9.2

8.875 reviews

English

EN

In 2022, Pieter Omtzigt drew attention to the ever-problematic euro. In 2023, a roundtable discussion with experts followed in the House of Representatives. But the political impasse since then has pushed reflection on the euro into the background. While not all questions have been asked, let alone answered. Under pressure from Italy and France, there will be renewed calls for a more far-reaching Euro-fiscal union at the end of this year. Where do we go from here? On the initiative of the House of Representatives, a 'State Commission on the Euro' should therefore now be set up, argues economist Harry Geels.

In May 2005, former investigative journalist and now nature farmer Marcel van Silfhout made the production that is still relevant today: Eurobedrog. Five years before the outbreak of the euro crisis (2010), this was the first major euro-critical review in the general Dutch media. At the time, it was about the scandal of the far too low euro entry rate of the guilder in 1999 and the consequences of this for the Dutch in particular, which affected purchasing power and prosperity. But also about the problem of the euro in general, which was still brewing under the surface at the time.

With the initiative of Pieter OmtzigtRoundtable discussion about the euro in the House of Representatives at the beginning of 2023 as a stepping stone, Van Silfhout now looks back on that Zembla documentary in a contemplative and revealing way almost 20 years later. But also, for the sake of historiography, on what preceded and surrounding the introduction of the euro in the Netherlands, and what happened afterwards. This (pre)publication about 'The Netherlands and the euro' is highly recommended for anyone who wants to delve into the past, current events and the future of the problem currency.

In conversations around me, I have been observing for years that the average citizen has little or no idea what kind of disastrous influence the euro has had – and still has – on purchasing power and prosperity in the Netherlands. And on the financial risks that the continuation of the euro entails for us Dutch. Possibly due to a lack of knowledge, but certainly also for political-ideological reasons, the political establishment practically never points this out and is not sufficiently thought about. In the mainstream media, it's the same story. It is only in a small circle that the problems of the euro are seen and understood, and in even smaller circles they are recognised.

In the run-up to the introduction of the euro, there were warnings that the euro would become a dangerous and destructive monetary project. In particular by professors Arjo Klamer and Alfred Kleinknecht, who were ridiculed and even cancelled as a result. But even in the meantime, the late André Szász, the greatest Dutch monetary expert ever to work at the Dutch Central Bank, saw this very clearly. But they were not listened to at the time. Despite this, Arjo Klamer themselves stir during the ongoing euro crisis. This is also the case for euro researcher André ten Dam, who, by the way, already at the beginning of 2010 Substantive contribution to the international economic and scientific debate on alternatives to the euro.

With today's knowledge, the Netherlands would naturally never introduced the euro, so did practically all of them Disconcerting euro roundtable discussion participating experts in the House of Representatives in early 2023. Ronald Plasterk, by the way, wasSame conclusion and then Calledfor a Dutch exit from the euro. The advantages of the euro have long been outstripped by its disadvantages, especially for the Netherlands.

Former Minister of Finance Hans Hoogervorst had announced a year earlier thatin EW Magazine a stone thrown into the euro pond: it really can't go on like this, we never intended it that way, and if it doesn't change soon, then the Netherlands should leave the euro. This is what Hoogervorst explained once again at the round table.

Hans Hoogervorst, former minister, on the European debt factory and option to leave the euro

And former DNB director Lex Hoogduin also made his contribution to the euro: instead of the strong German-Dutch euro we were promised, we have now ended up in a weak, Latin currency union with the euro. In addition, one way or another, the Netherlands and Germany are guarantors for the ever-increasing and unsustainable public debts of the weaker, southern euro countries.

And a North/South transfer union costs the Dutch citizen gold money. A rather expensive hobby of possibly even € 35 billion a year, he hadcalculated. During the roundtable discussion, Hoogduin said that it could easily be twice as much. So €70 billion a year. Hoogduin did not even mention the fact that the international exchange rate of the euro, which has been falling steadily since the beginning of the euro crisis, has saddled Dutch citizens and SMEs with a loss of purchasing power.

So much open and widely supported criticism of the euro had never been uttered before by such prominent figures. Nevertheless, in the Thorbecke hall of the House of Representatives, the only logical final conclusion was carefully avoided. After all, the euro – as another former Minister of Finance, Jeroen Dijsselbloem, made clear – is much more than a currency. The euro is above all 'political'.

Precisely because alternatives to the euro were hardly discussed in the Thorbecke Hall, the MPs did not know what to think next. Let alone what to do next. Neither did Pieter Omtzigt. Then 'muddle through' again?!

Incidentally, before the introduction of the euro (1998), the aforementioned André Szász had already foretold that, after the actual crash of the euro (i.e. in 2010), the 'muddling through' with the currency would take a very long time. But after more than 14 years of 'muddling through', that may have been enough.

The Canadian Nobel Prize winner, the late Robert Mundell, in the distant past, in his so-called Theory of Optimal Coin Areas Four criteria have been set out which would have to be met in order for monetary union (with exchange rates fixed in the single currency and the same interest rate for each country to be the same) between countries to be successful.

This requires good labour mobility, free movement of capital within the currency area and a high degree of political integration (with a fiscal union and mutual financial transfers and thus the need for mutual solidarity). Above all, however, the countries participating in a currency union must be economically convergent, i.e. have equal economic strength and business cycles.

But with the Euro experiment, Mundell's theory can be clarified, even rewritten. With the euro, for example, it has become clear that if the condition of 'economic convergence' is not met in a currency union, such a currency union will not only be destructive for the participating countries, but that in that case the other three conditions for a currency union (political union, labour mobility and free movement of capital) will also be counterproductive. If the economies of the countries participating in a currency union differ too much in terms of their character, economic cycles and, above all, their strength and development, the economically weaker countries will eventually pull the initially economically stronger countries into the abyss with them.

In his account of the Eurobedrog (Eurobedrog) account, Van Silfhout points out that, precisely in view of the economic differences between the European countries, there is also a European context, (OPTICS Report, 1976) and by England, (Hard ECU plan, 1989), that is to say, well before the Maastricht Treaty (1992), there was an explicit warning against a European Community currency Instead of but precisely Next to national currencies.

Moreover, as Arjo Klamer also argues, in addition to the economic aspects of a currency union, there is also the Cultural aspect. In order to be able to show solidarity, there must also be a cultural connection between the peoples of the countries participating in a currency union. But because of the centuries-old deep-rooted cultural diversity between the various European countries, there is none. There is no European 'demos'. There is no such thing as a European citizen.

It is therefore very important for each (euro) country to have a currency with a balanced exchange rate in relation to other countries with which a common trading market is formed and an interest rate appropriate to each individual country. With the right exchange rate and the right level of interest rates, economic equilibrium is created. On the one hand, between the domestic and foreign-related economy of a country, and on the other hand, between the countries that trade with each other.

This mechanism was developed by Euro-analytical engineer Theo Wolters 'Monetary welfare optimisation' said. In this way, prosperity in every country is optimally served.

However, due to the impossibility of adjusting exchange rates and interest rate differentiation between the economically different euro countries, this can never be the case for all euro countries at the same time within the current one-size-fits-all euro pact.

To say that the introduction and maintenance of the euro has had and continues to have major consequences for the Netherlands is an understatement. For the Dutch, the Euro project went wrong right from the start. The so-called Exchange loss As a result of the far too low euro entry rate of the guilder in 1999, we subsequently structurally lost 12% of purchasing power. The guilder should have been revalued in 1998, but unfortunately this did not happen for political reasons.

André ten Dam about the loss of billions of euros when the guilder was exchanged and his solution for preserving the euro

And since the outbreak of the euro crisis, the damage and risks for the Dutch taxpayer have become much greater. After all, by artificially maintaining the euro through all kinds of emergency funds, the (far too) loose ECB policy and the Eurobonds issued by the EU during corona (joint European debt securities in which the Netherlands is jointly and severally liable for the repayment to the financiers), the Dutch taxpayer is firmly 'at the bar', as also statedPieter Omtzigt in the subsequent parliamentary debate.

The fact that, according to Lex Hoogduin, maintaining the euro through a transfer union will cost the Netherlands an annual amount of between €35 and €70 billion, will not have eased Omtzigt's concerns. After the Eurobonds in the corona crisis in 2020 with a total amount of approximately €800 billion (eventually accepted by the government of Mark Rutte and the House of Representatives at the time under the motto 'once but never again'), there is now Italian opinions by Enrico Letta and Mario Draghi urged the EU to have structural Eurobonds, which the Netherlands so despises, and thus for a more far-reaching European fiscal and transfer union.

It is important to understand that a political union within the Europact will only ensure that financial transfers from the stronger to the weaker countries will take place more easily and without hindrance (i.e. more quietly). And that when the shore finally turns the ship around, it is much more difficult to correct things.

The introduction of the euro has therefore been rather disastrous for the Netherlands as a result of the far too low euro entry rate of the guilder (the food banks did not spring up from 1999 without reason), so the continued continuation of the euro also appears to be a rather expensive, let's say unaffordable political hobby. But unfortunately, it doesn't stop there for the Dutch. After all, we are now in a Exchange Loss Case 2.0.

In order to save the euro in the euro crisis and to keep the currency union together, the European Central Bank has pursued a policy since 2010 that has caused the international exchange rate of the euro to plummet from about $1.60 in 2010 to about $1.05 in the last few years. As a result, the Southern, weaker euro countries became competitive again on the international trade markets, but at the same time the Netherlands became far too cheap as a result. The result: a loss of purchasing power and therefore prosperity for Dutch consumers and SMEs, and at the same time an exorbitant trade surplus.

Not now with the guilder, but with this greatly undervalued exchange rate of the euro, our economy has once again overheated, just like in the second half of the 1990s. And just as in the years of the Exchange Loss Case (1999 to 2006), as a result, purchasing power-damaging inflation is now being imported from abroad again, as economists call it, resulting in a further wage/price spiral, thus in an even more festering inflation.

After the first major poverty trap in the Netherlands as a result of the non-revaluation of the guilder when the euro was introduced, we have now ended up in a second poverty trap. And now as a result of not being able to revalue our national currency. Unfortunately, the vulnerable groups in the Netherlands are much larger now than they were 20-25 years ago.

In fact, the euro is de facto only a crown jewel of and, above all, a crowbar for the politically and ideologically desired European integration that should culminate in the United States of Europe. That is why Eurocriticism is not tolerated by the political establishment, concealed where possible and, where necessary, ridiculed or suppressed.

In 2021 I Shown that in the case of the European Central Bank and the national central banks, too, euro policy takes precedence over sound monetary policy and Treaty rules, with all the consequences that entails. Moreover, we can now also ask ourselves whether, because of this (ostrich) policy, the monetary-economic mechanisms are still properly understood by political and monetary policymakers? And are the Dutch and European political leaders aware of the seriousness of the euro problem and the urgency to finally address it properly?

The Dutch government has, however, Emergency scenario developed in the early years of the euro crisis, in case the euro were to fall. It is an open secret among insiders that in that case the new Dutch guilder, the Florijn, will be (re)introduced. Then, no doubt, in consultation with Germany, which will then reintroduce the Deutsche mark.

At the end of 2022, a limited number of MPs were allowed to view that emergency scenario, under strict secrecy. According to the saying Sigrid Kaag, the then Minister of Finance, was never allowed to talk about this publicly because it would be speculative, but also because it affects foreign relations and could affect the capital market. A rather nonsensical reasoning because that emergency scenario has been out in the open for a long time. So we don't have to be secretive about that. After all, when switching to another currency, it is not so much the switching that is 'sensitive', but much more the general knowledge of the time of such a switch.

Harry Geels on 12 future scenarios of the euro

What is worrisome is that the emergency scenario in the drawer is apparently not only too limited, but also insufficiently elaborated. For example, we can deduce from the then on March 9, 2023 by then Member of Parliament Derk Jan Eppink Motion tabled. But what is particularly worrisome is that we also know that the emergency scenario will be taken out of the stable first when the euro implodes and has lost its value much further. In other words, the Netherlands will remain in the euro and (instead of a good preparation in the future) we will see where the ship strands, while every day that the Dutch participation in the euro continues costs us money on average. And while there have been plenty of suitable alternatives available for years!

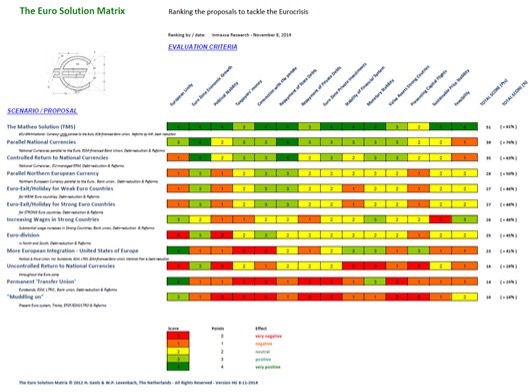

In 2012, when the various alternative scenarios for the euro had crystallised in the international economic-scientific debate, I (with the help of a number of experts in the field) compared them in a matrix according to relevant economic, monetary, financial, social and political criteria and ranked them in the so-called Euro Solution Matrix.

In addition, The Matheo Solution (TMS) by the aforementioned Dutch euro researcher André ten Dam (by far) with the best score because TMS combines the advantages of the monetary systems of both national currencies (possibility of exchange rate adjustments and interest rate differentiation) and the euro (monetary stability and absence of currency speculation), while at the same time eliminating the disadvantages of both systems, and also because TMS can be introduced quickly (without Treaty change) and easily (the euro remains the only means of payment in every euro country).

And the muddle-through/transfer union scenario that has been followed by politicians since 2010 has (by far) the worst score in the matrix.

In the round table discussion on the euro initiated by Pieter Omtzigt, therefore, by no means all the questions were asked. Where do we go from here? Will the euro ever be okay again? Wouldn't it be better for the Netherlands to leave the euro? And are there no other monetary avenues to be taken? And these questions do indeed need to be thoroughly investigated and answered. While the Netherlands and Germany did not even participate in this at the time, the previous Latin monetary union (1866-1927) was also Not eternal life To be able to do so, it is not the first time

In view of the unsolvable problem of the one-size-fits-all/none euro and the great importance of a well-suited monetary structure for the prosperity of the Netherlands, a 'State Commission on the euro' should therefore be set up on the initiative of the House of Representatives. The committee should not only compare the various monetary scenarios, but also calculate their 'ins and outs' using the computing power of the CPB and Statistics Netherlands. Such a committee would then have to be balanced in terms of staffing , in the sense that there would also be ample room for experts who have been making well-founded criticisms of the euro for years and the perpetual continuation of it.

The committee's final report will then provide insight into the euro and the various alternative scenarios and thus provide input for the Netherlands to reach the right conclusions about this. And that final report can then be used by the Dutch government to conduct a balanced discussion about the future of the euro within the Eurogroup and the European Union. This will then lead to decision-making in a European and/or Dutch context.

Harry Geels (1969) is an economist, publicist, lecturer, researcher and asset manager, currently working as deputy editor at Financial Investigator, lecturer in Investment Management at the Actuarial Institute and Senior Investment Advisor at Auréus Vermogensbeheer. Geels has been fascinated by the euro since its introduction. In his financial-economic articles and columns (currently for Financial Investigator and before that for Investors Interests and for many years for De Financiële Telegraaf) he regularly writes about the European currency and the emergency steps to maintain it.

This article was previously published (June 2024) in a similar version on OpinieZ.com