9.3

8.683 reviews

English

EN

For the first time in a decade, bonds are back to their hallmark: providing a fixed and predictable return. Now that interest rates have risen sharply in recent years, bonds are becoming popular with investors again. What is the return on these investments and what can we expect from interest rates in the near future?

After the credit crisis, interest rates on the capital market fell to unprecedented low levels. The ECB's expansionary policy led to downward pressure on both short-term and long-term interest rates. On the one hand, the policy rate fell sharply (short-term interest rates), and on the other hand, the central bank influenced long-term interest rates by buying bonds. For years, the Dutch State was able to issue bonds at negative interest rates, but other governments also enjoyed extremely low financing costs.

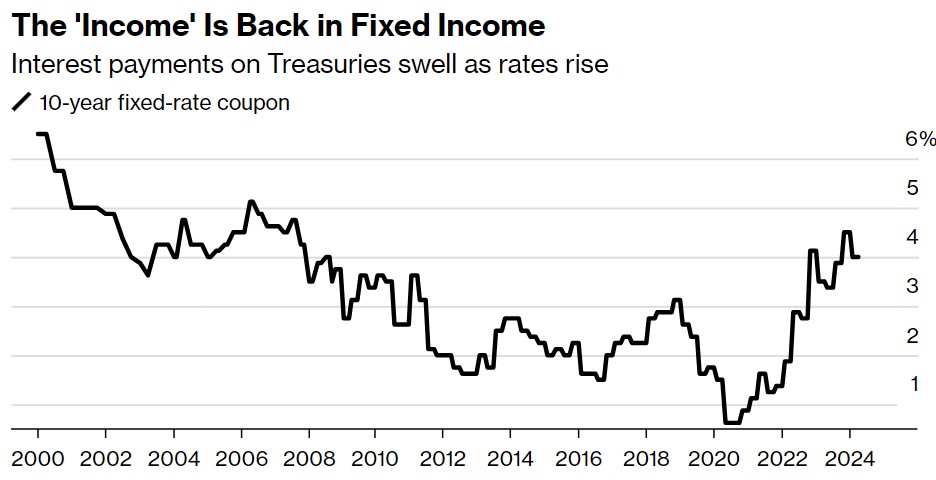

But with interest rates rising, investing in bonds is becoming more attractive and it shows in the market. U.S. Treasury yields rose from zero to five percent in two years. At the same time, the total amount of interest income received by investors increased to $900 billion, twice as much as the average during the previous decade. And as more and more bonds are issued at high interest rates, total interest income is likely to increase further. In doing so, bonds are once again fulfilling the traditional role of a source of income that investors can rely on and commit to for the future, regardless of the Yield.

Interest rates have risen rapidly in America. (Source: Bloomberg)

Interest rates have risen rapidly in America. (Source: Bloomberg)

It causes a sharp increase in interest costs for the US government. The national debt of the Americans currently stands at a staggering 34,700 billion dollars. Now that interest rates are rising, interest costs are also rising. In March alone, Americans paid $89 billion in interest to creditors. That's an expense of two million dollars every minute.

The central banks' asset purchase policy, Quantitative Easing (QE), also has downsides, as economist summed up Han de Jong together in his column. The purchase of government bonds has always been done through commercial banks. As a result, many bonds with low yields have ended up on the central bank's balance sheet. Central banks made profits for years and paid those profits as dividends to the state. At the same time, the reserves of commercial banks increased enormously. As a result, the banks were able to provide loans at low interest rates. In this way, the purchase policy stimulated economic growth.

The bank reserves of commercial banks increased mainly during the pandemic. (Source: Crystalcleareconomics)

The bank reserves of commercial banks increased mainly during the pandemic. (Source: Crystalcleareconomics)

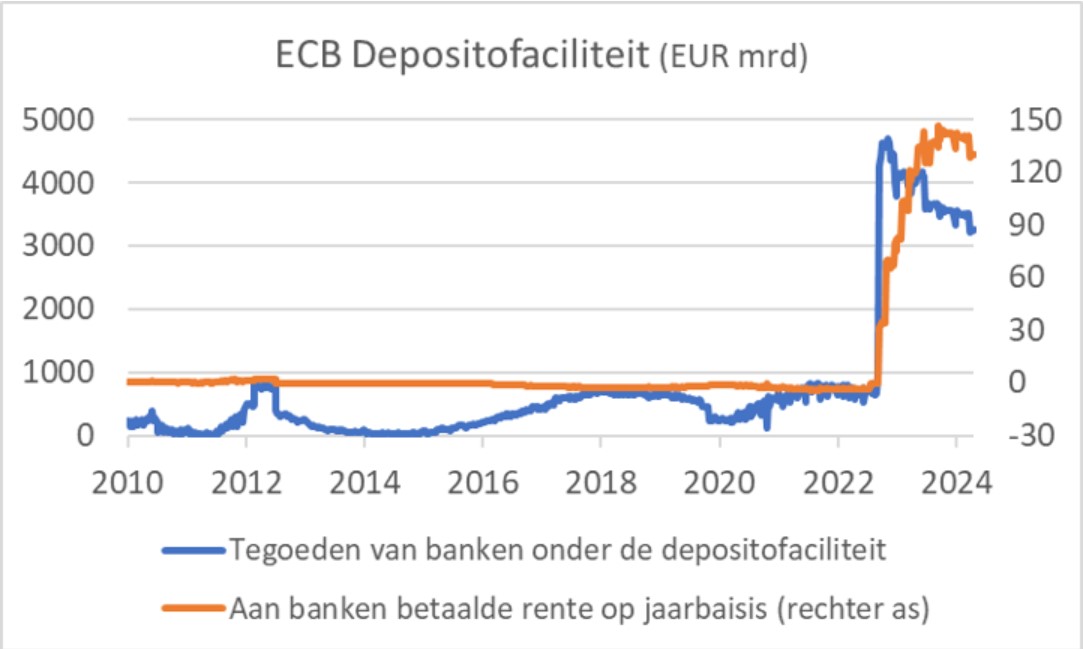

However, now that interest rates have risen sharply, the central bank's profit is turning into a loss, as we have seen. In a previous article Wrote. Central banks pay four percent interest on some of the huge reserves that the commercial banks hold, while on the other side of the balance sheet they still have the bonds with low interest rates. The ECB now pays 130 billion euros annually to banks, 0.9 percent of GDP. If the losses exceed the central bank's buffers, taxpayers may have to step in.

In addition, commercial banks only pass on the higher interest rate to the customer to a limited extent, since the banks have a huge amount of money at their disposal. Savers remain loyal to their own bank, which means that there is actually too little competition in the market. For the banks, according to De Jong, it is 'a case of sitting back and walking in'. ING's net profit in 2023 amounted to €7.3 billion. This was twice as many as in the previous year.

It remains to be seen what interest rates will do in the near future. In America, the central bank doesn't seem to be in a hurry yet. First, inflation in America is falling at a slower pace than expected. In addition, the economy is still doing very well. So the need to lower interest rates is not there yet. In Europe, the ECB appears to be preparing for a rate cut in June, it said Han de Jong to Holland Gold last month. There now seems to be room for that. In April, inflation in the eurozone was 2.4 percent. Core inflation fell from 2.9 to 2.7 percent in March compared to March. This means that the inflation rate is not far from the policy target of two percent. And since the effect of previous rate hikes is not yet fully felt, inflation that continues to fall is in line with expectations.

In the Netherlands, inflation was slightly higher. In April, the price increase was 2.7 percent. In March, this was still 3.1 percent. Inflation fell in the services sector in particular due to moderating wage growth. The services sector experienced the most persistent inflation, as it is very labour-intensive. If wages rise in that sector, this results in higher inflation than in other sectors that are less labour-intensive. Over the past year, wages have risen in many sectors, resulting in higher inflation.

Many economists have the impression that the ECB's asset purchase policy is now leading to High inflation. Madelon Fox rightly pointed to two contradictory reports from the Dutch Central Bank (DNB) about inflation. She also pointed to the fact that DNB ignores money creation. However, it is important to mention that QE does not equate to monetary financing. In the case of monetary financing, the central bank buys bonds directly from the government and there is no brake on money creation, so it quickly leads to hyperinflation. But the central bank's purchasing policy was channelled through commercial banks. So the central bank never directly bought government bonds. As a result, QE did not directly lead to high inflation, he said Isabel Schnabel, member of the Executive Board of the ECB.

Indirectly, QE did make an increase in the general price level possible. For example, the policy leads to wealth effects and a growing money supply facilitates inflation in the event of a price shock, Professor Lex Hoogduin explained in a podcast with Holland Gold: 'If you have a constant money supply and there is a shock, energy prices will rise and other prices will fall. However, the general price level remains the same,' Hoogduin said. Now the money supply is accommodating inflation, although the current inflation is not a direct result of QE. In fact, before the energy crisis, QE actually failed, economist argued Mathijs Bouman in a podcast at Holland Gold. In the years before the war in Ukraine, the ECB failed to raise inflation, despite very loose monetary policy.

It is interesting that bonds are once again fulfilling the traditional role in the economy. In the near future, it will become clear whether central bank interest rates will indeed be lowered and what effect this will have.

On Thursday 16 May 2024, Holland Gold will host a event on Gold and world politics in the Georg Kessler Lounge at the AFAS AZ Stadium.

The event consists of three parts: one interview, one presentation and a Q&A session for the audience. For example, the gold rush is discussed in World Politics, the geopolitical tensions that are rising every day; in Ukraine, the Middle East, in West Africa and around Taiwan. What impact does this have on the financial system? Central banks seem to be caught in a gold rush. The yellow metal achieves a Record price. How long will the US dollar remain dominant?

Buy your tickets here: https://www.hollandgold.nl/evenement/

Have a look at us YouTube channel

On behalf of Holland Gold, Paul Buitink and Joris Beemsterboer interview various economists and experts in the field of macroeconomics. The aim of the podcast is to provide the viewer with a better picture and guidance in an increasingly rapidly changing macroeconomic and monetary landscape. Click here to subscribe.