9.3

8.666 reviews

English

EN

The gold price is once again trading well above €140,000 per kilo this week, marking a strong recovery after the dip earlier this month. As a result, gold now appears set to close the month of February with a return of more than six percent. Was the recent decline merely a temporary interruption, and is the gold price already preparing to reach new record highs?

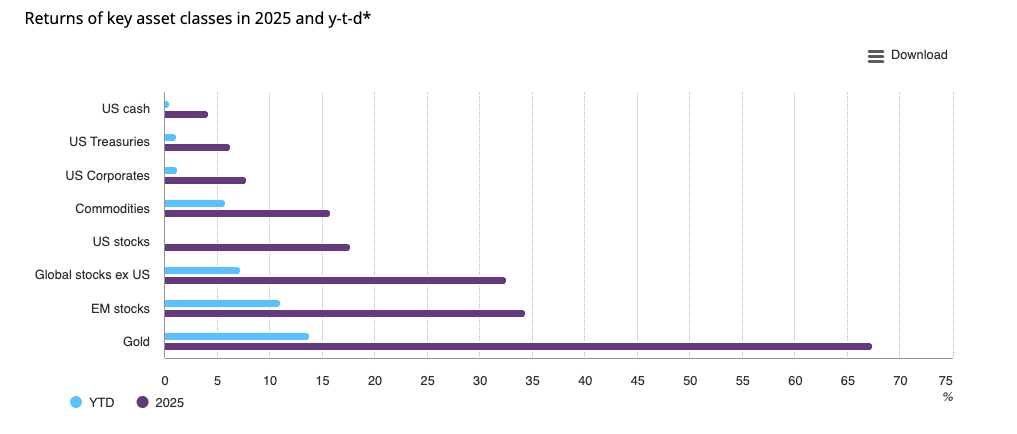

Gold returns in 2025 and in 2026 (until February 17) in US dollars (source: World Gold Council)

Gold returns in 2025 and in 2026 (until February 17) in US dollars (source: World Gold Council)

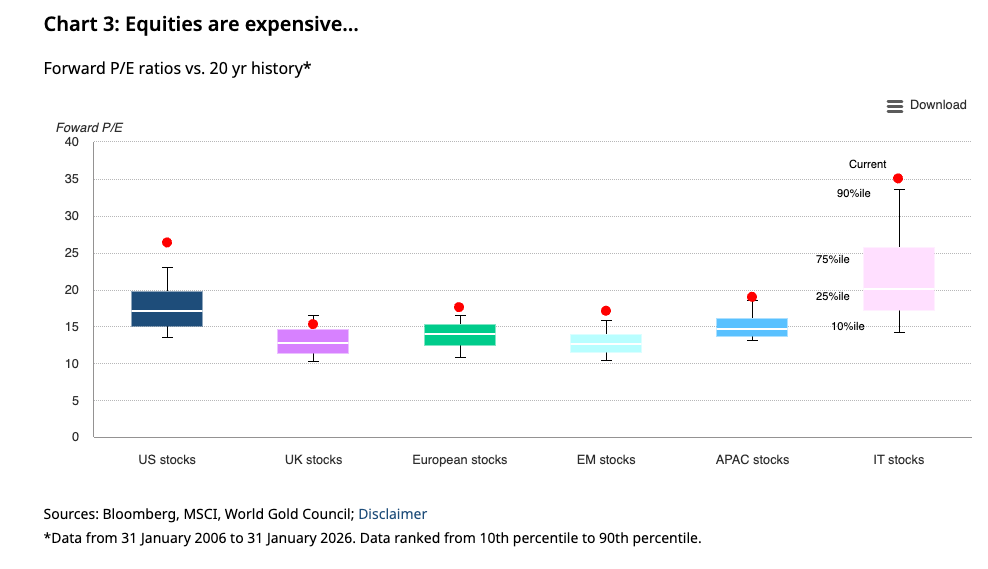

The World Gold Council (WGC) published a new article this week titled ‘Why Gold in 2026?’. According to the WGC, risk assets are sitting at uncomfortable highs while the world is increasingly characterized by unrest and uncertainty. The WGC notes that equities are historically expensive when measured by forward P/E ratios, which currently stand at very elevated levels compared with the past twenty years.

Equities are expensive according to the WGC; the red dot indicates the current situation (source: World Gold Council)

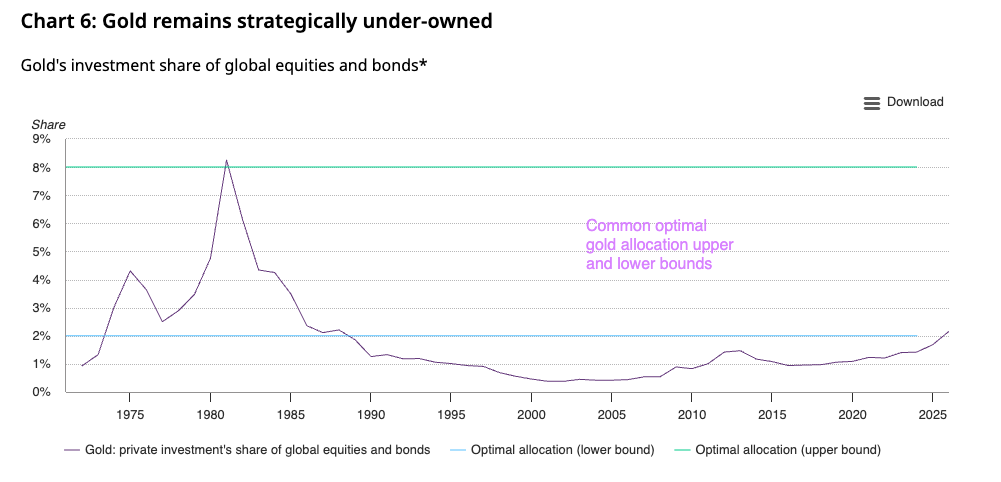

According to the WGC, an important driver behind the rise in the gold price is the ‘concerning’ gap between the strong level of certainty with which markets price in their economic outlook and the exceptionally high level of economic policy uncertainty. The WGC also states that gold remains underrepresented in investment portfolios.

The share of gold investments relative to global equities and bonds (source: World Gold Council)

Given the geopolitical environment and expectations of further monetary easing, the WGC believes gold deserves a larger role in investment portfolios. The organization warns of rising inflation risks, as an expected fiscal stimulus could further boost economic demand while little spare capacity remains in the U.S. economy. If this forces the Federal Reserve to raise short-term interest rates, it could put pressure on gold prices in the short term due to higher opportunity costs, but support gold over the medium and long term through stronger demand for inflation protection.

According to the WGC, rapidly rising U.S. margin debt points to increasing financial speculation and growing risks. Investors are borrowing more to buy equities, which after a long rally and elevated valuations increases the likelihood that disappointing earnings results could trigger a sharp correction.

“After a long rally, with valuations approaching dot-com levels, a few missed earnings expectations could be enough to undermine confidence. This could lead to an unwinding of investor leverage positions, potentially increasing downside risks for equity prices and boosting demand for safe-haven assets, notably gold,” the WGC states.

Goldman Sachs also believes gold could continue to rise in 2026. The U.S. investment bank writes that, amid growing uncertainty, investors are increasingly turning toward hard assets, with gold and copper particularly well positioned to benefit from this trend.

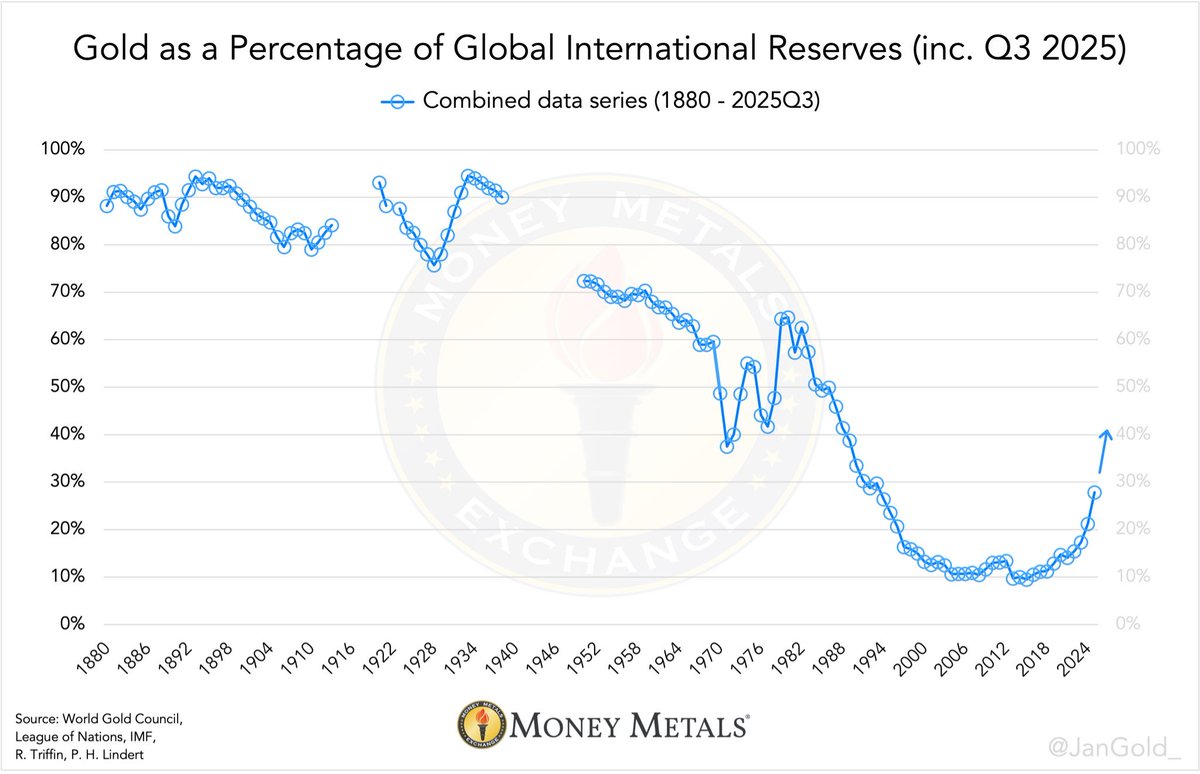

Gold as a percentage of international reserves (source: Jan Nieuwenhuis)

According to Goldman Sachs, demand for gold is supported not only by central bank monetary policy but also by continued gold purchases as central banks further diversify their reserves. The bank expects the gold price to rise to $5,400 per ounce by the end of this year, while noting there remains significant upside potential, as additional demand from private investors has not yet been incorporated into this forecast. Because the gold market remains relatively small compared with equity and bond markets (see WGC chart), additional capital inflows could provide a strong upward impulse to gold prices.

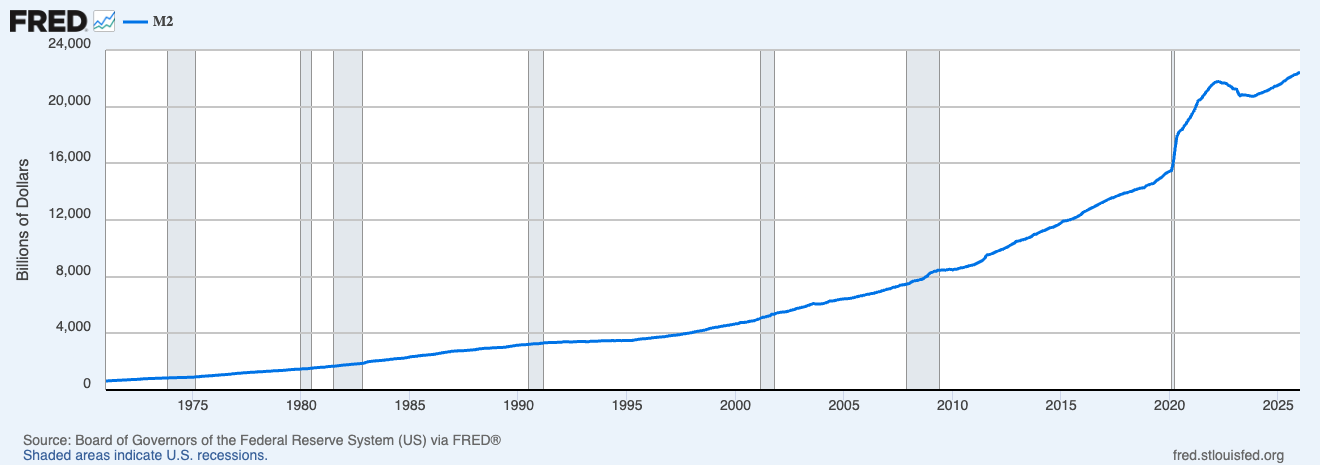

The U.S. M2 money supply rose to a new all-time high of $22.4 trillion in January 2026. The recent increase shows that more liquidity is once again entering the economy after a period in which money supply growth had been restricted. This could push inflation expectations higher, strengthening demand for gold as protection against currency debasement.

U.S. M2 money supply (source: FRED)

Jeroen Blokland notes that money supply in the eurozone also increased by 3.3 percent in January, the fastest pace in six months. He observes that money supply growth is accelerating in other parts of the world as well.

According to Jack Hoogland, everything ultimately comes down to one crucial question: will liquidity flow out of financial markets in the period ahead, or will it once again move back into them? For now, the latter scenario appears far more likely, suggesting the debasement trade could continue in the months ahead.

Based on the analyses and expert views above, the February correction appears to have been merely a pause within an ongoing upward trend. Underlying signals continue to point toward further gains in the gold price.

Also take a look at our YouTube channel

On behalf of Holland Gold, Paul Buitink and Yael Potjer interview various economists and macroeconomic experts. The goal of the podcast is to provide viewers with better insight and guidance in an increasingly fast-changing macroeconomic and monetary landscape. Click here to subscribe.