9.3

8.837 reviews

English

EN

The Fed, the U.S. central bank, cut interest rates by half a percentage point on Wednesday. In doing so, the central bank is following the same course as the European Central Bank (ECB), which has already cut interest rates twice by a quarter of a percentage point. Nevertheless, American companies may still have to deal with higher interest costs in the near future, while interest rates have been lowered. Why is that exactly?

With the Fed's rate cut, the interest rate has been reduced to a range of 4.75 to 5 percent. The rate cut was already predicted by the market, but how much the Fed would cut rates was still uncertain. One week earlier estimate market prices the probability of a quarter-percentage-point rate cut by the Fed was about 65 percent, while the probability of a half-percentage-point cut was at 35 percent. The day before the decision, these ratios were reversed, with a 65 percent chance of a half-percentage-point cut.

Last week, economist Han de Jong that there is room for the Fed to cut interest rates. In America, higher rents in particular play a role in inflation. If rents are not taken into account, inflation is only 0.7 percent. And since a sharp decline in rent increases is expected, inflation could fall rapidly in the coming months. Han de Jong believes there is a chance that the rent increase will halve and that inflation will be around 1.6 percent, well below the policy target of 2 percent.

In addition, the Fed wants to prevent the U.S. labor market from deteriorating. The ECB's sole mandate is to maintain price stability. The U.S. central bank has a dual mandate and must not only curb inflation, but also stimulate employment. With inflation coming down and the labor market deteriorating, there is room for the Fed to cut interest rates. Therefore, multiple rate cuts are certainly conceivable in the coming months.

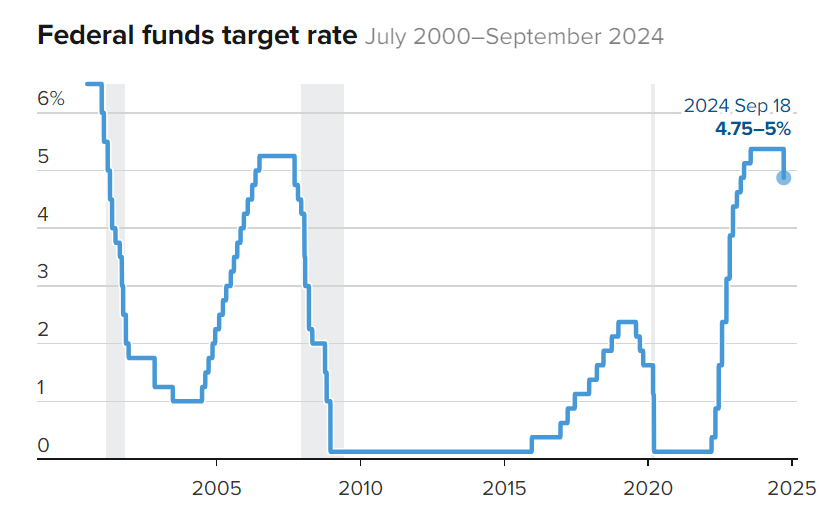

The Fed's interest rate has been cut again for the first time in a long time, as can be seen in the chart. (Source: CNBC)

The Fed's interest rate has been cut again for the first time in a long time, as can be seen in the chart. (Source: CNBC)

Nevertheless, the effect of the interest rate cut is not yet felt. In fact, companies are likely to face higher interest charges, he wrote The Economist last week. Why is that?

The central bank's policy always works with a significant lag. This is because, after an interest rate cut, companies first need time to analyse which investments are necessary and profitable. After that, companies take out a loan and investments are made. The money from these investments therefore only ends up with other companies after a few months, which then start spending that money again after some time. So before an interest rate cut really has an impact on economic growth, a lot of water still flows through the Rhine.

Due to the corona crisis, the slowdown in central bank policy may last even longer than previous periods, which means that companies will first have to deal with higher interest rates before interest rates in the market go down. During a previous interest rate hike in the period from 2016 to 2019, companies' net interest expenses rose by nine percent. Borrowing therefore became more expensive and investments subsequently decreased. But during the period after 2022, when interest rates rose much faster, net interest expenses fell by 35 percent. If the relationship between the policy rate and interest expenditure had held up, net interest expenditure would have had to rise by 50 percent.

One reason for this remarkable change is that companies were sitting on a big pile of money at the start of the rate hike. Companies' reserves were already rising in the years before the coronavirus pandemic. As the pandemic spread, businesses spent less money, as investments were postponed. For example, the cash reserves were more than doubled. Companies also received a higher interest rate on these reserves.

Another explanation may be that banks were less likely to pass on higher interest rates, because the risk of default was also lower due to increased reserves. The Economist points to the fact that banks' credit margins on safe loans have fallen in recent years. Normally, these margins increase during a tightening cycle, as borrowing becomes riskier as the policy rate rises. But between the beginning of 2022 and mid-2023, margins for these safe loans actually fell by more than 1.5 percentage points. The increased reserves reduce the risk for banks, resulting in lower market interest rates than expected.

In addition, many companies took out long-term loans with low interest rates in the period before interest rates went up. As a result, these companies were less affected when interest rates were raised. It is quite possible that this cheap financing has played a role in the strong growth that the S&P 500 has experienced in the recent period, while the central bank has raised interest rates. Now these cheap loans are starting to expire and the companies have to refinance their loans. Because these companies are looking for new financing, companies may first have to deal with higher interest rates.

An interest rate cut of this magnitude is fairly unique. In the early days of the corona pandemic, interest rates were lowered considerably. In addition, interest rates were significantly reduced in the crisis of 2007 and 2008, just as they were in the crisis after the bursting of the internet bubble and after the attacks on September 11. It shows that the Fed is seriously concerned about the cooling of the economy. At the moment, this cooling is mainly visible in the labour market. And if the effect of the central bank's policy is indeed delayed after the corona crisis, the Fed's concerns could be justified. In that case, it is possible that the Fed will cut interest rates even more often in the coming months. In Europe, too, there is a call to raise interest rates further reduce. In the coming months, it will become clear how the economies will develop and how central banks will respond.

Photo: Federal Reserve Bank of Chicago (source: Kenn Lund)

Have a look at us YouTube channel

On behalf of Holland Gold, Paul Buitink interviews various economists and experts in the macroeconomic field. The aim of the podcast is to provide the viewer with a better picture and guidance in an increasingly rapidly changing macroeconomic and monetary landscape. Click here to subscribe.