9.3

8.883 reviews

English

EN

In this weekly selection, we look at gold, Russia and the yield curve. As of today, Russia is buying more than seven times as much gold every day as before. We also see that a.o. Bloomberg is positive on gold, as was the Financial Times last week. In addition, there is news about the yield curve, a classic recession indicator. And finally, we take a brief look at a new figure on the housing market.

Today starts Russia with a drastic increase in his daily gold purchases. Russia will spend 8.2 billion rubles a day on buying gold at least until October 4. In total, it is almost 173 billion rubles, or $1.9 billion. This is an increase of more than 600% compared to last month, when the country bought 1.12 billion rubles worth of gold per day.

As Western sanctions against Russia become increasingly severe, the country is turning to precious metals to circumvent financial constraints. Russia has collaborated with China on a New approach where gold is used as a means of payment for goods and services. The process involves the purchase of gold in Russia, which is then transported to Hong Kong for sale. The proceeds from this sale will be deposited into local bank accounts.

There are also suspicions that in recent years, despite sanctions, Russia sold gold to a.o. Switzerland via Uzbekistan and Kazakhstan. After the invasion of Ukraine by Russia, gold imports from Uzbekistan and Kazakhstan to Switzerland increased sharply. An analysis of trade data shows that these countries exported more gold than they produced in 2023, with many experts pointing to Russia as the most logical source.

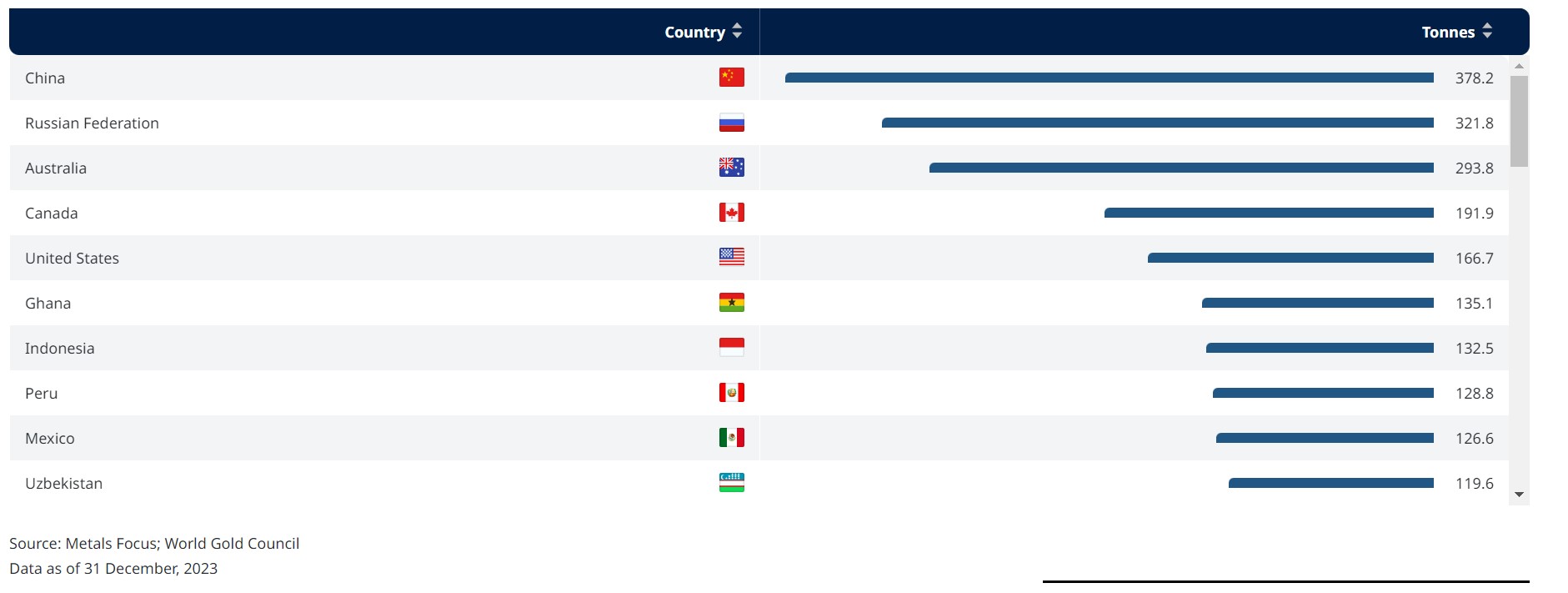

Russia uses the revenue from the sale of gas and oil now to buy the extra gold. The country has also been one of the largest gold producers for a long time. Last year, only China produced more gold. Earlier we read that Russia is not only engaged in gold production in our own country, but also a deal Mali, the world's 11th gold producer, has made over building a state-of-the-art gold refinery in the capital, Bamako. The refinery would be 200 tons gold.

Largest gold producers in 2023 (source: World Gold Council)

Analyst Jon Forrest Little says this shift to gold as a means of payment is more than a temporary workaround; rather, it is a return to a more fundamental and time-tested form of economic exchange. He argues that gold's intrinsic value and its historical role as a universal medium of exchange make it a more reliable option than fiat currencies, especially during times of geopolitical uncertainty.

Last week we wrote about an article in the Financial Times in which it is written that there is a structural tailwind for the demand for gold, partly due to Western sanctions and the freezing of Russian reserves. This week, not only the FD with a similarly positive article about gold, but also Bloomberg with an article about gold as "fallback money". The author writes that gold is a "forever asset" and should be part of your core portfolio. "Central banks own gold and always have, even at the lowest points of the market. If they still consider gold to be an essential part of the monetary system, that's probably something you need to pay attention to." Also Goldman Sachs came up with a similar advice to investors this week.

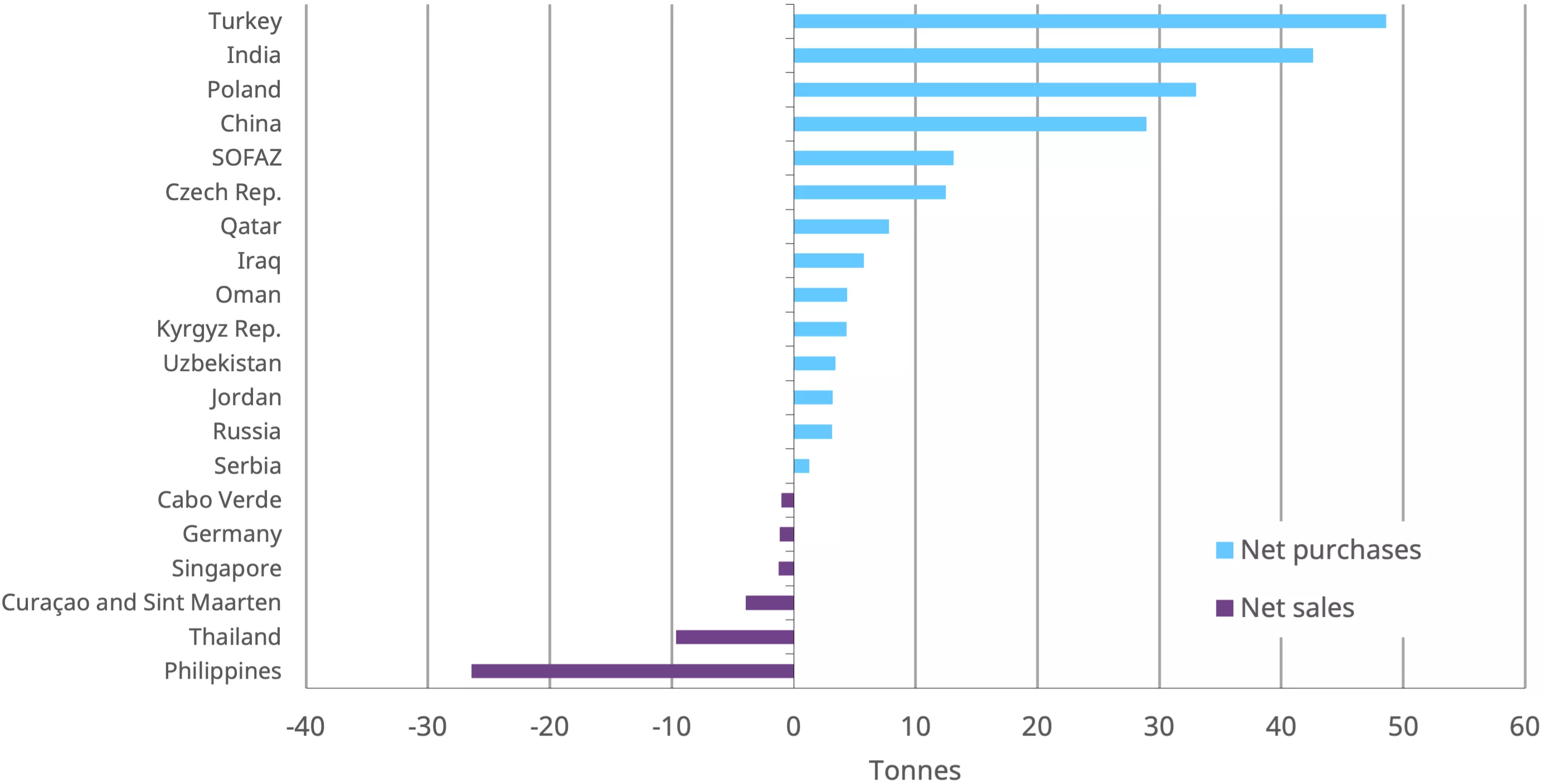

This week, the World Gold Council published the statistics on central banks' gold purchases in July 2024. According to the official figures, the central banks of Poland and Uzbekistan were the biggest buyers in that month, with 14 and 10 tons of net purchases respectively. This year, central banks have bought significantly more gold than they have sold, and the World Gold Council expects demand for gold from central banks to increase further in the coming months.

Gold purchases by central banks this year until July 31, 2024 (source: World Gold Council)

The relationship between 10-year and 2-year U.S. Treasury yields Normalized and briefly rose above 0 on Wednesday. This happened after the longest reversal of the Yield Curve ever. The inversion of the yield curve is seen as an important Recession signal.

The yield curve and recessions. Difference between 10- and 2-year state obiligations. (Source: Federal Reserve Bank of St. Louis)

The yield curve typically reflects market sentiment about the economic outlook, especially in terms of inflation and the policy that the central bank will follow. The yield curve is a visual representation of the difference in the return investors receive for short-term versus long-term debt. Most of the time, bond investors demand higher yields because of the greater uncertainty associated with locking up their money for longer. Therefore, the yield curve normally runs upward. A yield curve inversion occurs when the yield on long-term bonds is lower than that on short-term bonds. Historically, an inverted curve is often followed by a recession in the U.S.

The recovery of the normal upward slope of the yield curve typically happens when the Fed starts cutting rates, or when markets start pricing in future rate cuts. Since the central bank usually eases policy when the economy is doing worse, some say that 'Disinversions' are often a sign of a coming recession, not the reversal itself. A viewing tip for anyone with an interest in this topic is this video in which everything is explained with graphs.

In August Wrote house prices rose by almost 11 percent in July compared to the previous year. This week, Statistics Netherlands (CBS) published remarkable figures on rents. House rents were on average 5.4 percent higher in July 2024 than in July 2023. This is the Largest rent increase since 1993. The largest rent increase took place in the municipality Rotterdam, where rents rose by an average of 5.9 percent.

Rent increase (source: CBS)

In this week's monthly update, Frank Knopers discussed the housing market and the dichotomy that is emerging in society due to the problems in the housing market. He also shares an interesting graph that shows that house prices, measured in gold, have not become more expensive at all. Watch the episode back here.

(photo: Kremlin)

Have a look at us YouTube channel

On behalf of Holland Gold, Paul Buitink interviews various economists and experts in the macroeconomic field. The aim of the podcast is to provide the viewer with a better picture and guidance in an increasingly rapidly changing macroeconomic and monetary landscape. Click here to subscribe.