9.3

8.709 reviews

English

EN

Which factors impact the price of gold? Gold has declined significantly since the beginning of January. This raises questions: why is gold falling while geopolitical tensions are increasing and inflation is looming? Gold is generally seen as a hedge against uncertainty and currency debasement.

The answer lies in valuation. Stocks and bonds generate cash flows that can be valued. Gold does not generate these, and traditional valuation models do not apply. Its value is determined by macroeconomic factors that make gold more or less attractive relative to alternatives. Which factors drive the gold price, and which pose risks?

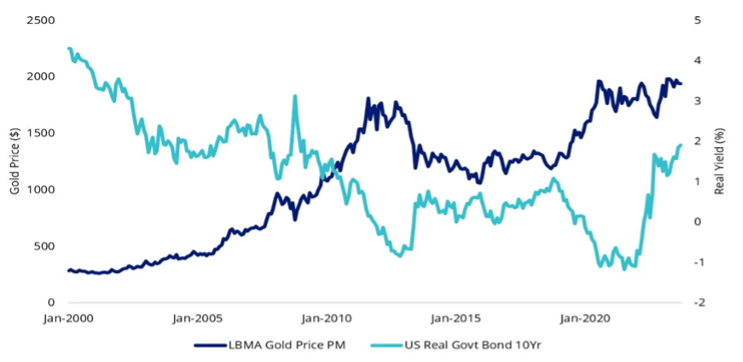

The value of gold is closely linked to its opportunity cost – what is foregone by holding gold. The key measure of this is the real interest rate: the interest rate adjusted for inflation. When this rate is high, holding currencies or bonds becomes more attractive, as they provide both purchasing power and yield. When it is low or even negative, meaning that holding currency erodes purchasing power, bonds become less attractive and gold becomes an important alternative. This principle is reflected in the gold price: periods of low real interest rates have historically been characterized by strong gold performance.

Gold price correlation with real interest rates. (Source: VanEck)

Current changes in interest rates affect the opportunity cost of gold. Although inflation expectations are rising due to the conflict in the Middle East, Fed Chair Jerome Powell stated that policymakers are in a good position to wait and see how the situation develops. If the conflict persists and inflation rises, an interest rate hike to combat it is likely. If it turns out to be a short-lived shock, a rate hike becomes less likely.

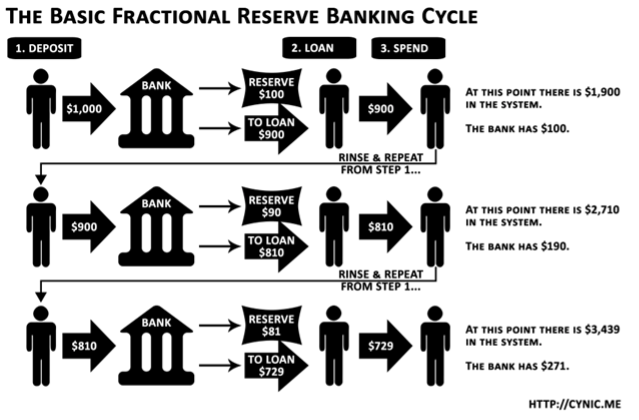

Gold is known as a reliable hedge against inflation. Historically, it has preserved its purchasing power at times when currencies did not. An important cause of this loss of purchasing power is fractional reserve banking.

Within this system, banks are only required to hold a fraction of deposits as reserves. When a customer deposits 100 euros, the bank lends out part of it, for example 50 euros. There are now two claims on the same money: the saver still has access to their 100 euros, while the borrower holds 50 euros. The money supply increases from 100 to 150 euros.

This process repeats itself. The 50 euros that were lent out are deposited elsewhere and partially lent out again, and so on. One initial deposit can thus generate a multiple of the original money supply. As this money enters the system without a corresponding increase in the production of goods or services, inflation arises.

Gold acts as a counterbalance. Its supply is scarce and cannot simply be created. While currencies are debased, gold preserves its purchasing power and rises when expressed in those currencies.

As the debt ceiling in the United States continues to be raised, concerns are growing about the sustainability of government debt. Jerome Powell himself warned that the debt is not sustainable in the long term, as it is rising faster than the economy.

When government debt becomes too large, investors demand higher interest rates to compensate for the risk that the government may not be able to meet its obligations. This increases financing costs and limits room for other spending. If doubts about repayment grow, this can spill over into the broader financial system. Banks often hold large amounts of government bonds on their balance sheets: falling prices or defaults can put pressure on the sector, according to De Nederlandsche Bank.

Geopolitical tensions can further amplify this effect, as they put pressure on confidence in financial markets and governments. In such situations, investors more often look for ways to safeguard their wealth outside the traditional system. Gold is a safe option because it is decentralized and therefore less dependent on policy decisions by governments or central banks.

However, the picture is nuanced. In periods of sudden declines, gold can temporarily move in tandem with other assets. For example, during the initial phase of the COVID crisis, gold fell alongside the stock market, as investors needed liquidity and sold profitable positions to cover losses. Once the initial panic subsided, gold has historically tended to perform strongly in times of uncertainty.

Another major factor is the buying and selling of gold reserves by central banks. According to the World Gold Council, they hold 18% of the above-ground supply. Turkey sold 58.8 tonnes of gold over the past two weeks. Due to the large reserves held by central banks, their gold reserve policies have a significant impact on the gold price.

Demand from these banks mainly comes from non-Western and emerging economies, which have been buying gold since 2022, after Russia’s foreign exchange reserves were frozen, in order to gain greater autonomy. Since 2022, central banks have been purchasing twice as much gold per year as the average of the previous decade.

Gold is not a traditional investment because it does not generate cash flows. This makes valuation using traditional models impossible. As a result, its price depends on macroeconomic drivers. Higher inflation expectations can have a negative short-term impact on the price, as potential interest rate hikes increase real interest rates. However, low real interest rates, high inflation, uncertainty, and increasing central bank reserves remain fundamental drivers of the gold price and enhance gold’s long-term potential.