9.3

8.524 reviews

English

EN

'The ECB will start its bond-buying programme this month', reads the headline of an article in Trouw on 3 October 2014. It is the announcement of unconventional monetary policy under the name of Quantitative Easing, QE. At the time, it was thought that this program would only last 2 years, but in fact the ECB has not really stopped quantitative easing since then. Just a few months into 2019, the bankers in Frankfurt tried to stop the policy, but it soon became apparent that the program had to go ahead again.

Now, with the current inflation figures, it seems that QE should come to an end once and for all and even monetary tightening is being discussed. In the case of tightening, the central bank shrinks the balance sheet and that is called Quantitative Tightening, QT. How will the markets react to this and what can we expect from QT?

Quantitative Easing

In recent years, central banks around the world have been buying bonds. In fact, it is an asset swap for banks, which receive reserves in exchange for the bonds. As a result of this purchase policy, interest rates fall and that stimulates borrowing. Although, according to the ECB, this policy has been necessary in recent years to create good financing opportunities, it has also caused bad blood among many critics.

According to opponents, it led to a huge growth in real estate prices and to bubbles in financial markets. Due to high inflation, central banks have started to taper their asset purchase policies. That will be Tapering said. It does not mean that a central bank will no longer buy bonds, but only that fewer bonds will be bought than before. Compare it to a smoker who smokes 'only' eight cigarettes a day instead of ten. In addition to the Tapering interest rates will also be increased incrementally. So the ECB announced that on 8 September, a rate hike of 0.75%.

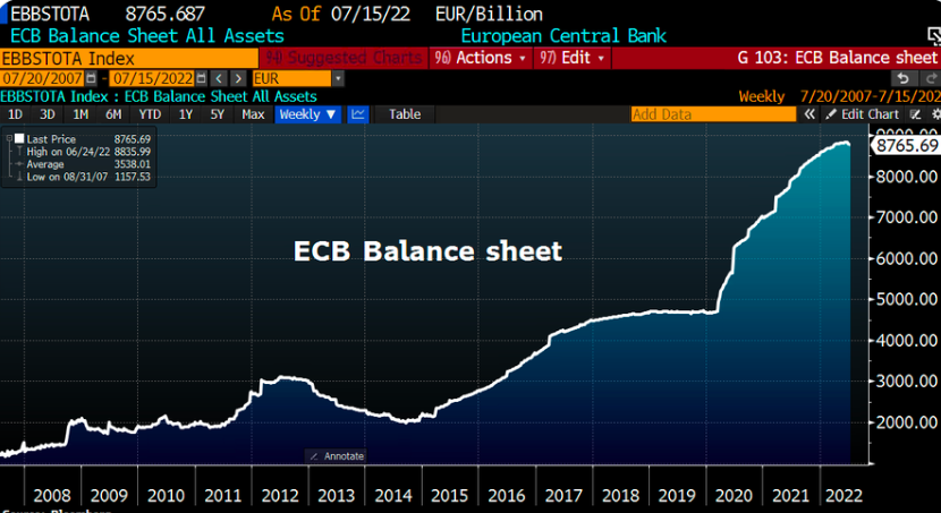

The size of the ECB's balance sheet in recent years (Source; Holger Zschaepits)

Quantitive Tightening

However, the ECB's policy rate mainly affects the interest rate on the money market, the market for short-term loans. Interest rates on the capital market, the market for long-term assets, depend on many more factors and are therefore less sensitive to the ECB's policy rate. Nevertheless, QT can help push up capital market interest rates. This can be done in two ways. For example, the ECB can choose not to reinvest the proceeds of the bonds it purchased.

If the central bank stops buying bonds, there will be less demand for bonds. That should cause interest rates to rise. As soon as a bond is redeemed, it disappears from the balance sheet and so money disappears from the economy. With less money circulating in the system, inflation could also be lower, at least that is the intention. In order to counter interest rate differentials within the euro area, the ECB invests in The proceeds of the repaid bonds are now in debt securities of countries with high public debts. There is a chance that the ECB will continue to reinvest part of it in the near future, as interest rates in countries such as Italy are rising much faster than interest rates in the Netherlands, for example.

A more aggressive form means that central banks will put the bonds they have on their balance sheets back on the market. They can do this, for example, by exchanging the bonds at commercial banks for reserves, which reduces the money supply. In this way, liquidity is extracted from the market even faster. The FED, the U.S. central bank, has already stopped reinvesting the proceeds of bonds, with which the Fed hopes to increase the balance sheet by 95 billion dollars per month in the months of September and October downsize. If that is not enough, the Fed could be even more aggressive by actively selling different types of bonds, such as government bonds and mortgage loans.

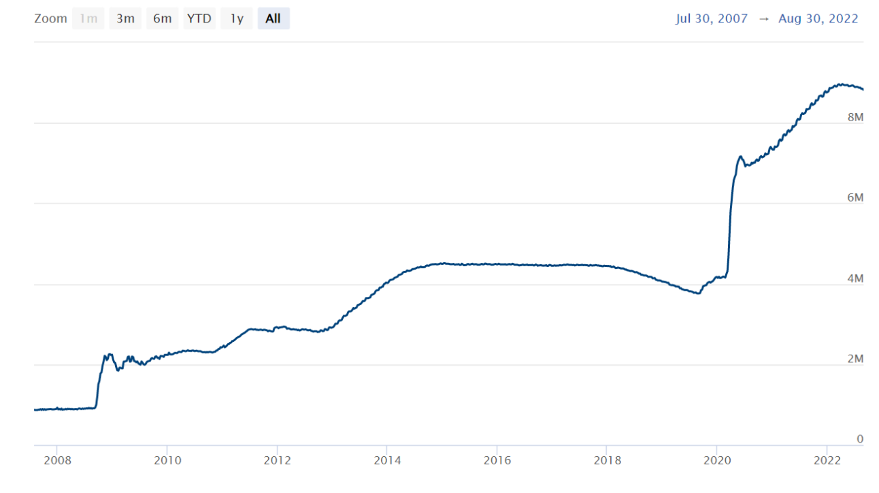

The interesting thing is that no one really knows for sure what the effect of such an aggressive policy will be. The Fed has tried to reduce the balance sheet before. That policy started in 2018, but had to be stopped in 2019, as banks no longer had enough reserves, causing panic in the repo market. Therefore, the Fed stepped into the market and then the balance sheet rose in size again, as the chart below shows.

In America, however, this is not expected to happen again. Not only are there now many more reserves in the system due to the large amount of money that has been pumped into the system since the corona crisis, the Fed now also has a new instrument up its sleeve; the Standing Repo Facility. This instrument functions as a possible reserve for banks in need of liquidity and it should ensure that the Overnight Lending Rates stay in line. A lack of liquidity can be disastrous for our financial system and must be prevented.

Size of the Federal Reserve's balance sheet (Source; Federal Reserve)

Criticism

Not everyone supports actively selling bonds. For example, Wim Boonstra in a debate with Paul Buitink on the channel of Holland Gold that selling actively is absolutely not wise; 'We are now in a situation where a large part of the national debt has been bought up by DNB. The Minister of Finance pays interest and repayment to DNB and gets it back in the form of dividends. Actually, you can cross it out.

If you put that back into the market, we will soon have to pay more tax to finance something that the government actually already owns.' Boonstra has already published about the monetary irrelevance of purchased government debt. It therefore makes no sense to put the purchased government debt back on the market. However, central banks must stop buying, according to Boonstra.

It will be very interesting to see how central banks operate in the coming months and how the markets will react to this. In America, it remains to be seen whether there is a risk of a repeat of the years 2018 and 2019. In Europe, it will have to be seen whether targeted purchases of debt securities are still accepted and how large the interest rate differentials will become in a market where the ECB is still intervening.

Admittedly, not with the large-scale purchases of recent years, but with the reinvestment of repaid loans in debt securities of the southern countries. We are already seeing a rise in interest rates, as the market rits against the ECB Speculates. Will the ECB get away with this, or will the market force the central bank to intervene again with targeted support measures? In that case, a turn to accommodative monetary policy cannot be ruled out.

![]() Have a look at us YouTube channel

Have a look at us YouTube channel

On behalf of Holland Gold, Paul Buitink and Joris Beemsterboer interview various economists and experts in the field of macroeconomics. The aim of the podcast is to provide the viewer with a better picture and guidance in an increasingly rapidly changing macroeconomic and monetary landscape. Click here to subscribe.