9.3

8.889 reviews

English

EN

The 60/40 portfolio has formed the standard in wealth management for decades. The allocation is simple: 60% equities for growth, 40% bonds for stability and income. For years, this combination optimized the risk-return ratio. Yet in 2022, the strategy came under significant pressure when both equities and bonds declined simultaneously. Morgan Stanley is now responding with a revised approach: the 60/20/20 portfolio, in which 20% is allocated to gold. Is this the end of an era, or is the classic strategy finding new paths?

In 1952, Harry Markowitz introduced modern portfolio theory, which laid the foundation for the 60/40 allocation. The principle was clear: maximize returns while minimizing volatility, in other words, the degree of price fluctuations. By combining equities and bonds, assets that complement each other under different market conditions, portfolio risk could be reduced without sacrificing returns. When equities fell, bonds absorbed part of the blow by rising.

The 1980s and 1990s were exceptionally favorable for this strategy. Since 1980, interest rates declined structurally, which made bonds valuable. The principle is straightforward: if a bond pays 5% interest and newly issued bonds only offer 3% after rate cuts, demand increases for the older bond with the higher yield. The price of that older bond rises accordingly.

US interest rate (source: FRED)

US interest rate (source: FRED)

Equities also benefited. Low interest rates made credit cheap for companies and reduced the attractiveness of saving, causing more capital to flow into equities, resulting in high valuations and strong returns.

In addition, the period was characterized by low and stable inflation. Interest rates remained above inflation, allowing bonds to preserve purchasing power. There was also a negative correlation between equities and bonds: during crises, central banks lowered interest rates to stimulate the economy, lifting bonds while equities fell sharply. This dynamic made 60/40 a reliable risk hedge.

Recent years show a different picture. High inflation and low interest rates are putting the strategy under pressure. In the European Union, only 6 of the 27 countries have balanced budgets. Deficits are financed by issuing bonds, but to keep borrowing costs manageable, the ECB maintains low interest rates and purchases government bonds through Quantitative Easing. This creates new money and fuels inflation.

US real interest rate (source: Investing.com)

The result is often a negative real interest rate. Inflation exceeds bond yields, putting purchasing power under pressure. When real interest rates turn negative, bonds lose purchasing power and become less attractive.

Moreover, the negative correlation between equities and bonds has weakened. In 2022, both declined simultaneously. The S&P 500 fell 19%, while medium-term bonds lost 10% and long-term bonds even collapsed by 39%. In periods of high inflation, investors move away from bonds into other assets, making the classic risk hedge less effective.

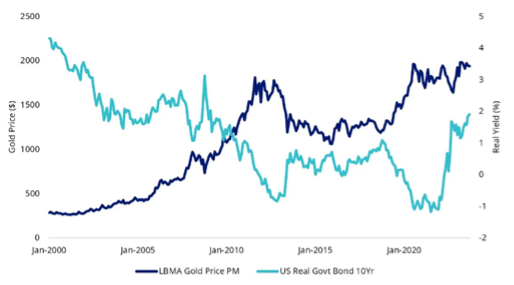

Morgan Stanley CIO Mike Wilson argues for a shift: 60% equities, 20% bonds, 20% gold. His argument is that gold offers better protection against inflation than traditional bonds. Historically, gold has often performed strongly when real interest rates are low and inflation is high.

Gold price and real interest rate (source: VanEck)

In addition, gold functions as a safe haven during crises. During the credit crisis, the dot-com crash, and the covid crash, gold rose while equities declined. In times of uncertainty, investors seek confidence and security. Thanks to this negative correlation with equities and low real interest rates, gold can diversify a portfolio and reduce overall risk.

The potential impact could be substantial. Given the size of global assets under management, even a modest allocation shift of a few percentage points toward gold could generate hundreds of billions of dollars in demand. In the relatively small gold market, this could create significant upward price pressure.

The 60/40 strategy flourished in a world of declining interest rates and positive real bond yields. Structural high inflation and negative real interest rates are undermining the traditional role of bonds as a risk hedge. Gold offers an alternative: it protects against currency debasement and retains its safe-haven function when markets come under pressure.

Also take a look at our YouTube channel

On behalf of Holland Gold, Paul Buitink and Yael Potjer interview economists and macroeconomic experts. The goal of the podcast is to provide viewers with greater insight and guidance in an increasingly fast-changing macroeconomic and monetary landscape. Click here to subscribe.