9.2

8.858 reviews

English

EN

Silver is heading toward its sixth consecutive year of deficits in 2026. In the World Silver Survey, research firm Metals Focus looks back on 2025 and ahead to 2026. The silver deficit could increase by 15% in 2026. What are the key trends, and what will this mean for you as a silver investor?

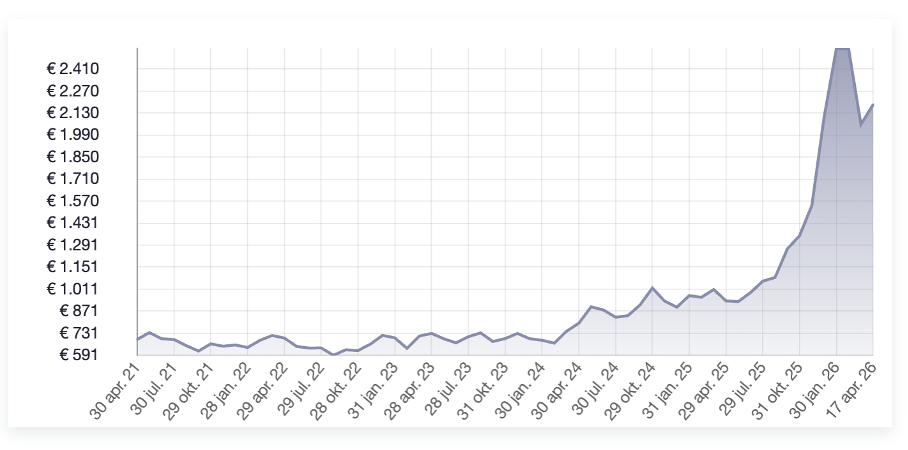

In 2025, we saw the silver price rise from €896 per kilo to €2,104 per kilo, an increase of 134%. A spectacular surge driven by a so-called silver squeeze starting in October 2025. This squeeze had been building for years, due to consecutive annual silver deficits. In 2025, everything came together: declining silver inventories, withdrawals from the London silver market, and massive demand from ETPs (Exchange Traded Products), also known as paper silver or trading in silver-backed instruments such as ETFs and ETCs.

After years of relatively modest gains, silver prices surged sharply at the end of 2025

After years of relatively modest gains, silver prices surged sharply at the end of 2025

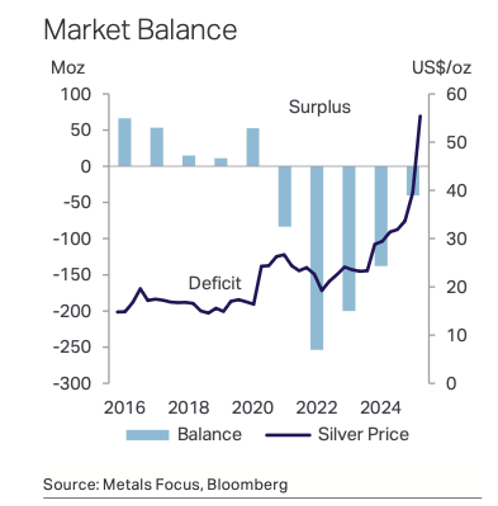

Silver deficits are expected to increase by 15% in 2026 due to declining supply. The net deficit is projected to rise from 40.3 million troy ounces to 46.3 million, according to Metals Focus. This reflects the actual shortfall based on demand from industry and the jewelry sector on one hand, and supply from mining and recycling on the other.

The bar chart shows annual silver deficits, while the dark blue line represents the silver price in dollars, source: World Silver Survey

The bar chart shows annual silver deficits, while the dark blue line represents the silver price in dollars, source: World Silver Survey

These deficits do not immediately translate into higher prices, until they suddenly become acute and a liquidity squeeze causes prices to spike. This is what we saw in October 2025 and the months that followed, when silver surged to unprecedented highs in January 2026. This squeeze is also reflected in the massive demand from (institutional) investors for silver through Exchange Traded Products such as ETFs and ETCs.

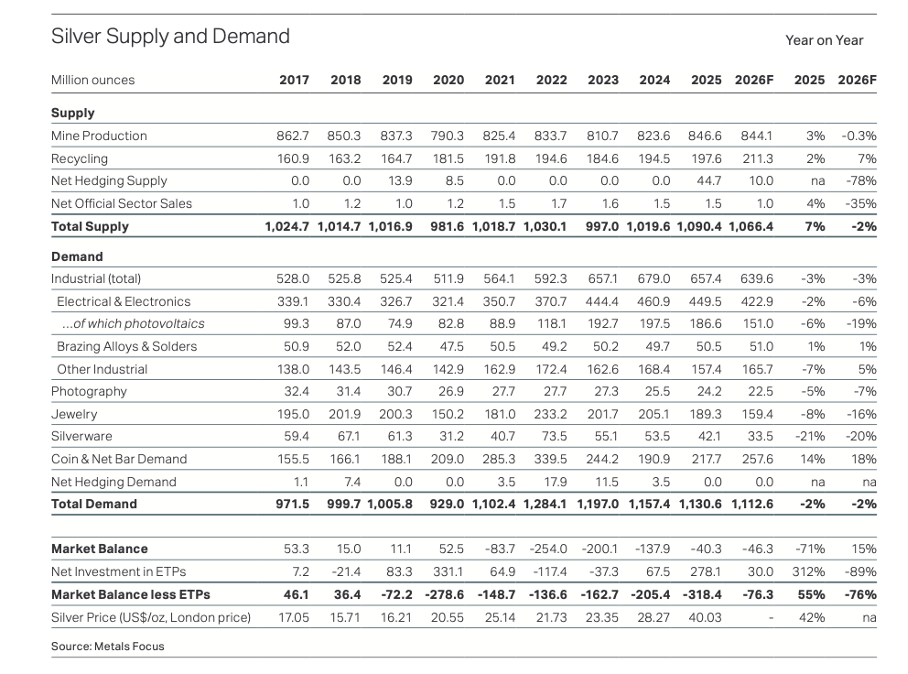

Including these paper positions, ETPs accounted for an additional 278 million ounces of silver demand in 2025, bringing the total deficit to 318 million ounces. The table below breaks this down by segment of the silver market, clearly highlighting the key trends.

Overview of total silver supply, demand, and investment demand via financial products, source: Metals Focus

Overview of total silver supply, demand, and investment demand via financial products, source: Metals Focus

Higher silver prices are also impacting industrial demand. Total demand from industry and jewelry fell by 2% in 2025. Silver jewelry and tableware have become less attractive to consumers due to elevated prices. Within industry, “photovoltaics” refers to silver demand for solar panels. Silver is a key component in solar technology, and the rapid expansion of solar farms has driven industrial demand. However, high prices are prompting manufacturers to seek substitutes or reduce silver usage.

According to the report, demand from emerging industries is increasing, particularly from electric vehicles and the growing need for electronics driven by data centers. As one of the best conductive metals, silver remains essential in these applications.

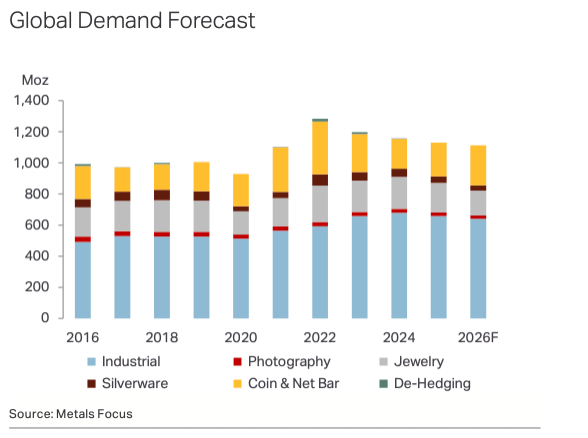

Global demand for silver bars and coins (in yellow) is increasing, source: Metals Focus

Global demand for silver bars and coins (in yellow) is increasing, source: Metals Focus

The decline in industrial demand is being offset by a sharp increase in investment demand. In 2025, more investors purchased silver bars and coins. Globally, investors are increasingly turning to physical silver, with demand rising by 14% in 2025. A further increase of 18% is expected in 2026.

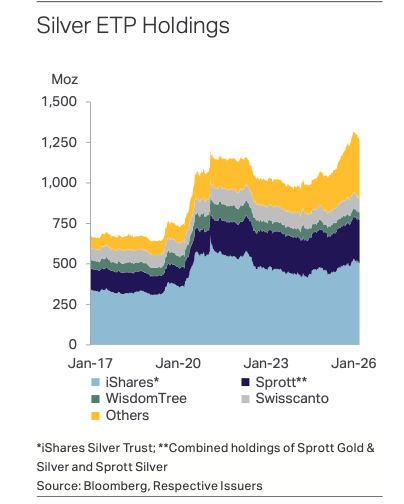

Total millions of ounces invested in ETPs, source: Metals Focus

Total millions of ounces invested in ETPs, source: Metals Focus

As reflected in the large volumes mentioned earlier, positions in paper silver are also rising. Notably, Asian funds are absorbing outflows from Western funds, while rapid price movements are attracting a growing number of short-term speculators.

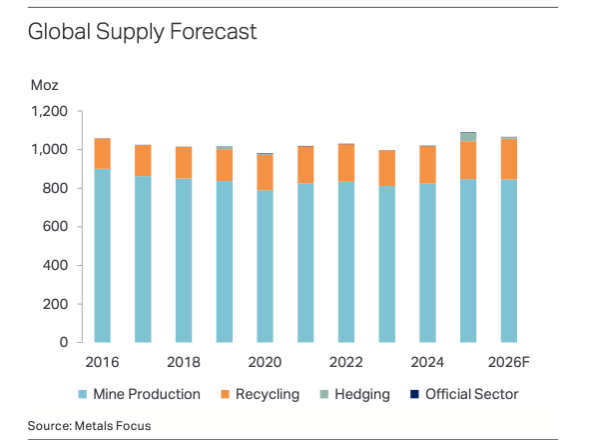

Despite strong demand, silver supply is not increasing significantly. One reason is that scaling up mining operations is a lengthy process. Although mine production rose by 3% in 2025, Metals Focus expects total supply to decline by 2% in 2026. Notably, despite silver prices more than doubling with a 134% increase, total supply grew by only 7% in 2025. Much of this additional supply came from hedging activities by market participants (refiners, miners, and industry). As shown in the table, this appears to be a one-off effect. With relatively stable supply levels, silver deficits are likely to continue widening in 2026.

Silver supply has remained largely unchanged for years, source: Metals Focus

Silver supply has remained largely unchanged for years, source: Metals Focus

Iran has announced that the Strait of Hormuz has been fully reopened to commercial shipping. “In line with the ceasefire in Lebanon, the Strait of Hormuz is fully open to commercial shipping for the duration of the ceasefire,” wrote Iran’s Foreign Minister, Abbas Araghchi, on X. Gold jumped nearly 2% to €4,123 per troy ounce in the first minutes following the news before easing slightly. By Friday at 15:56, gold was still up 1.4%. Oil prices (Brent crude) fell by 11%.

Gold price reacts to news of the reopening of the Strait of Hormuz

Gold price reacts to news of the reopening of the Strait of Hormuz

Gold, the Fed, inflation and labor data remain key drivers

Gold traded sideways in recent days as markets closely monitored peace negotiations between Iran and the United States. Comments from U.S. President Trump supported market sentiment. In recent days, U.S. equity markets recovered after Trump indicated that Iran may be willing to make concessions regarding its nuclear program and the Strait of Hormuz.

At the same time, Bloomberg reports that senior officials from Europe and the Gulf expect that reaching a comprehensive peace agreement could take up to six months. They warn that if the Strait of Hormuz does not reopen within the next month, it could trigger a global food crisis. This is because the Gulf region is a major producer of fertilizers, a sector highly dependent on energy. A shortage of fertilizers could result in lower agricultural output this year.

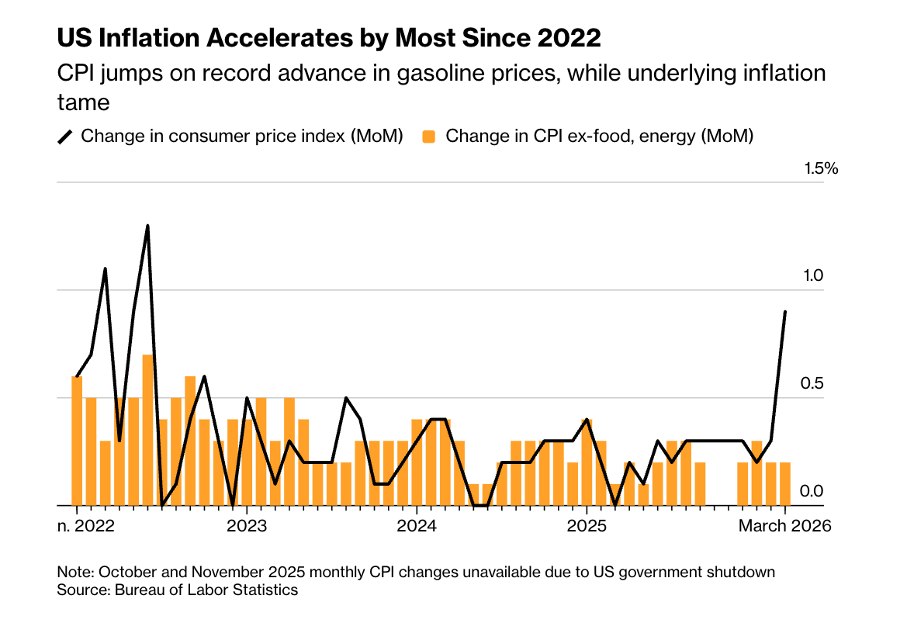

U.S. inflation shows the fastest increase since the 2022 energy crisis, source: Bloomberg

U.S. inflation shows the fastest increase since the 2022 energy crisis, source: Bloomberg

Gold is benefiting from market optimism driven by Trump’s statements. Earlier on Friday, the metal was up 1% compared to the start of the week in dollar terms. However, due to the strength of the dollar, this increase is less visible in euro-denominated prices.

The short-term outlook for gold is largely determined by expected central bank policy. The Federal Reserve’s recent Beige Book presented a complex picture:

Despite rapidly rising inflation, markets appear to expect that interest rates will remain unchanged, with more clarity expected at the Fed’s next meeting on April 28–29.

This suggests that the market is “moving in a more constructive direction,” according to Ole Hansen, Head of Commodity Strategy at Saxo Bank: “Lower real rates, a weaker dollar, renewed expectations of rate cuts, and a mildly speculative positioning all point to a market that is recovering rather than collapsing.” Hansen also notes that the gold market appears to have stabilized, as hedge funds have significantly reduced their positions. This lowers the risk of downward pressure from large-scale selling and increases the likelihood of renewed inflows into gold.