9.3

8.833 reviews

English

EN

The recent decline in the gold price is widely attributed by analysts to a sudden need for liquidity among investors. Margin calls, forced selling, and the adage “sell what you can, not what you want” are often cited as explanations. However, financial commentator Jeroen Blokland raises serious doubts about this interpretation in his latest blog. According to him, broader market sentiment points to a different, less dramatic cause.

A key argument against the liquidity narrative is the absence of genuine panic in financial markets. When investors are in urgent need of liquidity, this is typically accompanied by sharp price declines and extreme volatility in equity markets.

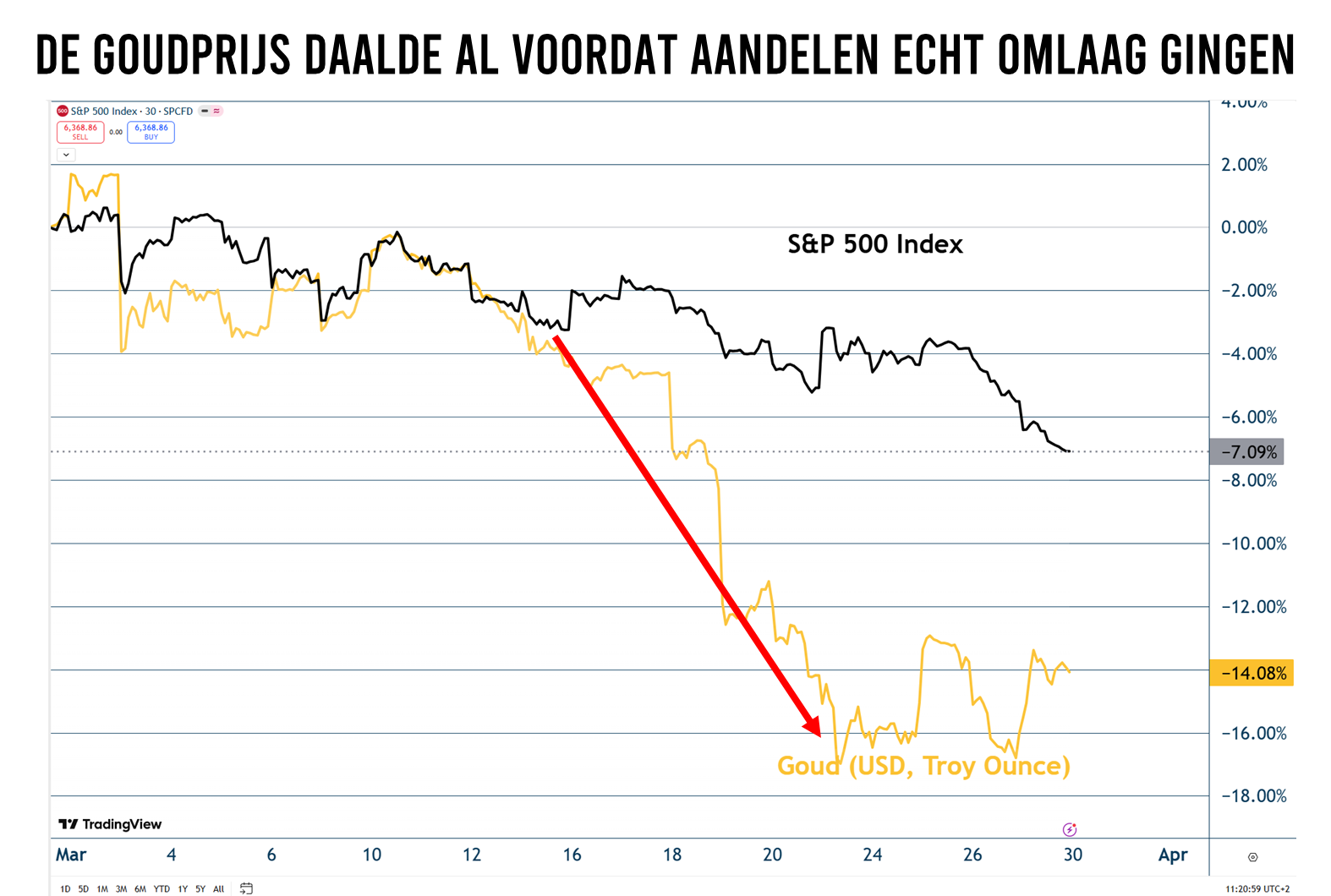

Although the S&P 500 Index briefly declined following the outbreak of tensions surrounding Iran, a large-scale sell-off failed to materialize. In fact, when gold experienced its sharpest decline, equities were only slightly lower. This does not point to a systemic crisis in which investors are forced to liquidate positions en masse. Notably, gold actually recovered at moments when equities declined further afterward. This pattern undermines the idea that gold was primarily sold to offset losses elsewhere.

Not only equities, but also the bond market offers little support for the liquidity thesis. The so-called MOVE Index — a gauge of expected volatility in the bond market — only began to rise after the gold price had already largely declined.

If liquidity stress had been the cause, the bond market in particular should have shown signs of tension earlier. That was not the case.

Another frequently cited explanation is that investors were simply overexposed to gold and therefore exited en masse. According to Blokland, this argument is also weakly substantiated.

In reality, gold remains significantly underrepresented in institutional portfolios. For example, the average allocation among family offices is only around 0.9%. Among pension funds and insurers, this share is often even lower. This makes it unlikely that large-scale selling from this group caused the price decline.

Even if investors needed liquidity, gold positions are simply too small to play a decisive role.

Data on derivative positions held by hedge funds and other active investors shows that while the number of long positions has declined, this group remains net positive on gold.

An important detail: a large part of this reduction took place before the escalation in Iran. This points more toward risk management amid rising uncertainty than to panic-driven selling afterward.

The war in Iran currently dominates market sentiment. In theory, a conflict can lead to liquidity pressure, for example when countries are forced to tap into their reserves.

A concrete example is Turkey, which sold approximately $8 billion worth of gold after the outbreak of the war. However, this appears to be an exceptional case, driven by specific economic conditions such as high energy dependence and geographic proximity to the conflict zone.

For other countries, this applies to a much lesser extent. Moreover, central bank buying has already slowed in recent quarters, weakening the supportive effect on the gold price.

According to Blokland, the most plausible explanation lies closer to home: investors are simply taking profits.

The gold price has risen sharply since 2024 and, even after the recent correction, has still roughly doubled. In that context, it is logical that investors at some point decide to lock in (part of) their gains.

According to him, this phenomenon is often confused with ‘extreme positioning’. Not because everyone was overly bullish, but because many investors were sitting on substantial unrealized gains.

The common explanation that gold declined due to acute liquidity stress holds up only partially upon closer inspection. Neither equity nor bond markets showed signs of broad-based stress, and investor positioning does not point to widespread forced selling.

This shifts the focus to a less spectacular, but more plausible cause: profit-taking following an exceptionally strong rally.

The correction in gold therefore does not necessarily signal a structural weakening. On the contrary, according to Blokland, the precious metal remains attractive over the long term, despite recent volatility. Read the full analysis by Jeroen Blokland.