9.3

8.889 reviews

English

EN

Gold and silver have once again gained a prominent place in the investment debate in recent years. Both retail and institutional investors are increasing their allocation to precious metals, primarily to hedge risks stemming from high government debt, low real interest rates and persistent inflation. This shift toward scarce assets is known on Wall Street as the debasement trade. But why is this strategy attracting so much attention now and what role do gold and silver play in it?

Gold has risen exceptionally over the past five years, gaining 170 percent. According to JP Morgan, this increase is mainly attributable to declining real interest rates, meaning the return earned after adjusting for inflation. Gold becomes attractive when the value of money is eroded by factors such as inflation.

A classic example is the denarius, the Roman silver coin. Emperors structurally reduced the silver content of the coin and replaced it with copper to finance high war expenditures. The debasement became so severe that the silver percentage fell from 98% to less than 5%. The result was persistent and rising inflation, ultimately contributing to an implosion of the economic system alongside hyperinflation. The debasement trade therefore represents a shift away from currencies and bonds toward hard money to mitigate the risk of currency debasement.

Figure 1: Gold price versus real interest rates. (Source: J.P.Morgan)

The importance of gold is increasingly recognized by institutional investors. In 2019, economist Mathijs Bouwman argued that De Nederlandsche Bank would be better off selling its gold reserves because they supposedly had no value in the modern monetary system. Today, however, the CIO of Morgan Stanley argues that the traditional 60/40 portfolio of stocks and bonds is outdated. He advocates a 60/20/20 allocation with 20 percent in gold, citing its effectiveness as a hedge against inflation and particularly against negative real interest rates, which have become a growing risk.

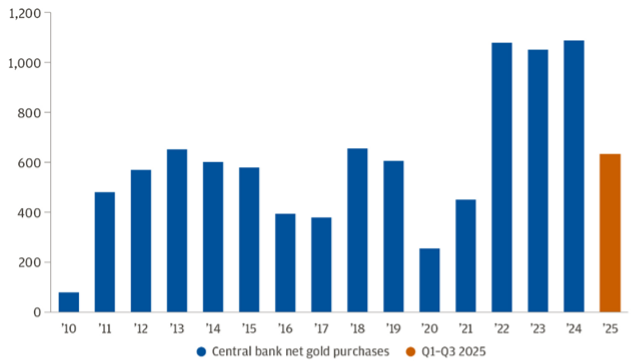

Central banks have always maintained gold reserves. De Nederlandsche Bank describes gold as an anchor of trust: while modern money is made from inexpensive materials, gold historically provided a sense of underlying value. Even after the link was abandoned, gold never lost this role. Purchases of gold by central banks clearly demonstrate their continued confidence in the metal. Since 2010, net purchases by these institutions have risen significantly, doubling from 2022 compared with previous years.

Figure 2: Net central bank purchases. (Source: J.P.Morgan)

The shift toward scarce assets intensifies as fears of currency debasement grow. These concerns are fueled by steadily rising government debt levels. The Netherlands, long considered a benchmark for fiscal discipline, is projected by the CPB to reach a debt-to-GDP ratio of 126% by 2060. This increase is attributed to higher spending on pensions and healthcare. Because raising taxes is politically unpopular, additional revenues fail to offset rising expenditures, leading to higher debt levels.

To finance these deficits, governments issue bonds. Investors, however, increasingly demand higher yields to compensate for elevated default risk. To prevent borrowing costs from rising too sharply, central banks implement Quantitative Easing (QE) by purchasing government bonds before they reach capital markets. This reduces supply and helps keep government borrowing costs lower.

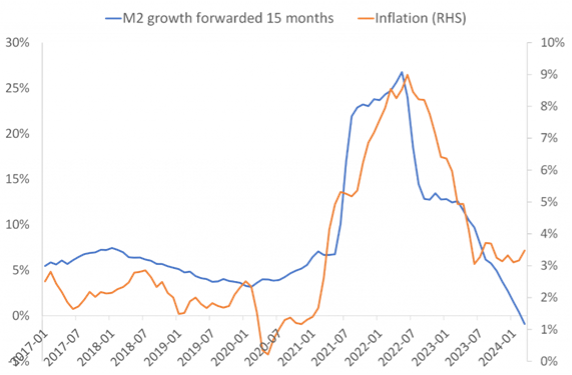

The major drawback of QE and money creation by central banks is inflation. As the money supply expands, its value declines through inflation. During the pandemic, the Federal Reserve injected massive liquidity into the economy. The money supply surged in a short period, resulting in persistent inflation and eroded dollar purchasing power. Because central banks target inflation around 2% while relying on low rates and monetary expansion that increases money supply, currency purchasing power tends to come under pressure over time. This is especially true when inflation persistently exceeds returns on savings and bonds.

Figure 1 Money supply growth and inflation correlation. ( Source: St. Louis FRED and J. Rangvid.)

Since the abandonment of the gold standard in 1971, governments and central banks have generated more inflation through artificially low interest rates and money creation, reducing the value of currencies. Hard money, by contrast, derives scarcity from limited supply, meaning no central authority can simply create more of it. As a result, it better preserves value.

Producing hard money also requires effort. Extracting gold from the ground is a physical process involving significant labor and capital, which supports its credibility and perceived value as money. When money is inexpensive to produce, the incentive to create more becomes extremely strong.

Gold and silver are both extremely scarce: all the gold ever mined would fit into a cube measuring roughly 22 by 22 meters. Mining these precious metals requires substantial labor and capital, reinforcing their credibility. In a world where currencies often yield negative real rates and purchasing power is eroded, gold and silver, along with digital scarce assets such as Bitcoin, can serve as a hedge against debasement.

The debasement trade gains momentum particularly in environments characterized by low real interest rates, rising debt and accommodative monetary policy. When confidence in a currency remains strong and real rates are positive, the need for such protection typically diminishes. This interplay explains why gold and silver play a central role in portfolios during certain periods while fading into the background in others.