9.3

8.837 reviews

English

EN

Last month, Rabobank published a a report in which it stated that Europe needs to pursue new policies. The bank's economists see a number of major vulnerabilities for European countries. What vulnerabilities is the bank talking about and how can Europe deal with these Achilles heels?

Europe is very vulnerable when it comes to important scarce raw materials, because European countries are largely dependent on a small number of countries for many raw materials. This was already visible when the war in Ukraine broke out and European countries had to deal with high energy price increases. Europe is now focusing on the transition to green energy sources, but this also requires scarce raw materials. Europe is very dependent on non-European countries for the purchase of these raw materials. For this reason, the European Parliament adopted the Critical Raw Materials Act an initiative to reduce dependency on other countries. However, the funding of the initiative is still shrouded in mystery.

If Europe chooses to produce more itself, this could lead to higher inflation rates. In addition, the energy transition already involves major investments, as houses have to be insulated and because many industrial and logistics processes are being overhauled. Precise estimates of the costs of the energy transition vary, but it seems certain that substantial investments will be needed in the coming years, which will probably lead to structurally higher inflation.

Last week, Jack Highland doubts about the feasibility of the energy transition. According to Hoogland, the upscaling of the production of copper and uranium, for example, will take up to ten years. As a result, the prices of these raw materials will rise sharply in the coming years. This applies, for example, to copper; 'The production of electric cars requires much more copper than the production of petrol cars, but the supply of uranium will probably not be able to keep up with that demand,' Hoogland said.

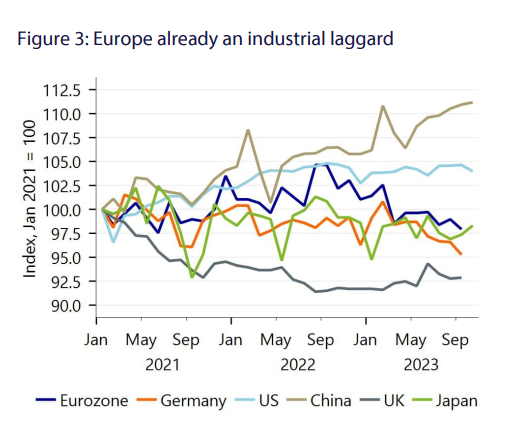

Jack Hoogland was also critical of Europe's industry, as there is less and less production on the continent, and Hoogland is therefore supported by the economists of the Rabobank. In Rabobank's report, industrial production is the second Achilles heel. The production of important goods is essential for a country's strategic autonomy. But production in Europe is declining and high energy prices are playing a major role in this.

Other superpowers, such as the U.S. and China, can live on low energy prices for a long time, but things are different in Europe. As a result, companies are more likely to choose to move production out of Europe, rather than to establish themselves on our continent. This can also be seen in the production figures. Production in Germany decreased by five percent since 2022, but in America and China, production grew by five and eleven percent, respectively. For Economist Han de Jong this trend is worrying and was reason to call the developments in Germany a 'disaster'.

The industrial figures in several countries paint a bad picture for Europe. (Source; RaboResearch)

In recent years, it has become clear that war on the European continent can no longer be ruled out. European countries have a lot of soft power. Rules drawn up in Brussels are also quickly being implemented on other continents, the so-called Brussels effect. However, European countries have not invested enough in defence to be able to make much of a military contribution against other major power blocs even without the help of America. In view of a possible Trump victory in the upcoming presidential election, the future of NATO is uncertain.

Another factor is that the EU may be a strong economic and monetary union, but it does not always work out politically. EU countries seem too different to convey political unity. This can be seen in the differences between North and South in terms of fiscal rules, but also between East and West in relation to immigration, for example. The lack of political unity is a stumbling block to the formation of a military alliance.

A fourth vulnerability for Europeans concerns the issue of migration. Since the Arab Spring, the number of migrants has skyrocketed. This not only caused a heated discussion in our own country, but in many European countries there is a discussion about migration. In recent years, Rabobank has seen a shift to the right. For example, Germany is now pursuing a stricter migration policy, but the PVV's victory in the last elections did not come out of the blue for Rabobank either.

The costs for these four vulnerabilities run into billions. Rabobank estimates the cost of these four vulnerabilities to be between a minimum of two and a maximum of five percent of the national product. However, many European countries do not have the space to deal with these high costs. While governments may make some cuts, the implementation of the above plans is likely to be accompanied by higher debt-to-GDP ratios. The question is whether countries that already have a high national debt can bear this burden with rising interest rates, Rabobank writes.

Rabobank also argues that the theories that were previously dominant no longer offer a way out. A liberal policy, in which a tight monetary policy, austerity and a high level of confidence in the market are central, no longer offers a solution. Higher interest rates actually slow down growth further and liberal policies ensure that more imports are made from countries such as China. Although we will be 'green' in the short term and drive electric cars, this will further erode European industry. Liberal policy does not give us strategic autonomy, according to Rabobank.

Keynesian policies, with fiscal stimulus and protectionist policies, are an equally unattractive option, the report says. Stimulative fiscal policies could not only promote the energy transition and industrial production, but also help address social and economic challenges. At the same time, this policy leads to high inflation, with higher interest rates as a high price. And as we saw earlier, governments don't have the space to spend much more.

Rabobank, on the other hand, proposes a new 'holistic' approach, drawing up a clear strategy to help Europe get back on its feet. It is a policy mix that considers different policy areas to serve three major pillars; energy transition, industrial revitalization and a stronger army. Rabobank calls it a 'fiscal whatever-it-takes', referring to monetary policy under Draghi. In this case, the government intervenes to free up enough capital for the necessary investments, as the market is inadequate. Debts must remain sustainable and moderate inflation is permitted.

A call for a European long-term strategy also came from former chief economist of Rabobank, Wim Boonstra, in a podcast by Holland Gold; 'The difference between China and Europe is that China thinks a long time ahead. When China wanted to become an economic power bloc in 1979 and started opening up the economy, there was a chuckle in Europe and America. Twenty years later, it is thanks to China that the global poverty reduction goals have been met. Ten years later, China had become a world economic power. They know exactly where they want to go. While Europe has been asleep for ten years when it comes to strategic thinking, otherwise we really wouldn't have been so dependent on Russian gas or Arab oil,' says Boonstra.

Have a look at us YouTube channel

On behalf of Holland Gold, Paul Buitink and Joris Beemsterboer interview various economists and experts in the field of macroeconomics. The aim of the podcast is to provide the viewer with a better picture and guidance in an increasingly rapidly changing macroeconomic and monetary landscape. Click here to subscribe.