9.2

8.874 reviews

English

EN

This article has been automatically translated from Dutch. Click here to see the orginal article including all links to sources.

In Asia, Singapore’s Prime Minister warns of a “messy” transition toward a multipolar world, while in Europe, France continues to sink deeper into fiscal trouble. Yet French politicians keep pressing the accelerator, driving ever faster down a dead-end road. How much longer can this go on?

In an interview with the Financial Times, Singapore’s Prime Minister Lawrence Wong warned of turbulent times ahead. He foresees a “messy” transition from a post-American world order to a multipolar one and emphasized that no single country can fill the vacuum left by the U.S.: “There is no doubt it will be messy and unpredictable.”

“We find ourselves in an uncomfortable position where the old rules no longer apply, while the new ones have yet to be written. We must brace ourselves for the turbulent times ahead,” Wong said. He expects profound structural changes in the world and believes we are in the midst of a major transformation that could last a decade.

Prime Minister Wong during his interview with the Financial Times (source: FT)

According to Wong, Singapore as a trading nation cannot simply wait and hope for the best. He calls for action: building new trade links and maintaining the momentum of trade liberalization together with like-minded countries. “We live in a world where the global system is becoming increasingly clogged. But we want to keep the arteries of trade open and perhaps even create new ones.”

Wong stated that China is neither ready nor willing, for now, to replace the United States as the dominant power in the global system. He stressed that Singapore wants to maintain strong relations with both superpowers.

Reading tip: China accelerates de-dollarisation. Foreign lending in renminbi is surging as Beijing aims to use the currency for trade and investment, speeding up the shift from a dollar-based to a multipolar monetary system.

France’s government has a serious budget problem — a fact our regular readers are already aware of. The public sector now absorbs 58% of the economy, and the budget deficit stands at around 6%. But what is the plan to fix this?

Earlier this month, we reported that pension spending accounts for 25% of total public expenditure. Since President Macron took office in 2017, public debt has increased by €812 billion, of which 44% went to pensions. You’d think cutting pension costs would be priority number one — but nothing could be further from the truth.

Prime Minister Sébastien Lecornu (yes, he’s back again) has now proposed suspending Macron’s pension reform to prevent his fragile minority government from collapsing. This move temporarily secures support from the Socialist Party.

French President Emmanuel Macron (source: World Economic Forum)

Concretely, this means a temporary halt to the gradual increase of the legal retirement age from 62 to 64. In the short term, the financial impact is limited, reports Le Monde: the suspension will cost €400 million in 2026 and €1.8 billion in 2027. But the long-term sustainability of the pension system — and thus the public finances — remains an open question.

Economists and rating agencies are far less optimistic. Standard & Poor’s downgraded France’s credit rating last Friday, warning that public debt will rise faster than previously expected. It was the third downgrade in about a month. France’s rating was cut from AA- to A+, with S&P forecasting public debt to reach 121% of GDP by 2028.

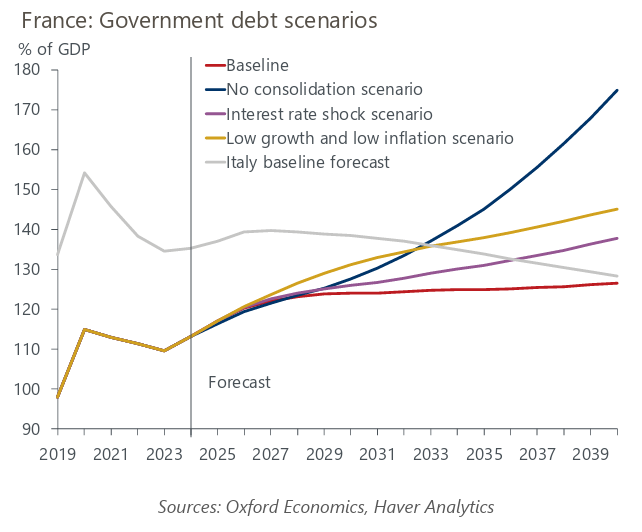

Projected French debt growth (source: Oxford Economics)

Oxford Economics expects the debt ratio to reach 125% by 2035 — and in a scenario of prolonged political paralysis blocking fiscal reform, debt could climb to 145% of GDP by then. They foresee rising borrowing costs for France, while economic growth is expected to fall below 1% by 2030 due to an ageing population. The gap between the average interest rate on public debt and nominal GDP growth will worsen. By the early 2030s, the average interest rate will likely exceed economic growth. By 2035, France will rank among the developed economies with the worst debt positions.

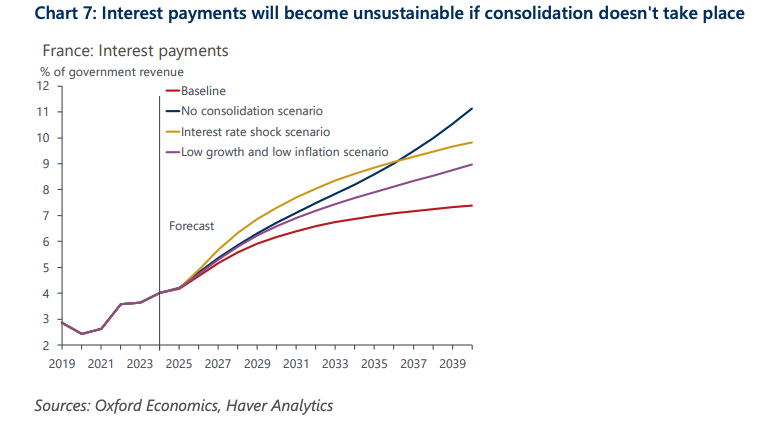

Debt service becomes unsustainable without fiscal improvement (source: Oxford Economics)

This means France must generate budget surpluses (excluding interest payments) just to keep its debt-to-GDP ratio stable. Oxford Economics doesn’t expect an acute debt crisis in the near term, but sees a “slow erosion” scenario as highly likely: persistently higher interest rates than growth, gradually shrinking fiscal space, and mounting debt. As in Italy, this would weigh heavily on growth, as the government would be forced into tighter budgets to offset rising interest costs.

In the meantime, France will have to raise taxes, cut spending, or both. We’ve written before about why reforming in France is so difficult. Experts expect meaningful reforms or spending cuts only after the 2027 presidential elections. In the meantime, tax hikes are already being discussed: a wealth tax, higher digital taxes on large U.S. tech companies, and a proposed tax on global income of French citizens who relocate abroad to low-tax jurisdictions.

But such measures could easily backfire, as seen in the UK and Norway, where tax hikes led to lower revenues — a classic case of the Laffer curve. Higher tax rates don’t automatically mean higher income when people adjust their behavior. Beyond a certain point, tax increases are a dead end.

A more effective approach would be to boost economic freedom by lowering taxes and reducing the size of government and bureaucracy. France could then attract talent and investment again. As we noted earlier, 15% of graduates from France’s top engineering and business schools leave the country, mainly due to high taxes and low net wages.

This week, the Financial Times published an article titled “France’s wealthy shift funds to Luxembourg and Switzerland.” Asset managers, bankers, and tax experts report that capital flight from France to safe havens has sharply increased amid political turmoil. Some wealthy individuals have even moved abroad permanently, not only for tax reasons but also due to growing political uncertainty. Still, most prefer to move their assets first, since relocating physically is complex from a legal and fiscal standpoint.

We will, of course, continue to monitor the situation. For now, one can only hope that the Netherlands will not join France in issuing common debt. Both Han de Jong and Kees de Kort agreed in our podcast that such a move would be very unfavorable for Dutch taxpayers. They also shared their views on how long this situation can continue. To be continued.