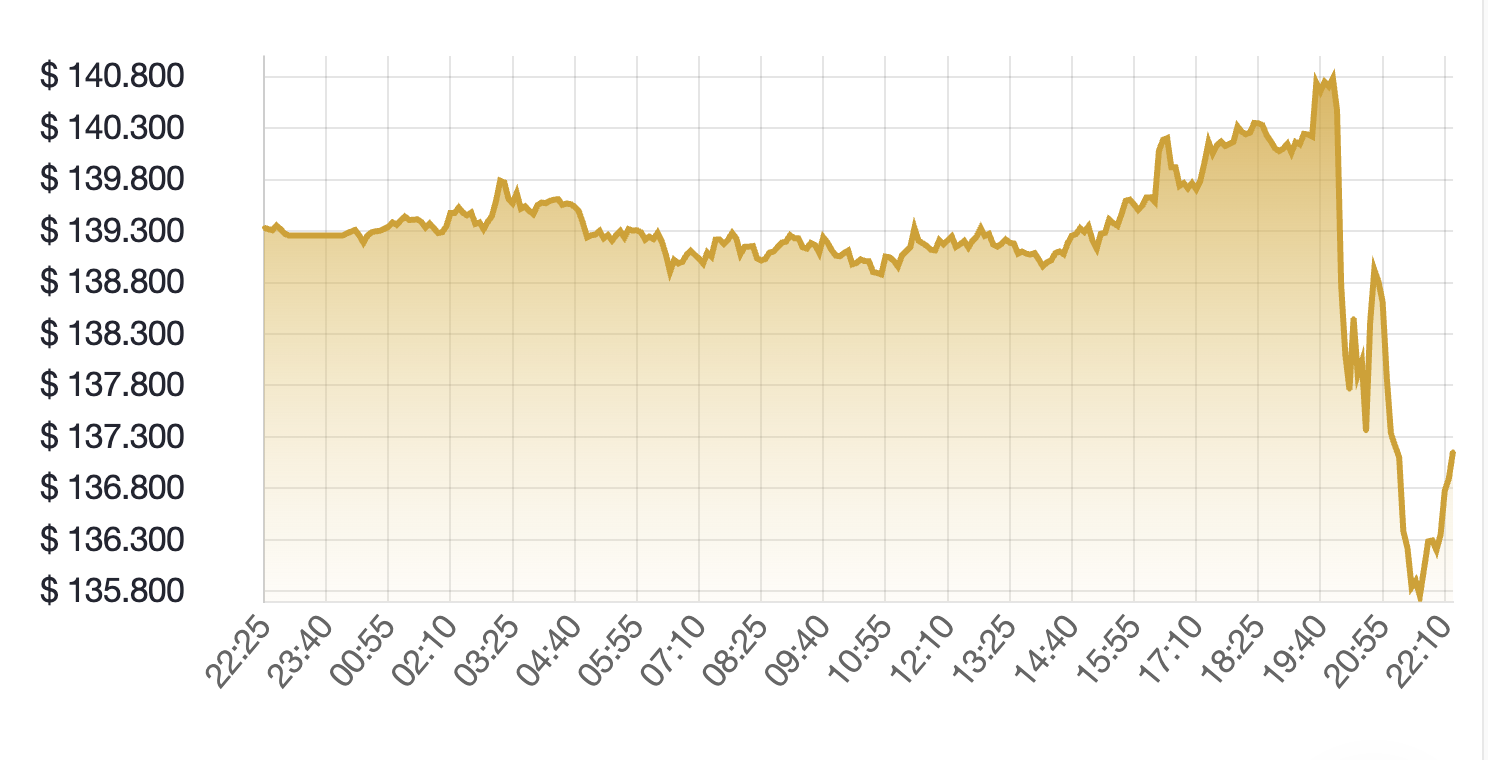

Gold price in dollars falls quickly on Wednesday evening 17 June after the interest rate decision and statement were published

While that is a good sign for America’s financial stability, a possible interest rate hike is bad news for gold. Gold fell by almost 1.5% immediately after the news. The dollar rose quickly, causing the euro to fall by 0.9% against the USD. This softened the blow for the gold price in euros, which therefore fell by only 0.6%.

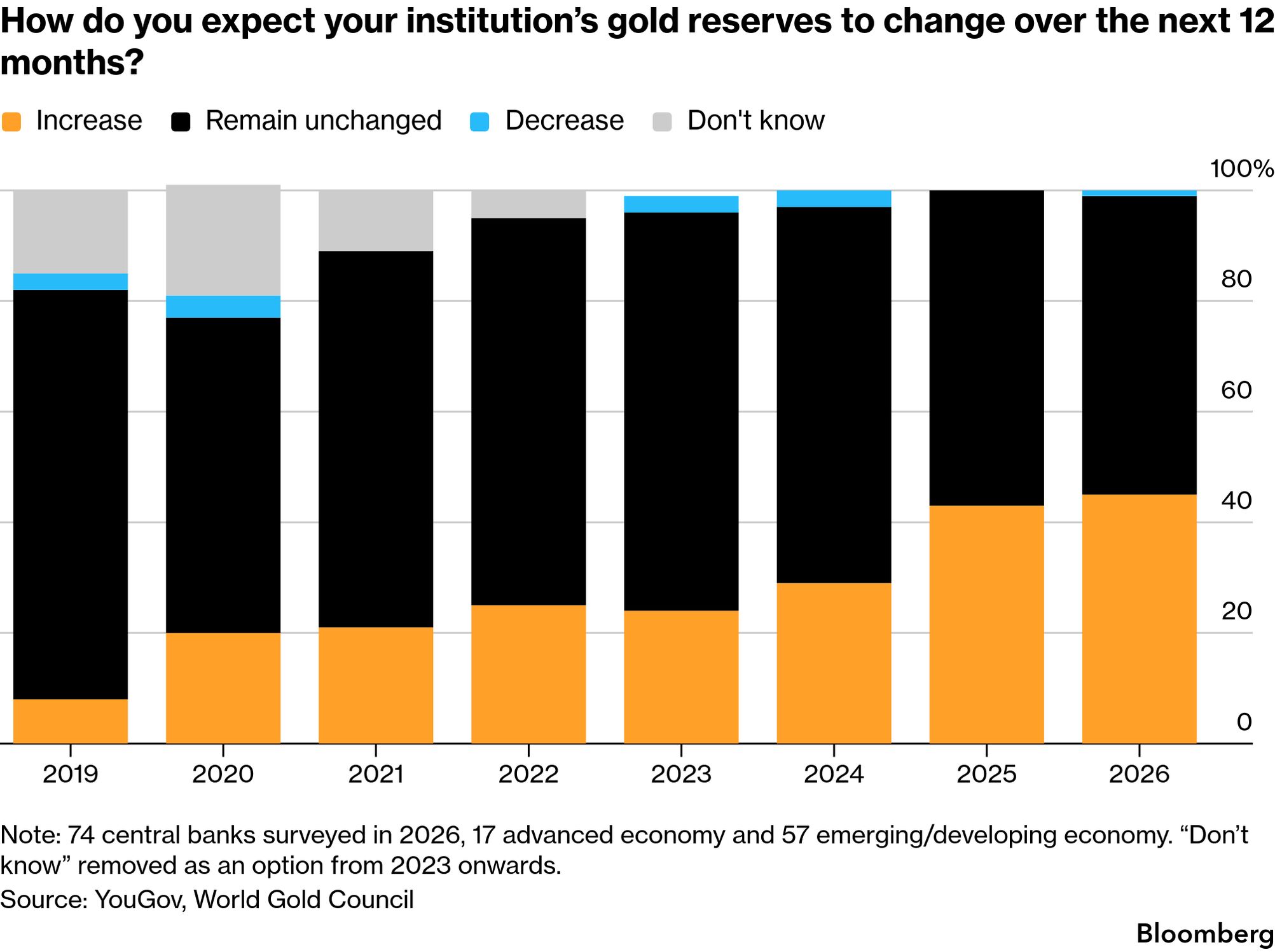

Yes, central banks continue to buy gold in large quantities, according to a survey by the World Gold Council among 76 central banks. As many as 89% expect global central bank gold reserves to increase over the next twelve months. A record 45% also say they expect to expand their own gold reserves in 2026.

How do central banks expect to adjust their gold reserves? Orange: increase gold reserves; black: keep gold reserves unchanged; blue: reduce gold reserves. Source: Bloomberg.

Although there are reports that the central banks of Turkey and Russia are selling large amounts of gold, it appears that central banks worldwide actually want to buy more gold. Over the past four years, central banks worldwide have purchased an average total of 1,000 tonnes of gold per year, compared with 500 tonnes in the years before that. The number of banks expecting to buy gold has risen sharply since 2019.

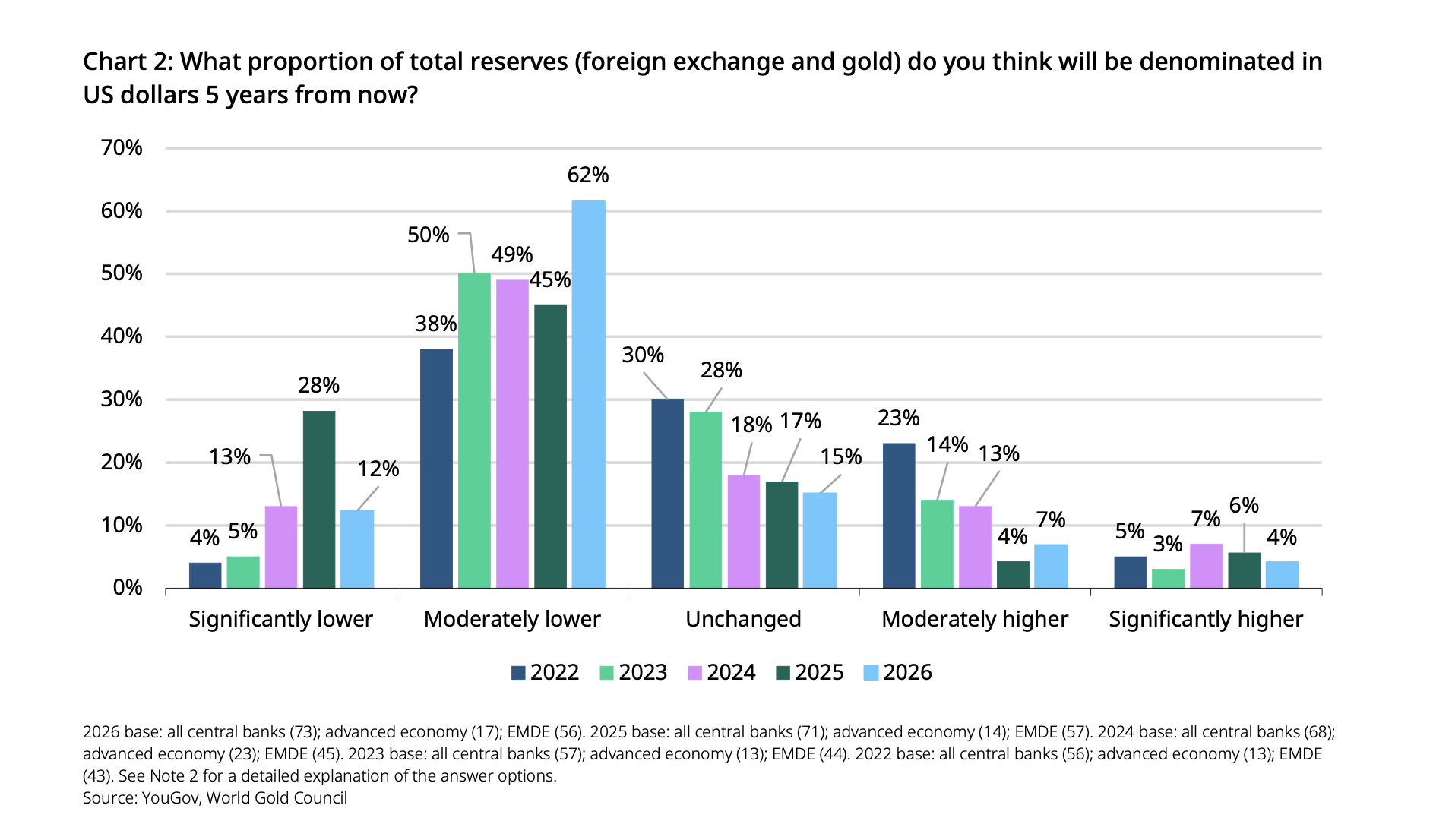

Do central banks expect dollar reserves to decline relative to gold? Responses broken down by year from 2022 to 2026. Answers from left to right: significantly fewer dollars; moderately fewer; unchanged; moderately higher; significantly higher. Source: World Gold Council.

The growing gold reserves are coming at the expense of the dollar, the Financieel Dagblad also writes. According to the World Gold Council’s survey, 74% of central banks expect global dollar reserves to decline over the next five years. This expectation was shared by central banks from both the Western world and emerging markets. This would mean that central banks will hold fewer dollars in the future in the form of US Treasury bonds or other dollar reserves.

The shift between 2026 and all previous years is striking. Whereas in 2022, 28% still expected dollar reserves to increase, in 2026 that figure is only 11%. The expectation that dollar reserves will shrink rose sharply to 73% in 2025, compared with 42% in 2022.

This aligns seamlessly with the trend previously identified by Deutsche Bank, in which central banks are steadily increasing their gold holdings while dollar reserves decline in relative terms, in response to geopolitically and economically uncertain times.

Be sure to also visit our YouTube channel

On behalf of Holland Gold, Paul Buitink and Yael Potjer interview various economists and experts in the field of macroeconomics. The aim of the podcast is to give viewers a better understanding of, and a firmer grip on, an increasingly fast-changing macroeconomic and monetary landscape. Click here to subscribe.