9.3

8.709 reviews

English

EN

This article has been automatically translated from Dutch. Click here to see the orginal article including all links to sources.

You regularly read that the rise in precious-metal prices such as gold and silver is linked to growing government debt. Economist Daniel Lacalle put it sharply this week: “Gold is reflecting the destruction of purchasing power of fiat currencies.” What does he mean by this, how does this mechanism work, and are we currently seeing a debt crisis emerge?

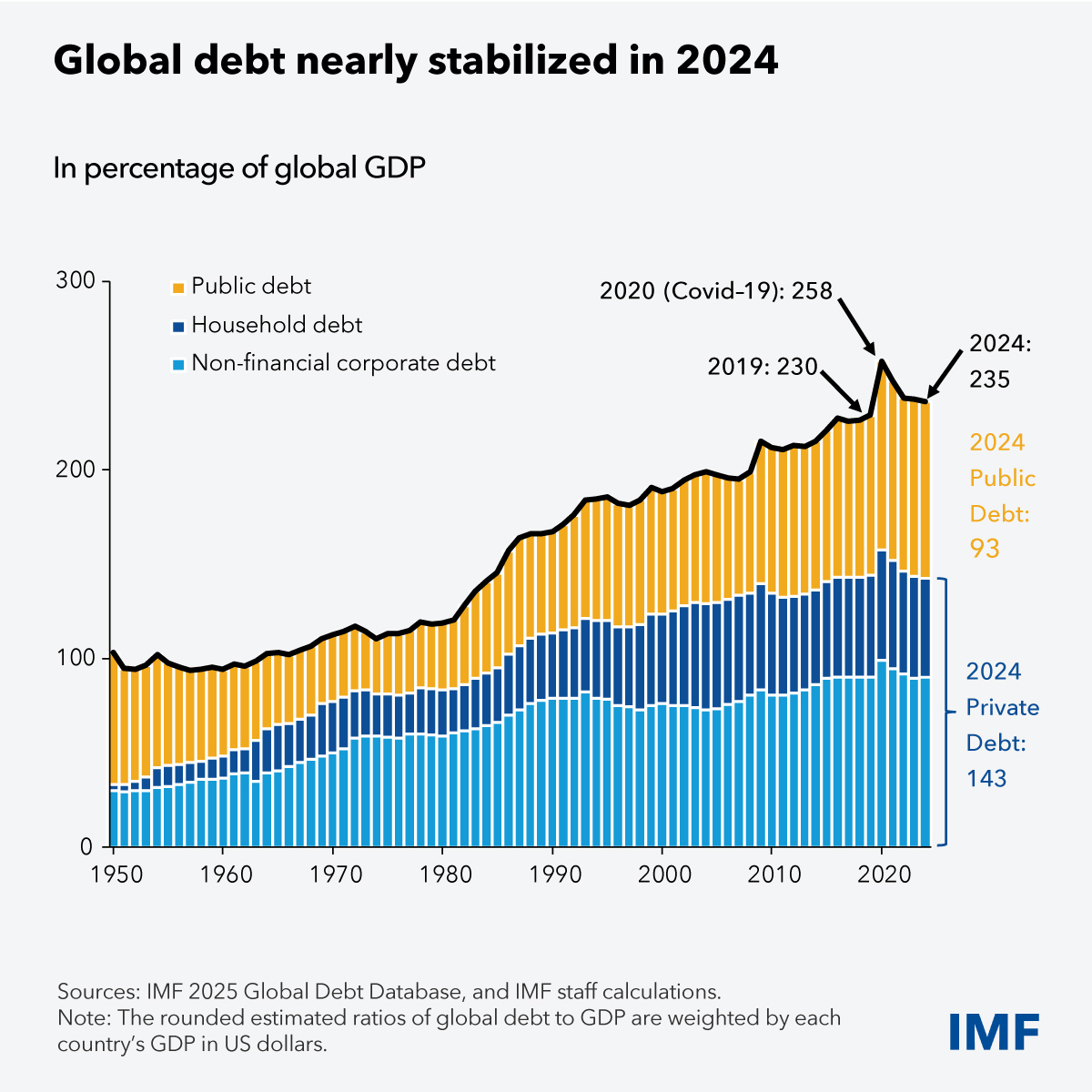

According to the IMF, global debt currently stands at a high level of 235 percent of global gross domestic product. Of this, 143 percent consists of private debt and 93 percent of government debt. The IMF observes that the share of government debt has increased in recent years.

Development of global debt according to an IMF publication from September 2025 (source: IMF)

The chart above shows that this is historically a high level of debt. Only during the Covid period was global debt slightly higher. Until the 1980s, a debt level of around 100 percent of GDP was common; since then it has increased sharply. In this weekly selection, we focus on government debt. The reason for this will become clear, but first follows an overview of global government debt.

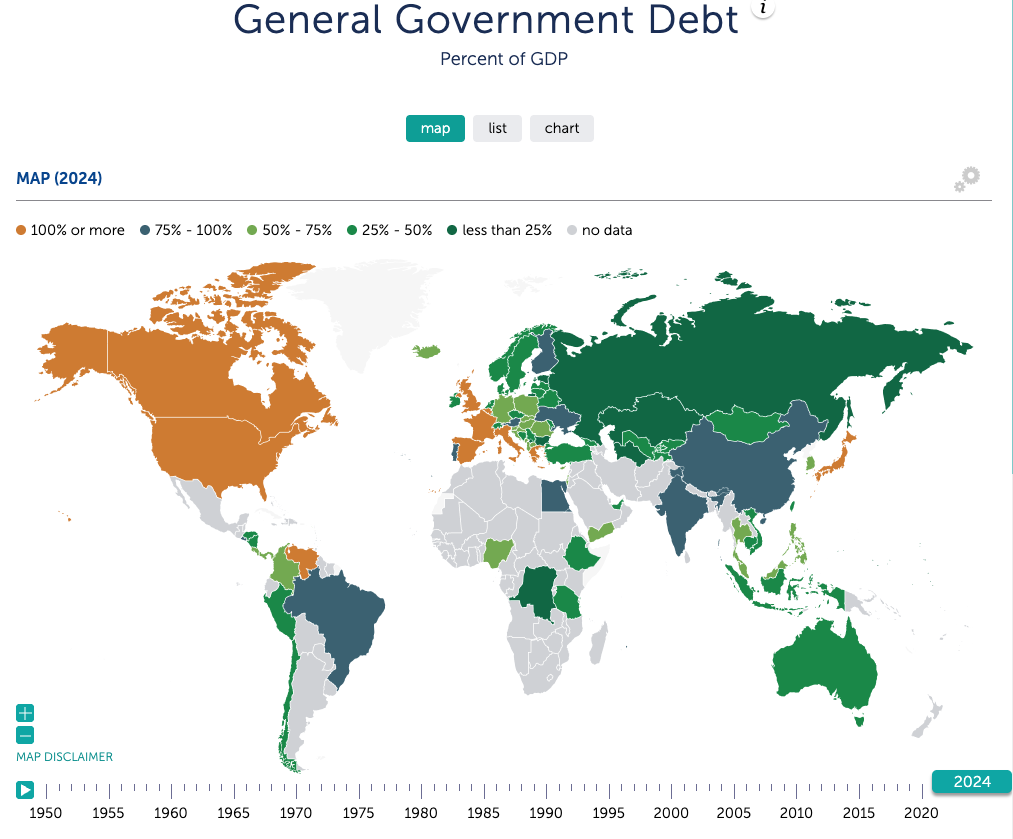

Government debt ratios worldwide (source: IMF)

Developed economies in particular have debt ratios exceeding 100 percent. The Netherlands forms a positive exception, with a debt level of 43 percent of GDP, although a substantial increase is expected in the coming years. To better understand why high government debt drives investors toward safe havens such as gold, we look at the country with the largest economy and the country with the highest debt ratio.

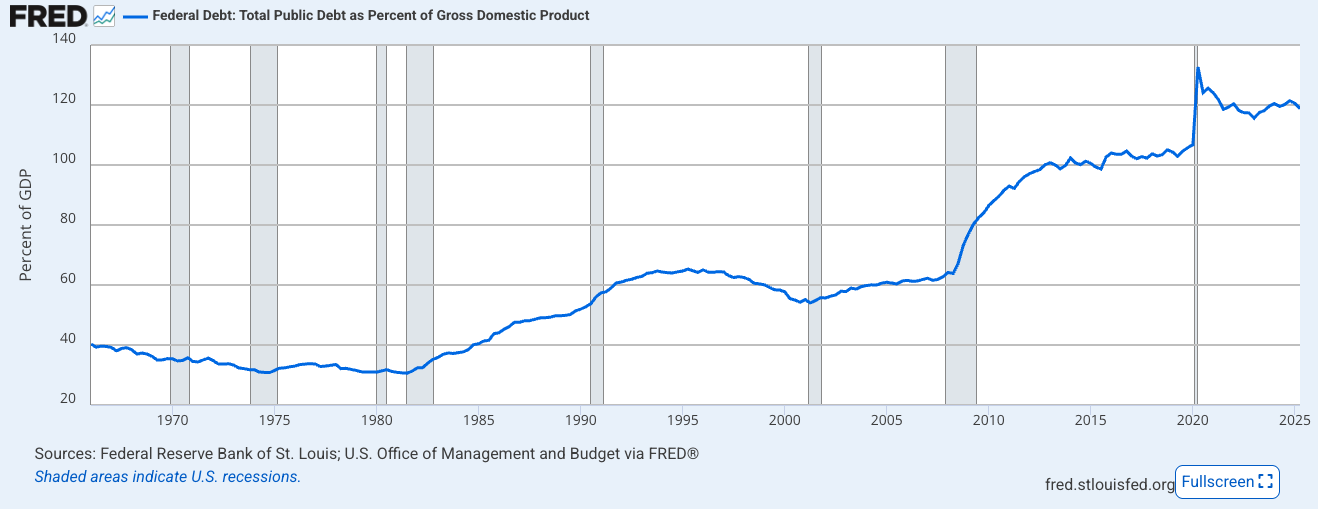

The United States has been struggling for years with large budget deficits and a rapidly rising national debt. U.S. government debt is now approaching $39 trillion, roughly 120 percent of GDP.

Development of U.S. government debt (source: St. Louis Fed)

Fortune wrote this week that interest expenses on this debt are becoming an increasingly serious challenge. In fiscal year 2025, the United States paid $952 billion in interest, compared with $375 billion in 2019. This represents an increase of 153 percent over six years.

Interest expenses have now become the third-largest spending category of the U.S. government, after Social Security and healthcare. At 3.2 percent of GDP, these costs weigh heavily on the economy, and this share is expected to rise further. In fiscal year 2026, interest expenses even temporarily ranked as the second-largest budget item, exceeding Medicare and defense. Between fiscal years 2019 and 2025, the share of interest in total federal spending rose from less than one dollar in ten to more than one dollar in 6.5.

Earlier, we already wrote extensively about similar problems affecting the French government budget and interest expenses.

Normally, a government can reduce its budget deficit to prevent interest costs from spiraling out of control. When debt declines relative to the size of the economy, risk for lenders decreases and interest rates can fall. Many Western governments, however, are failing to reduce their budget deficits, partly due to the effects of population aging. In the United States, interest expenses themselves are increasingly becoming a driver of the budget deficit, which currently stands at around 6 percent of GDP.

According to leading economists, the rapidly rising federal debt represents one of the biggest challenges for the U.S. economy. What now threatens, former Fed Chair Janet Yellen warns, is a situation in which the solution is no longer sought from the government, but from the central bank.

Fiscal dominance is the situation in which the size of government debt compels the central bank to keep interest rates low in order to limit debt-servicing costs, rather than focusing on fighting inflation. Fiscal policy then becomes dominant over the central bank’s monetary policy. In such a situation, the central bank can no longer properly pursue its primary objective of price stability, because it must take the sustainability of government debt into account.

Under fiscal dominance, central banks may therefore choose to lower or keep interest rates low despite high inflation. Inflation can also be used to ease the debt burden, and central banks may purchase government debt with newly created money, for example through quantitative easing (QE). As a result, fiat currencies, and in this case the dollar, lose value.

You have likely already read that President Trump is increasingly putting pressure on the independence of the Fed, among other things by pushing for interest-rate cuts. According to U.S. bank Citibank, this could also become a problem in Europe in the coming years.

There is a widespread belief that the threshold for a debt crisis in developed economies is very high. Central banks would be able to create money and purchase government bonds when interest rates rise too sharply, without significantly affecting inflation. Economist Robin Brooks explains why he believes this is incorrect.

When government debt is sufficiently high, negative shocks can lead to sharp increases in interest rates, because investors then rightly factor in a further rise in public debt. If the central bank continually absorbs these rate increases, any incentive for politicians to reduce debt and pursue prudent fiscal policy disappears. According to Brooks, this will ultimately lead to unanchored inflation expectations.

It is far from certain that central banks will succeed in capping bond yields. But even if they do, they cannot prevent the currency from losing value. “If risk premia are artificially suppressed in the bond market, they will simply manifest themselves through a weaker exchange rate,” Brooks states.

In a debt crisis in developed economies, the national currency will therefore lose value even if interest rates rise, whereas higher interest rates would normally lead to a stronger currency. He sees this type of debt crisis currently emerging: “The bottom line is that debt crises in the G10 are very much possible. In fact, we’re already seeing them play out in real time.”

One country where Brooks currently sees this happening is Japan. The country’s debt ratio is now above 230 percent, and the Japanese central bank is pursuing policies aimed at limiting interest-rate increases by purchasing large quantities of government bonds. The risk premium that would normally be reflected in higher yields is now showing up in the exchange rate.

The price of silver in Japanese yen (source: Robin Brooks / Bloomberg)

The yen is losing value against other currencies, such as the euro. This depreciation is even more pronounced in the price of precious metals, which cannot be “printed” by central banks and therefore cannot be weakened in the same way.

Brooks uses the price of silver denominated in Japanese yen to illustrate his point. “The flight to safe havens such as precious metals is about trying to escape debt monetization. Nowhere is this fear as pronounced as in Japan. Japan is at the center of the global debasement trade,” Brooks concludes.

To be continued!