9.2

8.853 reviews

English

EN

It is code orange for the financial system, according to the risk analyses presented by both DNB and the CPB to the House of Representatives. Geopolitieke and economic risks are omnipresent across these reports, with specific emphasis placed on the dangers surrounding AI, private credit, and the French national debt. Meanwhile, gold is moving sideways, but these dark clouds present a compelling reason to safeguard one's equity with physical precious metals.

The Centraal Planbureau (CPB) and De Nederlandsche Bank (DNB) do not mince words in their respective publications. Using unusually blunt language, they expose the severe risks facing our financial framework. According to DNB, it is even a "code red" scenario regarding geopolitical tensions, cyber threats, and the sudden risk of a major stock market crash; whereas mounting sovereign debts, private credit, and rising interest rates currently sit under "code yellow".

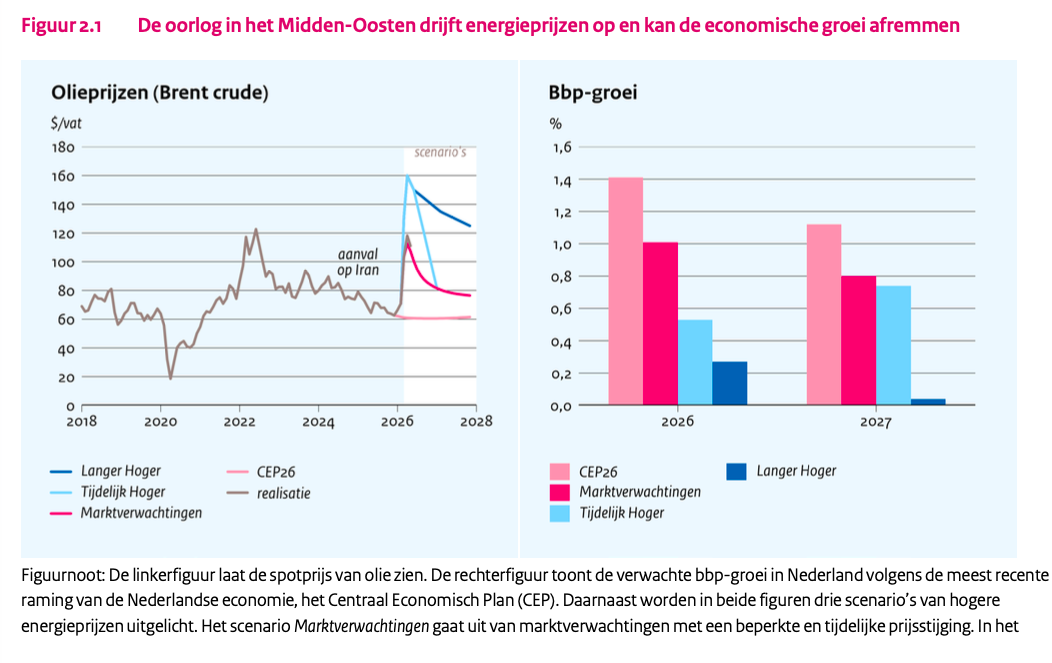

Various scenarios demonstrate that the longer oil prices remain elevated, the less room is left for Dutch economic growth. (Source: CPB)

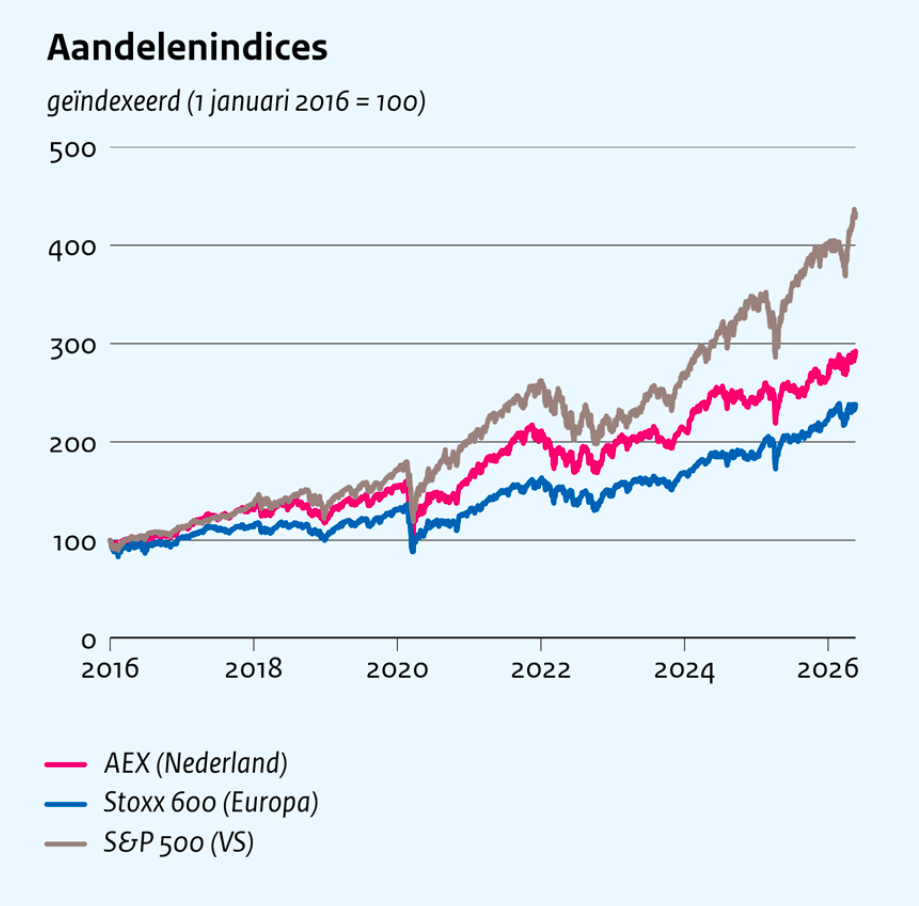

Now that an extension of the ceasefire between the United States and Iran appears to be a done deal, global stock markets are bouncing back higher. US indices are pushing back toward all-time highs while traders await the precise framing of a peace treaty that could structurally reopen the Strait of Hormuz.

US stock markets are climbing to fresh records, consistently outpacing European bourses over the past decade. (Source: CPB)

According to reports from DNB and the CPB, however, the stellar performance of US equities is completely decoupled from global economic uncertainty. Multiple uncertainty indexes are hitting historical peaks, even as the VIX index—measuring financial market nervousness—remains at a baseline average. High stock market valuations are holding ground solely because investors expect sustained, AI-driven corporate earnings growth.

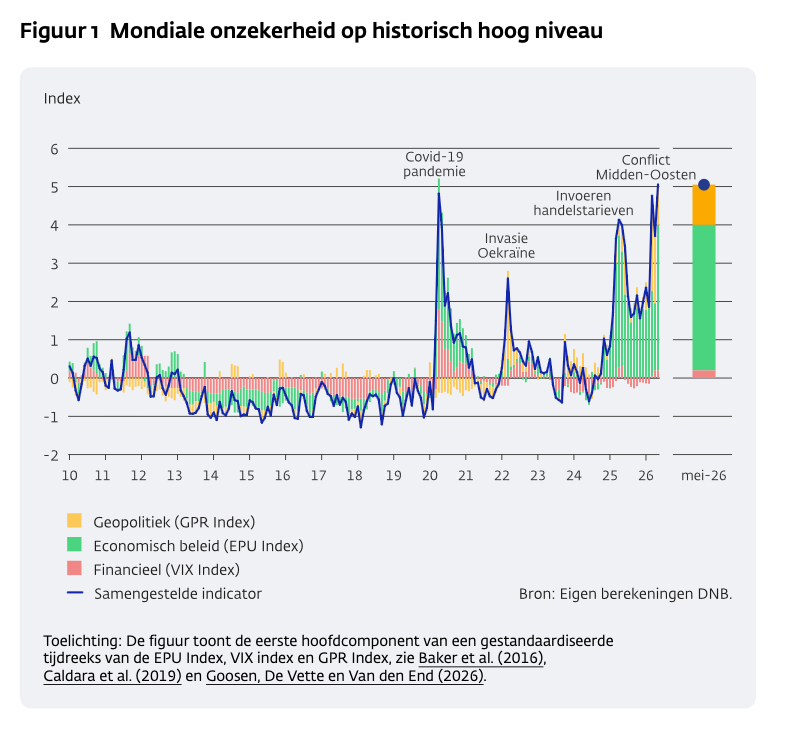

DNB integrated the EPU Index, VIX Index, and GPR Index to demonstrate how mathematical aggregates of global uncertainty are once again peaking. (Source: DNB)

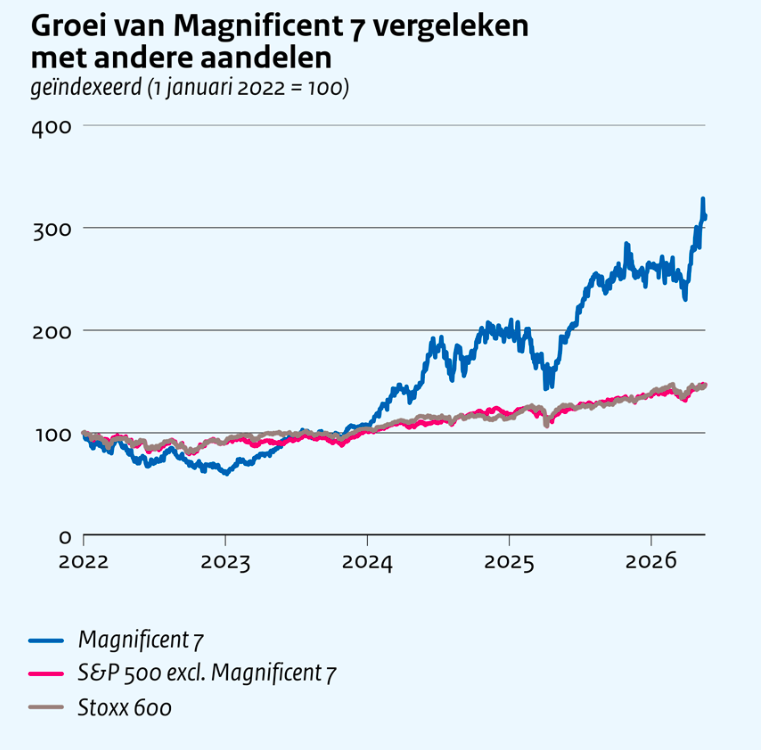

Recently, Bank of America market strategist Michael Hartnett warned of an escalating bubble in the tech sector, amplified by massive upcoming public offerings from mega-firms like SpaceX and OpenAI. The tech space already commands 44% of the aggregate S&P 500 market valuation. These upcoming listings could easily push index concentration past the dangerous thresholds (~48%) witnessed during the bubbles of the Roaring Twenties or the late 1990s dot-com era.

The absolute dominance of US equity markets is almost exclusively driven by the "Magnificent 7" (Nvidia, Google, etc.), perfectly highlighting the extreme concentration in tech stocks. (Source: CPB)

The CPB notes that investors are drastically underpricing extreme tail risks in their valuations, which could trigger sharp, systemic declines the moment market sentiment turns.

Private credit consists of a closed ecosystem of corporate loans that are not traded on public exchanges. These debt instruments are not underwritten by commercial banks, but rather by institutional players like insurance companies and pension funds, issued either directly or via specialized funds.

With any corporate loan, there is an inherent risk of default or structural distress. Because of private credit's opaque, bespoke nature, regulators lack granular visibility into underlying asset quality. This creates widespread concern that private credit could spark a hidden financial crisis, echoing the subprime collapse of 2008.

According to an analysis by the ECB, private credit losses present a more direct threat to pension funds and insurers than to traditional commercial banks. Widespread European insurers and pension funds have deployed billions into this segment—holding €211 billion and €52 billion, respectively. At the broader European level, private credit represents 2.3% of the total assets managed by insurers. According to data from DNB, this concentration sits significantly higher in the Netherlands, where private credit commands up to 8% of Dutch insurers' total assets under management.

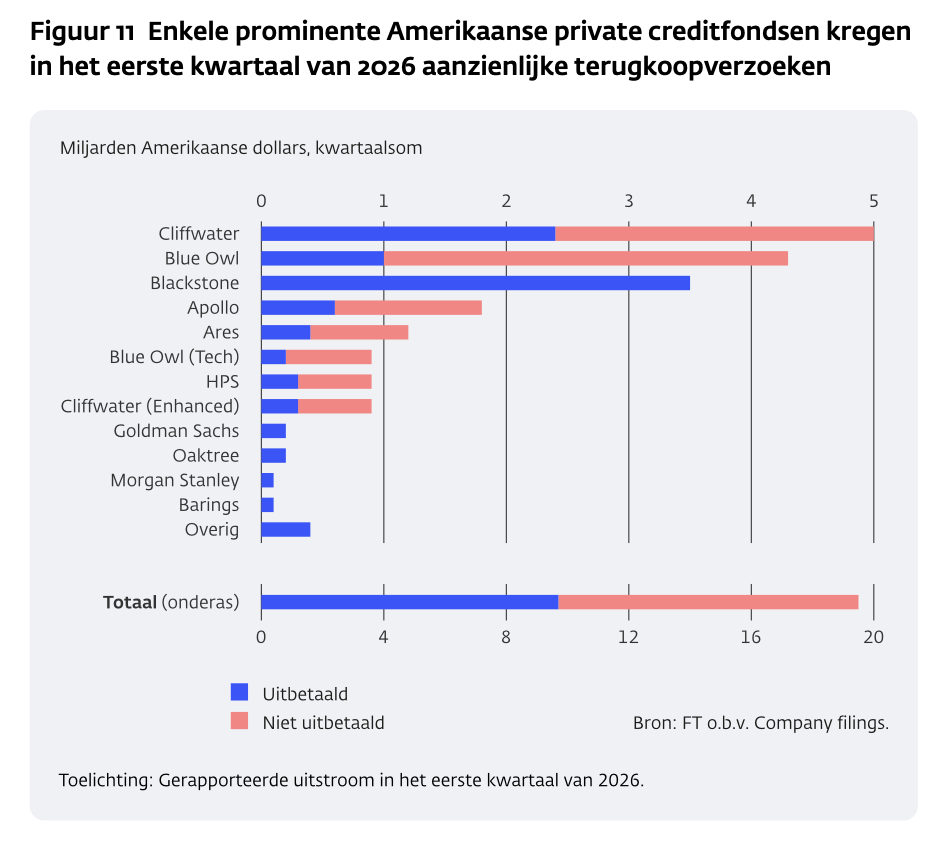

In recent months, private credit has faced intense scrutiny due to its arguably disproportionate exposure to the software sector. This setup could trigger synchronized losses if the profitability of traditional software-as-a-service (SaaS) companies is disrupted by the rise of new AI applications. This vulnerability recently sparked minor panic, hitting private credit vehicles with substantial redemption requests that could not be fully liquidated. This confirms that these debt instruments suffer from strict liquidity constraints during periods of market stress.

Billions of dollars per private credit fund that investors attempted to liquidate in Q1 2026. (Source: DNB)

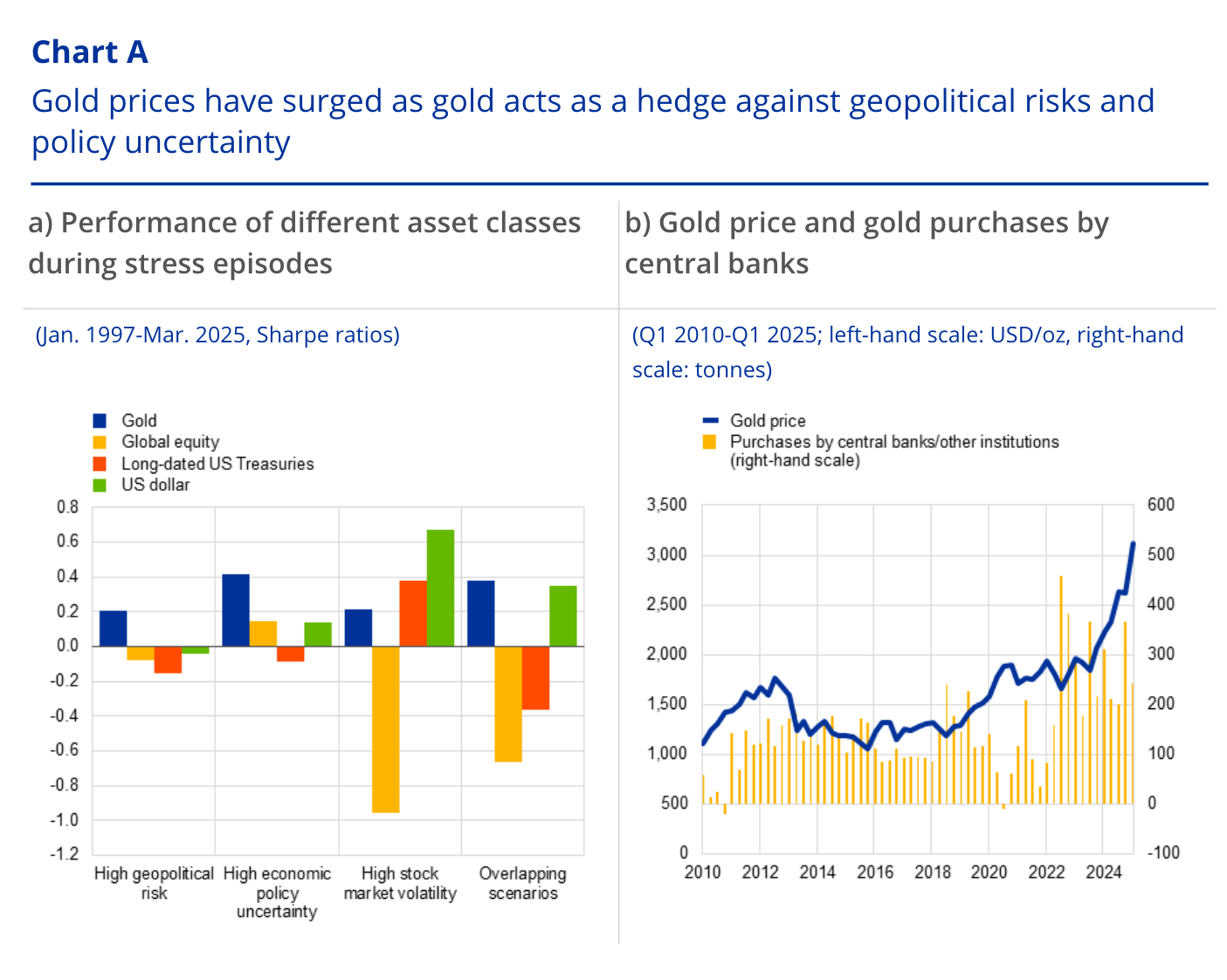

Historically, gold has served as the premier safe haven during phases of financial and geopolitical instability. ECB research confirms that gold performs exceptionally well amid compounding geopolitical risks, economic policy uncertainty, and massive equity market volatility. Regarding the latter, the 2008 financial crash remains a text-book example: while the S&P 500 shed up to 55% of its value, gold rallied aggressively, trading 166% higher by 2011.

Left: A chart tracking how gold (blue) performed over the past 30 years relative to traditional asset classes: equities (yellow), government bonds (red), and the US dollar (green) across various stress scenarios. Right: A chart mapping gold price development alongside central bank gold accumulation. (Source: ECB).

The latest reports from DNB and the CPB point to severe structural threats to the financial system, driven by geopolitical friction, economic policy volatility, sovereign and corporate debt overhangs, and digital security risks targeting institutional infrastructure. These represent the exact macro-economic catalysts that visually validate gold's safe-haven status.

Gold is a physical asset that an investor holds with absolute title and zero counterparty risk—completely free from the banking system. It can be held in direct private possession or via specialized, AFM-licensed vaulting facilities. Consequently, it contains zero exposure to commercial banks prone to insolvency during financial, sovereign, or systemic crises. With the financial landscape operating under a confirmed "code orange," diversifying a portfolio with physical gold appears more essential than ever.