9.3

8.889 reviews

English

EN

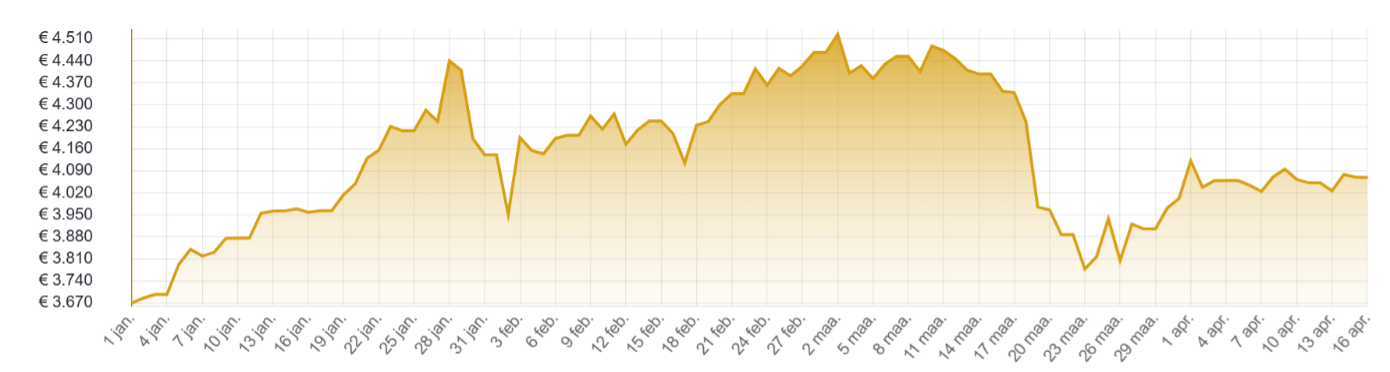

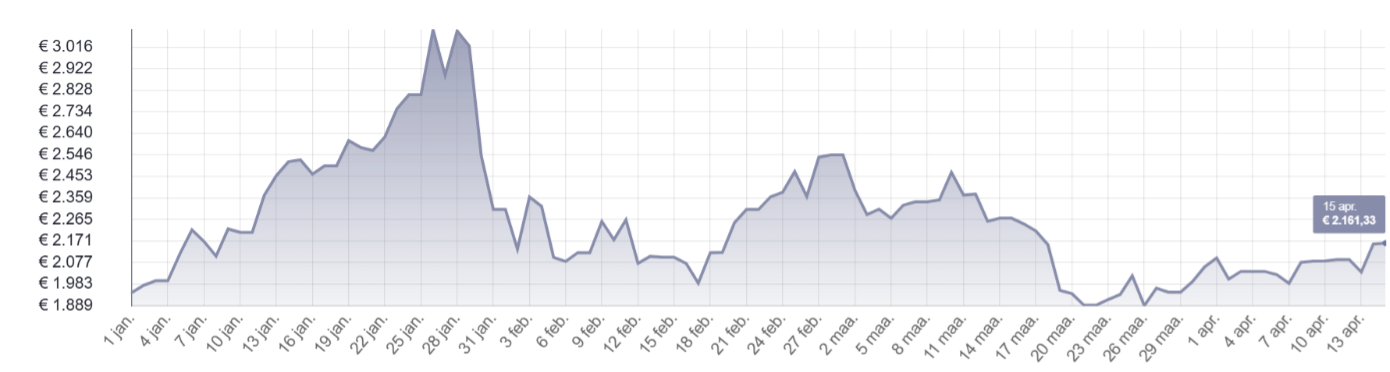

At the start of the second quarter, precious metals are trading within a relatively narrow price range. Gold and silver are currently up 11% compared to the beginning of 2026. In euros, this is about half a percent lower. In the case of gold, roughly half of the decline between the late-January peak and the March 13 low has now been recovered. Silver fell more sharply and has so far recovered only one-third of its price decline.

Unrest in the Middle East continues, but the rise of the dollar as well as the increase in long-term interest rates has now come to a halt. These were two key factors often cited by analysts to explain the decline in precious metal prices.

Chart: gold price since 1/1/26, in EUR per troy ounce (Source: HollandGold)

On the Comex futures market, the net long position in gold futures is at its lowest level since March 2024. At that time, however, the gold price was still trading at just $2,000 per troy ounce. This may indicate that profit-taking by speculators is largely behind us. In the absence of a clear short-term direction, momentum traders have also stepped out of the market for gold.

In physical gold ETFs, inflows are picking up again. During the March correction, there was an outflow of 94 tonnes, bringing total holdings to 3,044 tonnes. While this may seem significant, it represents only 17% of the inflows seen in 2025 (545 tonnes). Moreover, 21 tonnes were already repurchased in the first trading week of April.

These trends are particularly visible in China, as highlighted in the China Gold Market Update published earlier this week by the World Gold Council (WGC). Even in March, gold ETFs saw inflows of 7 tonnes, bringing the total for the first quarter to 50 tonnes, equivalent to $8.5 billion. All Chinese gold ETFs now hold a combined 298 tonnes under management.

At the same time, average trading volume on the Shanghai Futures Exchange in March was 12% lower than in February. This suggests a preference for physical gold over futures contracts. The Chinese central bank also expanded its gold reserves for the 17th consecutive month in March. By the end of March, China held 2,313 tonnes of gold. The total value of these reserves now accounts for 9% of the country’s total foreign exchange reserves.

Chart: gold price (Source: Stockcharts.com)

Chart: gold price (Source: Stockcharts.com)

Technically, short-term moving averages are starting to turn upward. The 200-day moving average, which acted as support when the decline halted in mid-March, has now risen to $4,176.

Concerns about rising inflation due to energy prices remaining higher than before the conflict persist. All central banks have a mandate to maintain price stability, and in the case of the Federal Reserve, this is complemented by the goal of maximum employment.

The U.S. labor market is performing better than expected, with stronger job creation and a lower unemployment rate in March. Combined with inflation concerns, this makes further interest rate cuts in the short term unlikely. This applies to the upcoming Federal Reserve meeting on April 29, and according to the CME FedWatch Tool, policy rates may not be cut at all this year.

Chart: silver price since 1/1/26, in EUR per kilogram (Source: HollandGold)

Chart: silver price since 1/1/26, in EUR per kilogram (Source: HollandGold)

Additionally, concerns about the political independence of the Federal Reserve have resurfaced after President Trump again threatened to dismiss Jerome Powell, the current Fed Chair. Powell’s term as chair is set to expire next month, although he can remain on the Board of Governors until 2028.

Powell may also remain as acting chair until the Senate approves the nomination of his successor, Kevin Warsh, who was put forward by Trump. That approval is being delayed due to a criminal investigation into Powell related to the renovation of the Fed’s headquarters. The investigation is being contested by both Powell and several members of the Senate.

Meanwhile, the IMF warns that U.S. government debt will continue to rise in the coming years. The budget deficit has already been around 6% of GDP for several years, and according to projections by the Congressional Budget Office, this trend will continue due to higher spending on healthcare and defense. The IMF notes that this could lead to rising bond yields, increasing the burden of debt. This is favorable for gold, which becomes more valuable in purchasing power terms.

The French central bank recorded a windfall gain of €12.8 billion by selling part of its gold reserves in the United States and repurchasing them in Europe. In recent years, several European central banks have attempted to repatriate gold reserves stored in the U.S.

This process has not always been straightforward. As a result, the Banque de France decided not to repatriate 129 tonnes of gold (5% of its total reserves) held at the Federal Reserve Bank of New York, but instead to sell it. The operation took place between July last year and the end of January this year. With 2,437 tonnes, France holds the fourth-largest gold reserves in the world. These are now fully stored in the vaults of the Banque de France in La Souterraine.