9.3

8.837 reviews

English

EN

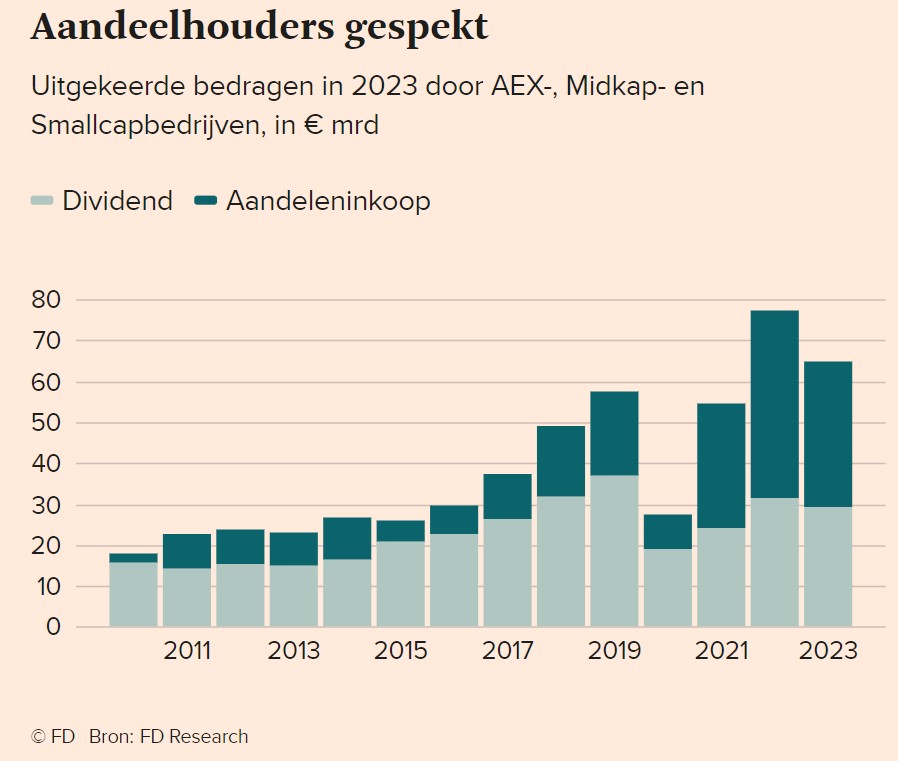

Listed companies are increasingly buying back their own shares to allow investors to enjoy the profits, according to research by the Financieel Dagblad. Before the coronavirus crisis, companies spent about 30 percent of their spending on rewarding investors through share buybacks. Now, that percentage has risen to more than half. The House of Representatives wants to tax this procurement, but that decision was met with a lot of criticism. Why are companies buying back shares and why is there a debate about it?

It seems strange; companies that buy back shares, even though they have spent them themselves to raise capital. Still, the buyback is a logical way for companies to reward the investor. Because an extra buyer is created in the market and therefore the demand increases, the share price is pushed up. The profit of the coming years will also be distributed over fewer shares, and the profit per share will therefore increase. From a tax point of view, share buybacks are also more attractive. When purchasing treasury shares, a tax of 30 percent is applied to the buyback bonus, which is the difference between the paid-up capital and the buyback price. This tax corresponds to the tax levied on dividends, but the paid-up capital is exempt from tax, which makes it possible to buy back own shares More advantageous from a tax point of view is.

Before 2012, for example, companies were allowed to own a maximum of 20 percent of their own shares, but those rules have been loosened and companies have become freer since 2012. For companies, the buyback is therefore a way to Dilution counteract. In many companies, it is common for additional shares to be issued from time to time. This is the case, for example, if additional funding is needed. The existing shares are diluted through an additional issue and share buybacks reduce that effect. Also, share buybacks are a more flexible way for companies to reward investors. If a company chooses to increase the dividend, it is actually forced to maintain this high dividend. The share buyback can be one-off and does not tie the company to a long-term obligation.

Share buybacks have risen sharply in recent years. (Source: Financieel Dagblad)

Share buybacks have risen sharply in recent years. (Source: Financieel Dagblad)

In The Hague, a discussion is raging about the buyback of own shares. The House of Representatives recently decided to tax the purchase of own shares at 17.65 percent. GroenLinks MP Tom van der Lee wants to use the tax to encourage companies to invest. "These gifts to investors widen the wealth gap, line the wallets of Boards of Directors and do not lead to real investments. That's why we want to tax the buyback, just like dividends!', as can be read in his tweet.

The decision was opposed by several employers' and investment organisations. According to these organizations, the tax makes the Netherlands less attractive and it could be a reason for Dutch companies to move to other countries where this tax is not levied. Also Jeroen Blokland, formerly an investor at Robeco and recently started his own investment fund, has focused on Forcefully pronounced as an opponent of the decision. Blokland does not understand why the government should receive income if a company decides to buy back its own shares. Companies are then forced to make less favourable investments and then the government decides how companies allocate them.

Also, according to Blokland, this tax does not work in favor of employees or investments. Wages will not be increased if this is not accompanied by higher company income. And a buyback offers companies that can't find attractive investments a way out. It gives investors the opportunity to invest the money they receive from the purchase in, for example, startups. Those who oppose share buybacks and would like to see more investments should focus on stimulating such investments, according to Blokland.

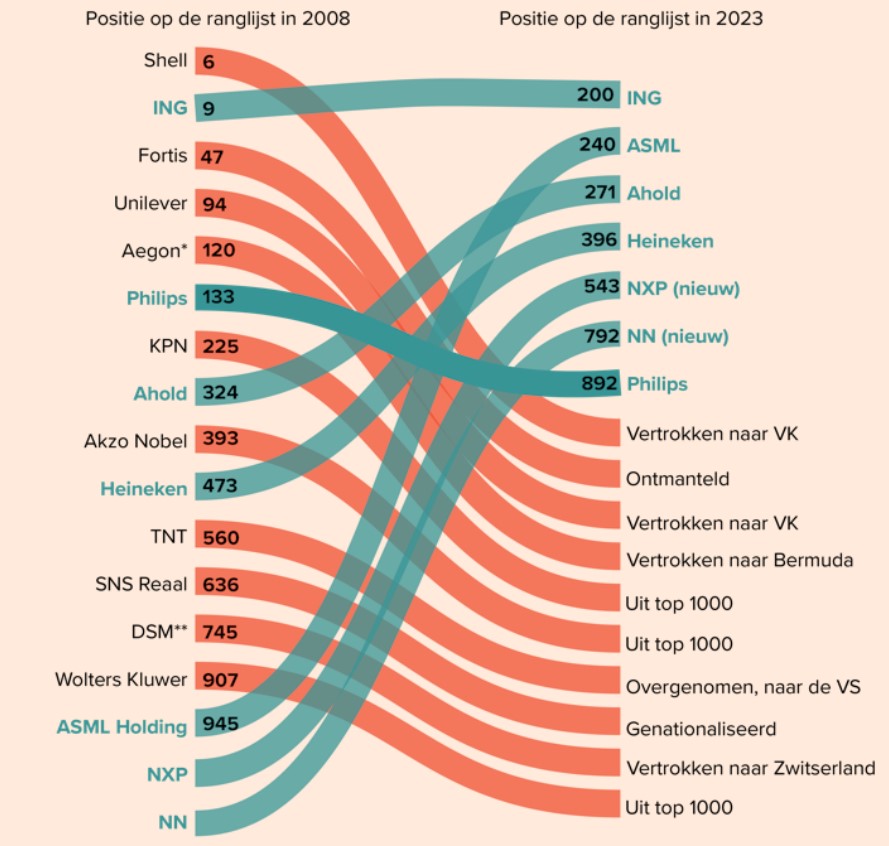

The discussion about the tax on share buybacks fits in well with the situation in which the Netherlands finds itself. Compared to 2008, there are fewer Dutch companies in the top 1000, according to Mathijs Bouman back in his column. At the time, ING and Shell were even in the top 10, but ING's profit, balance sheet total and workforce have fallen sharply since the credit crisis. As in 2008, Shell is in The Top 10, but, like Unilever, TNT, DSM and Aegon, is no longer a Dutch company. Akzo Nobel, KPN and Wolters Kluwer dropped out of the top 1000. A bright spot were newcomers Nationale Nederlanden, NXP and ASML, but recently crown jewel also expressed ASML's doubts about future investments in the Netherlands, as it is becoming increasingly difficult to find staff. The current political trend, which tends towards fewer foreign students and wants to phase out the expat scheme, also plays a role.

The change compared to 2008. (Source: Financieel Dagblad)

The change compared to 2008. (Source: Financieel Dagblad)

Since then, the debate about the business climate has come to a head. The government is now Pulling out all the stops to keep ASML in the Netherlands. The 'Belgification', as Bouman calls it, would be complete if ASML were to leave the Netherlands. He refers to the fact that foreign companies set the tone with our southern neighbors, supplemented only by some promising home-grown technology companies. It will be interesting to see whether the course will now be changed and the Netherlands will improve its business climate. In the coming period, we will elaborate on this at Holland Gold with some experts.