9.2

8.874 reviews

English

EN

As of January 1, 2028, the Netherlands plans to become the first country in the world to introduce a broad-based tax on accrued wealth gains. Under this system, investors will be taxed annually on increases in the value of their assets, even if those gains have not yet been realized. The proposal has attracted criticism both domestically and internationally. The Dutch Council of State warned about the significant administrative burden, while Tesla CEO Elon Musk argued that such a tax could discourage startups and drive talent elsewhere. At the same time, rulings by the Dutch Supreme Court rendered the current deemed-return system unsustainable. What exactly will change in 2028, and why has the new regime sparked so much debate?

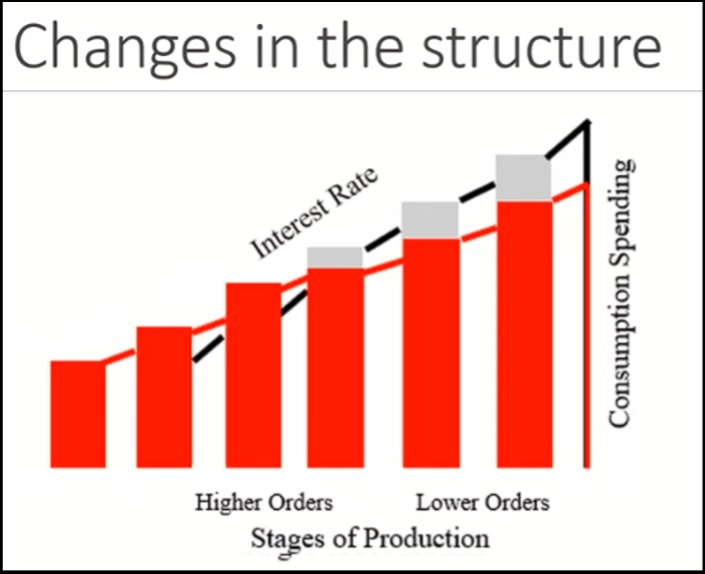

To understand why the new system is so controversial, it is important to first examine the economic function of capital. Saving is essentially the act of postponing consumption. Imagine Robinson Crusoe stranded on a deserted island. To satisfy his hunger, he spends ten hours each day gathering berries. He could make a bow and arrow to obtain food more efficiently, but producing these tools would require thirty hours of labor. To make this investment possible, he must first save enough food to sustain himself while building the bow. By temporarily reducing consumption, he can invest in productive assets that increase his future output.

This principle forms the foundation of capital formation. People who save postpone consumption and thereby make investments possible that increase productivity. In return, they earn a return on their capital. The more people save, the more resources become available for long-term projects that only generate consumer goods in the future. These investments are often responsible for higher consumption, greater prosperity, and lower prices over the long run. As a result, the way wealth is taxed can significantly influence the amount of capital available for future investment.

Higher savings (red) lead to higher future consumption.

The current Box 3 regime came under pressure because taxpayers were required to pay tax on returns they had not actually earned. As a result, the Netherlands will move to a taxation system based on actual returns from 2028 onwards. The new legislation, which has already been approved by the House of Representatives, introduces a broad accrued gains tax.

Under this system, not only income such as dividends and rental income will be taxed, but also annual increases in the value of investments, even if those gains have not yet been realized. Real estate, such as second homes and investment properties, as well as shares in startup companies, are exempt from this treatment. These assets will instead be subject to a capital gains tax, meaning tax is only due when the gain is actually realized.

The transition to actual-return taxation will also abolish the current tax-free wealth allowance. In its place, taxpayers will receive a tax-free return allowance of €1,800 per fiscal partner. Returns exceeding this threshold will be taxed at an expected rate of 36%. In addition, losses exceeding €500 can be carried forward and offset against future positive Box 3 income.

Because the proposed Box 3 regime faced significant criticism, the Dutch Senate consulted various experts regarding the consequences of the accrued gains tax.

The Council of State issued a critical report on the proposal and warned about its practical implementation for both taxpayers and the Dutch Tax Administration. The system becomes substantially more complex because taxpayers must calculate annual returns for each investment and keep detailed records of costs and deductions. According to the Council of State, the proposal places a considerable burden on citizens' ability to comply with tax rules. The Council also warned about deteriorating public services, limited opportunities for consultation with the tax authorities, and insufficient oversight.

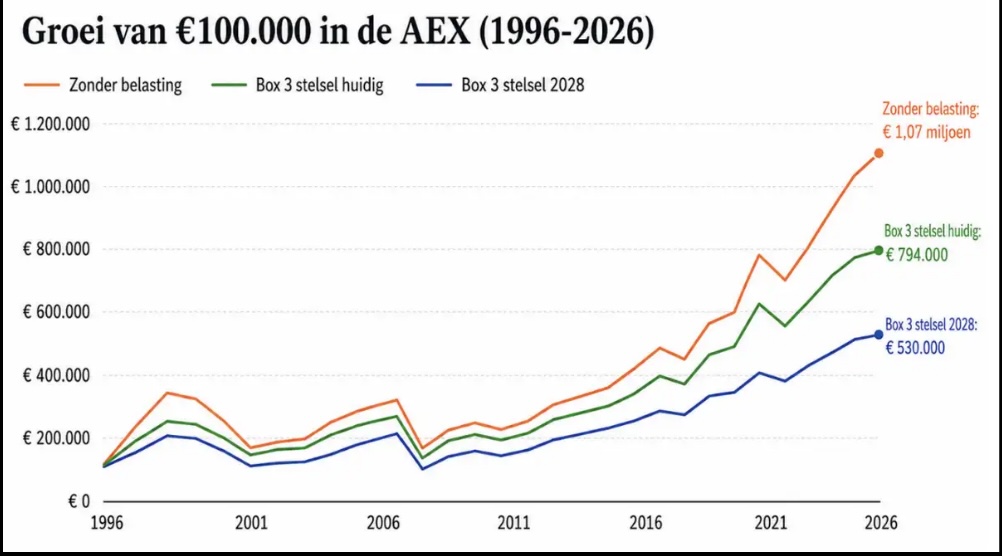

Employer organization VNO-NCW has also voiced criticism and advocates replacing the accrued gains tax with a traditional capital gains tax. According to the organization, taxing unrealized gains annually undermines the power of compound returns, resulting in lower wealth accumulation and less capital available for investment over time. Although a capital gains tax would initially generate less tax revenue, VNO-NCW argues that over a thirty-year period it could ultimately produce approximately one-third more revenue.

Difference in wealth growth under the new Box 3 regime. (Source: StockWatch)

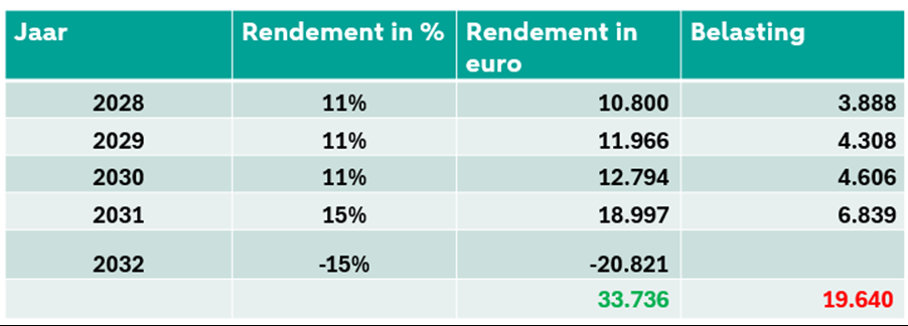

Another frequently raised concern relates to the treatment of losses. If an investor generates gains over several years and pays tax on those gains, but subsequently suffers a significant market decline, those losses cannot be offset against taxes paid in previous years. Losses may only be carried forward against future positive returns. As a result, less capital remains available to benefit from a recovery, and the effective tax burden can become substantially higher than the nominal 36% rate.

Supporters of the accrued gains tax argue, however, that a capital gains tax has disadvantages of its own. If tax is only due upon sale, investors have an incentive to delay realizing gains for as long as possible. This allows taxes to be deferred for many years, significantly reducing the effective tax rate. Furthermore, a capital gains tax may encourage investors to favor assets that pay little or no income, solely to postpone taxation.

Although the debate surrounding Box 3 may appear to be primarily a tax issue, capital formation and investment play a crucial role in economic growth and future innovation. With the introduction of the accrued gains tax, unrealized gains will become taxable from 2028 onwards. Various organizations and experts have criticized the system due to concerns about administrative complexity, wealth accumulation, and the treatment of losses. On the other hand, a capital gains tax also has drawbacks, as it allows investors to defer taxation and may encourage investment in assets that generate little or no current income.

At a time when the Netherlands is advocating for a stronger European Capital Markets Union to stimulate investment and economic growth, the new Box 3 regime raises a broader question: does Dutch tax policy risk encouraging the opposite?