9.3

8.813 reviews

English

EN

Gold is recovering after the gold price fell below €112,000 per kilogram at the end of June. Is this the end of the decline? On 1 July, the gold price surged by as much as 3.1% from its lowest point earlier that day. While some say that the new Fed Chair Warsh has killed the bull market in gold, he has now become the very reason for the rally. What is happening to the gold price?

After enormous price increases earlier this year, the gold price has fallen in recent months to below its opening level on 1 January. While in the Netherlands we often follow the price of gold per kilogram, international markets usually focus on the price of 1 troy ounce of gold. Last week, the price of gold briefly fell below €112,000 per kilogram and below the symbolic threshold of $4,000 per troy ounce (31.1 grams). The question is whether the headwinds for gold will persist, or whether we have now reached a bottom from which the yellow metal can begin to recover.

Analyst Jeffrey Christian of CPM Group does not rule out a decline to $3,800 per troy ounce, but points out that the long-term case for gold remains intact. At the same time, we are seeing banks such as Goldman Sachs reaffirm their positive view on gold. “Gold is not done yet,” said Samantha Dart of Goldman Sachs in an internal update to investors. According to the US bank, gold will even rebound to $4,900, driven by gold purchases by central banks in emerging economies.

For reference: since the dollar has strengthened against the euro, a bottom of $3,800 corresponds to €3,330, while a price of $4,900 corresponds to €4,295 per gold coin of 1 troy ounce.

Last week, we wrote about the price forecasts of several banks. Those forecasts fall into two camps: first, a group that expects gold to face prolonged headwinds from higher interest rates; second, a group that expects the gold price, despite this, to rise or to be supported by central banks continuing to buy gold. Goldman Sachs belongs to the latter group, and its case received support this week from an OMFIF report.

According to a survey by the Official Monetary and Financial Institutions Forum (OMFIF) among central banks, they foresee an important role for gold. The Global Public Investor 2026 report reveals how central banks see the future: as extremely uncertain. As many as 79% of central banks observe a shift towards a multipolar system.

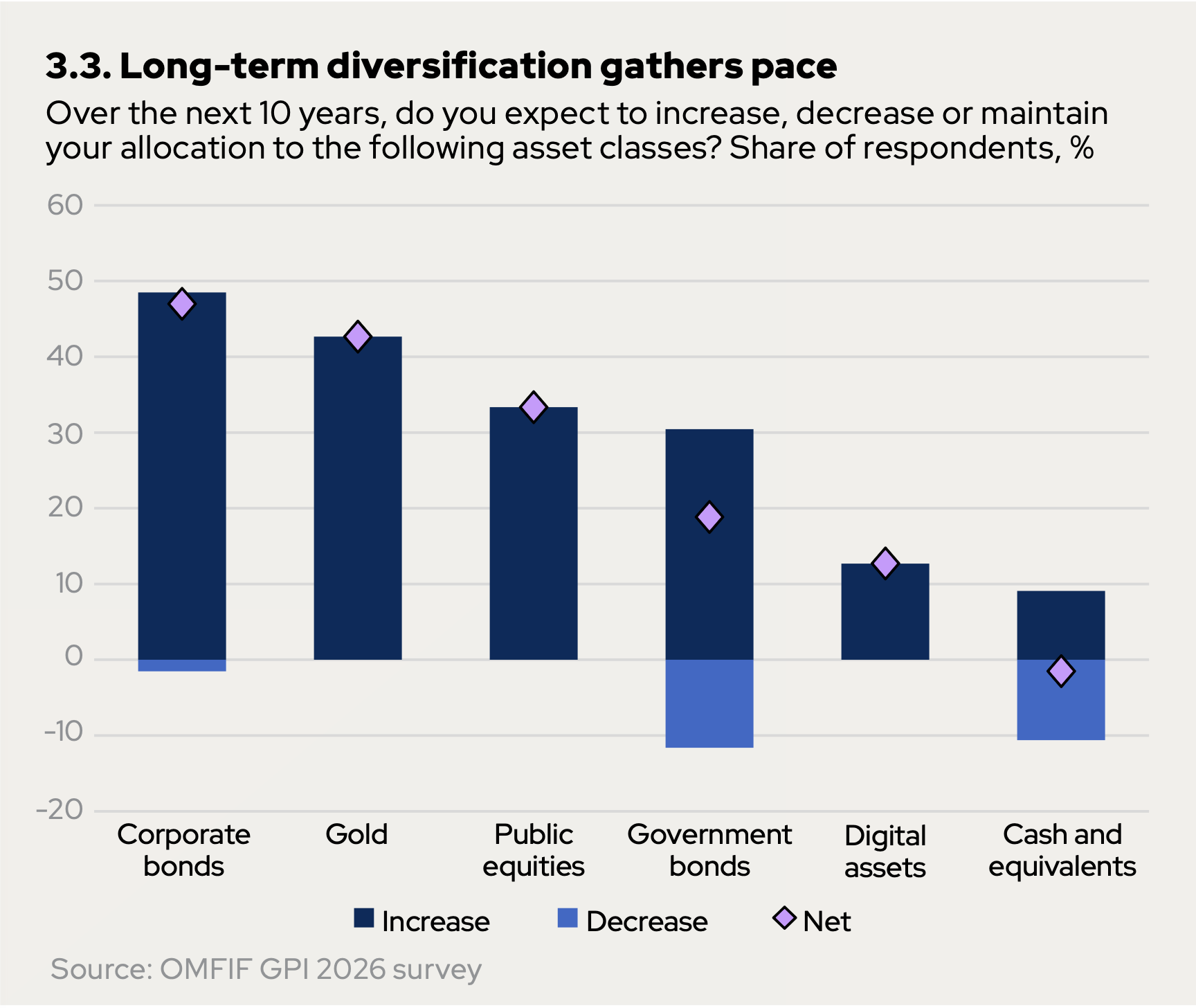

Gold is one of the biggest winners from this shift, and 82% of central banks hold gold reserves. According to the survey, 43% of central banks expect to continue expanding their gold reserves over the next ten years. In the short term, 30% expect to buy gold over the next 12 months.

Percentage of central banks expecting to expand certain reserves over the next ten years. Corporate bonds rank first at 47%, followed by gold in second place at 43%. Government bonds and cash are also expected to decline. (Source: OMFIF).

Readers may be experiencing a sense of déjà vu, because just a few weeks ago the World Gold Council presented a similar report. As was the case then, the same picture is emerging. The dollar and US Treasury bonds are under pressure among central banks. Gold and other reserves are gaining ground.

Central banks are generally less sensitive to the gold price and are strategically expanding their gold reserves to protect themselves against geopolitical and economic uncertainty. That is why banks such as Goldman Sachs also see this as an important driver of higher gold prices in the second half of 2026.

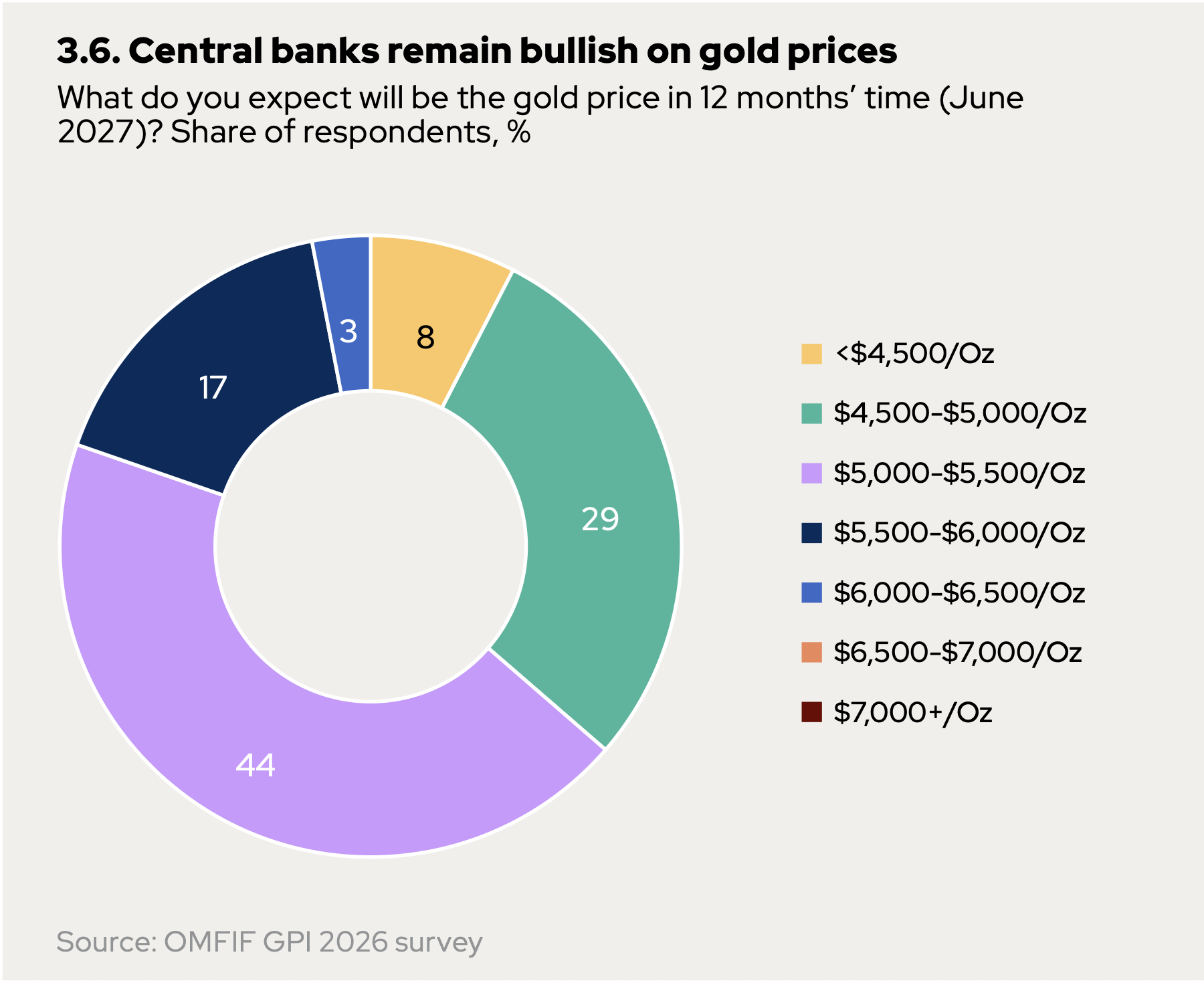

Percentage of central banks with a particular price expectation for the next 12 months. Prices in dollars per troy ounce of gold. (Source: OMFIF).

In the OMFIF report, central banks were also asked about their price expectations for gold over the next 12 months, up to June 2027. Only 8% expect a price below $4,500 per troy ounce, while 64% foresee a price above $5,000.

And we remain with central bank news. Kevin Warsh is the new chair of the US central bank, the Federal Reserve (Fed). During the 18 June interest rate decision, he startled markets not because he kept rates unchanged, but because he made the prospect of a rate cut disappear like snow in the sun. He struck a hawkish tone, with renewed focus on excessively high inflation. Markets subsequently priced in an interest rate hike in October, causing the gold price to fall further.

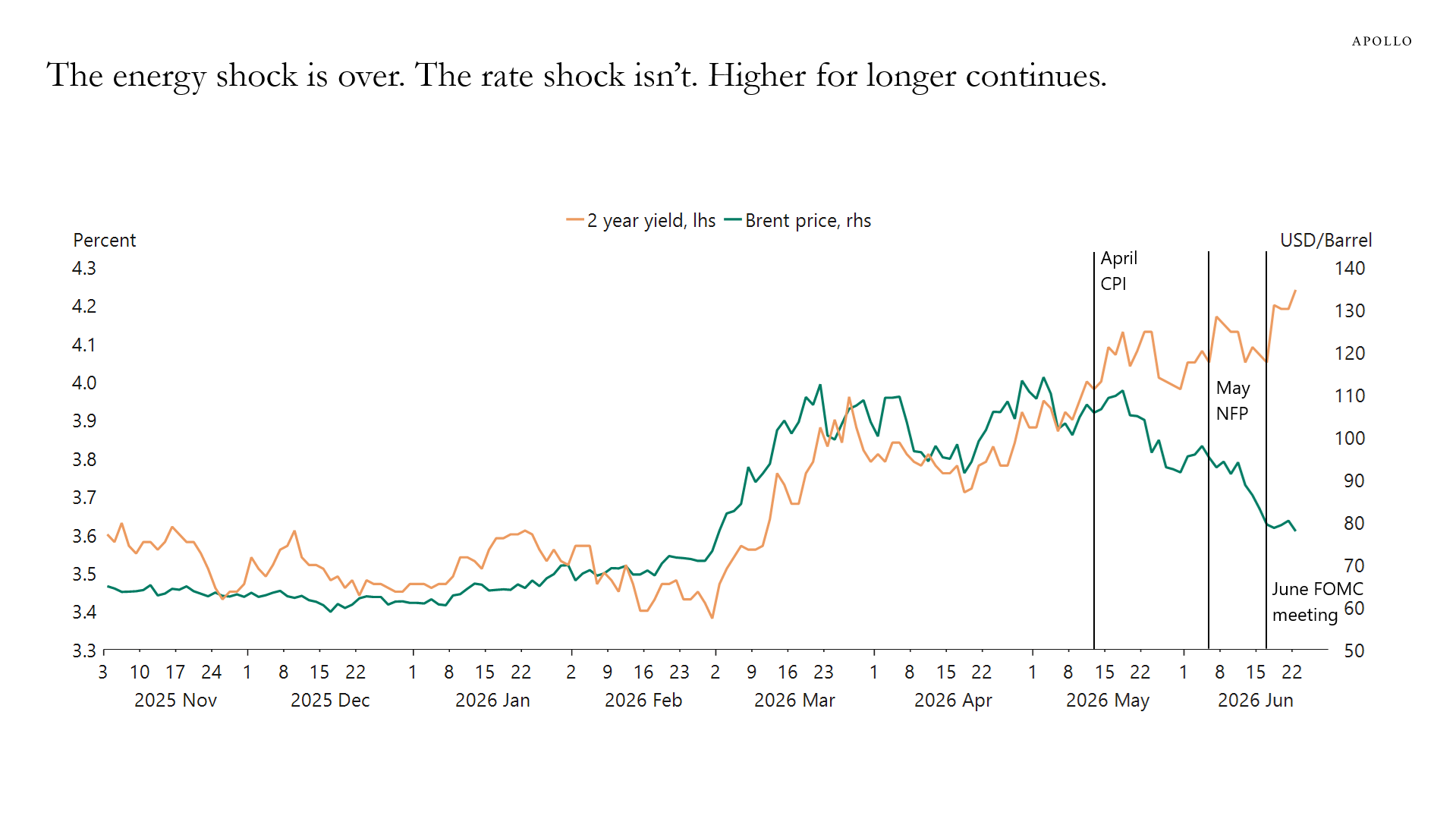

“The energy price shock is over, but the interest rate shock is not.” The yellow line shows the two-year bond yield and the green line shows the price of a barrel of Brent oil in dollars. The two initially moved together, but have diverged since the April inflation figures (CPI). (Source: Apollo).

Even a declining oil price seemed to have little effect on inflation expectations and the gold price after that. The United States and Iran are still in their 60-day period to reach a definitive peace agreement, with shipping through the Strait of Hormuz now resumed. It seemed logical that lower oil prices would reduce inflation expectations. In recent days, however, nothing appeared further from the truth. Despite reports that we may now even be facing an oil surplus, markets are seeing a new risk. Rapidly falling oil prices could unexpectedly stimulate the economy, while that economy is already overheated, writes Torsten Slok of Apollo.

Kevin Warsh at the ECB Forum on 1 July 2026. Photo: Sérgio Garcia/Your Image for ECB, © European Central Bank 2026. (Source: ECB).

On 1 July, Warsh spoke at the ECB Forum, his first public appearance since the rate decision. "Inflation expectations over the first four weeks of this period have declined, inflation risks have fallen," Warsh said, to everyone’s surprise. At the same time, he reiterated that the Fed is determined to bring inflation back to its 2% target. Nevertheless, markets appeared to interpret his remarks as pointing to lower interest rate expectations. This time, the two-year bond yield did fall after his comments.

That same day brought disappointing private-sector jobs figures (ADP) from the US and better-than-expected inflation figures in the EU. Whereas 122,000 jobs were added in the United States in May, that figure had fallen to 98,000 in June. A weaker labour market increases the likelihood that the Federal Reserve will raise interest rates more slowly, or even cut them sooner. In addition, inflation in the eurozone appears to have fallen from 3.2% to 2.8% as energy prices decline again. Lower inflation makes it less necessary for central banks to raise interest rates. Is the same thing happening in the US? If so, that is positive for gold.

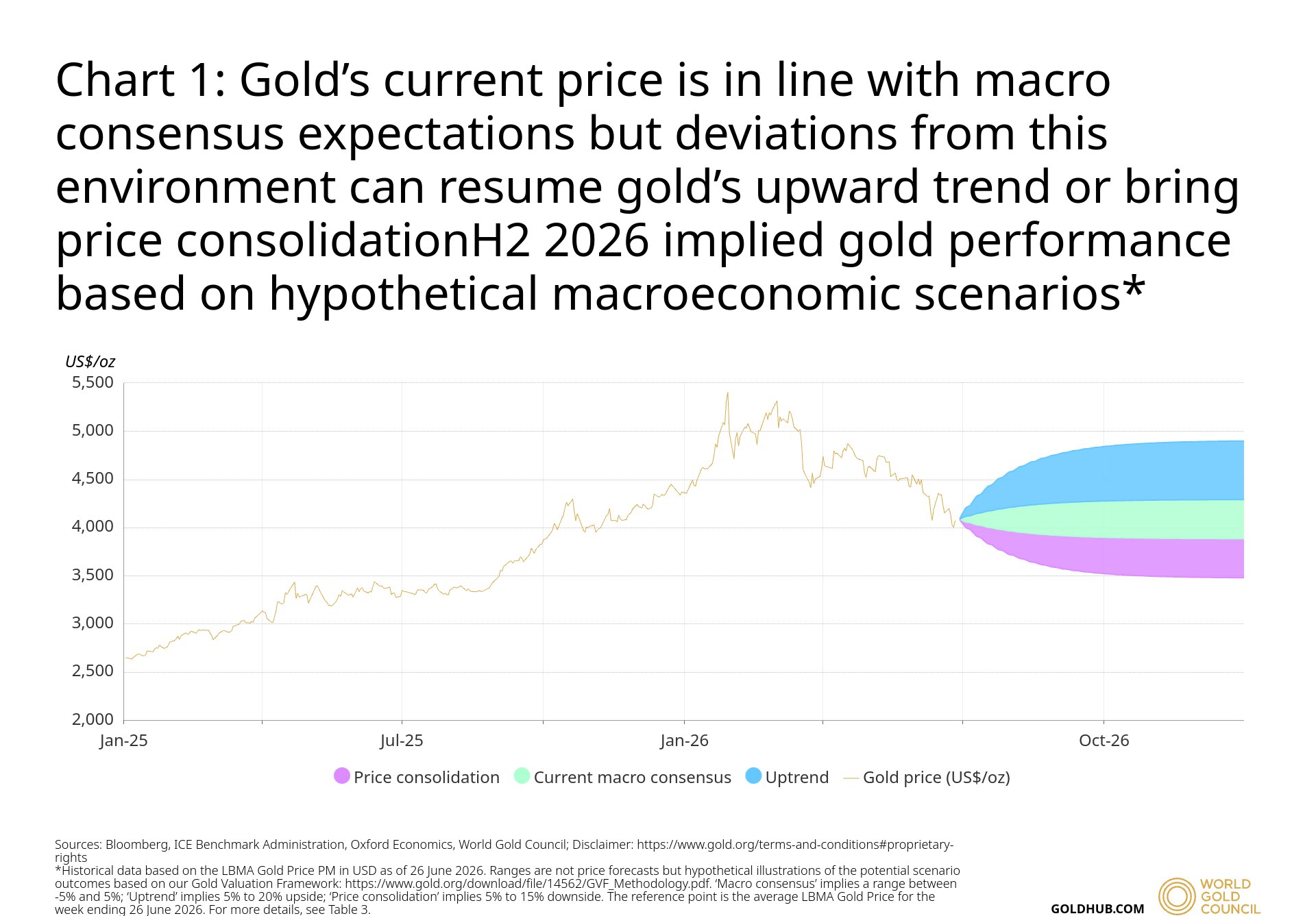

On 1 July, gold surged by 3.1% from the lowest point of the trading day, apparently in response to Warsh’s remarks and the new data. Markets are now waiting for new developments that could substantially alter interest rate expectations. According to the World Gold Council, gold needs a new catalyst to push the gold price back towards $4,500 per ounce and beyond.

Various scenarios for the gold price. Green represents the current macroeconomic consensus. Purple represents further price consolidation if gold faces more headwinds. Blue represents a new upward trend, for example if interest rate expectations change. (Source: World Gold Council).

Central banks hold reserves as a financial buffer for uncertain times, to support their own currency in foreign exchange markets and to provide the country with liquidity for foreign obligations in times of market stress. For that reason, central banks hold dollar reserves, including in the form of US Treasury bonds.

Gold is a crucial complement within those reserves. On the one hand, this is because countries retain full control over it by storing the physical gold in their own vaults. On the other hand, it is very easy to sell for dollars or another currency. In an era in which the dollar can be used as a weapon, countries are in a stronger position when they hold gold. After the invasion of Ukraine, Russia was cut off from the international payments system. Thanks in part to its gold reserves, the country was nevertheless able to continue trading with other countries.

Gold is also the perfect buffer during market stress. Recently, the Turkish central bank sold part of its gold reserves to support its own currency. Turkey is largely dependent on oil imports for its energy needs, and rising oil prices put the country in difficulty and sent the Turkish lira tumbling.

This shows why countries that expect geopolitical risks buy gold. These often include countries from emerging markets, such as China, Turkey and Russia, but also, for example, Poland.

Be sure to also check out our YouTube channel

On behalf of Holland Gold, Paul Buitink and Yael Potjer interview various economists and experts in the field of macroeconomics. The aim of the podcast is to give viewers a clearer picture and a firmer footing in an increasingly fast-changing macroeconomic and monetary landscape. Click here to subscribe.