9.2

8.858 reviews

English

EN

The Silver Institute recently launched a report in which they focus on the future demand for industrial silver, focusing specifically on the period from 2023 to 2033. In today's rapidly evolving industrial world, forecasting demand for precious metals like silver is essential for various stakeholders, including producers, investors, and policymakers. In this article, silver usage has been split into three major industrial categories: electrical and electronics, solder alloys, and other miscellaneous applications as detailed in the World Silver Survey 2023.

The electrical and electronics industry is a significant buyer of industrial silver, accounting for about 67% of the silver used for industrial purposes in 2022. This industry includes manufacturers of computers, electrical equipment, and general machinery, all of which rely heavily on silver for a variety of applications.

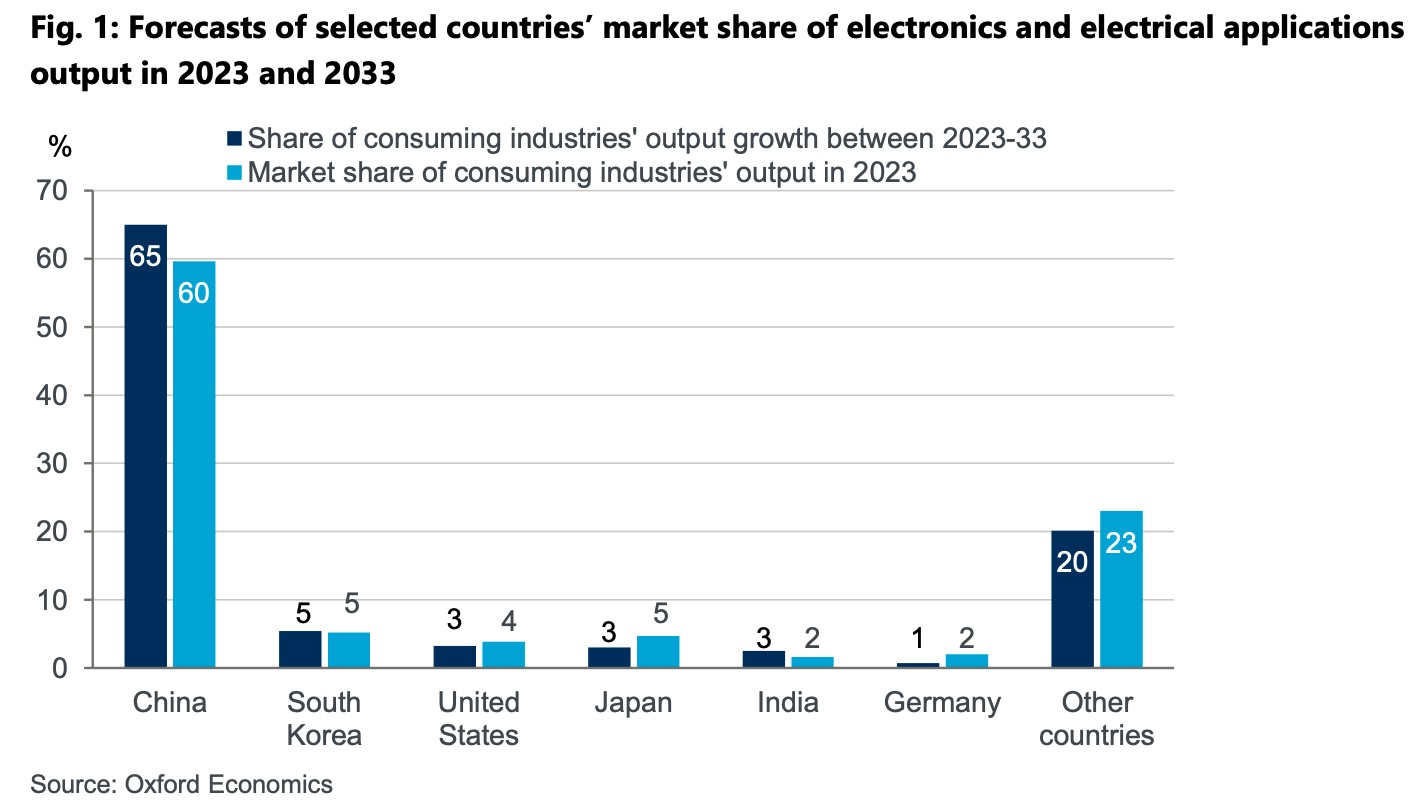

Over the next decade, global manufacturing in the electronics and electronics applications industry is expected to grow by an impressive 55%. This significant growth will be primarily driven by China, which is expected to capture a significant 65% of global growth in electronics and electronic applications manufacturing between 2023 and 2033. South Korea, the United States, and Japan are also expected to contribute significantly to this growth.

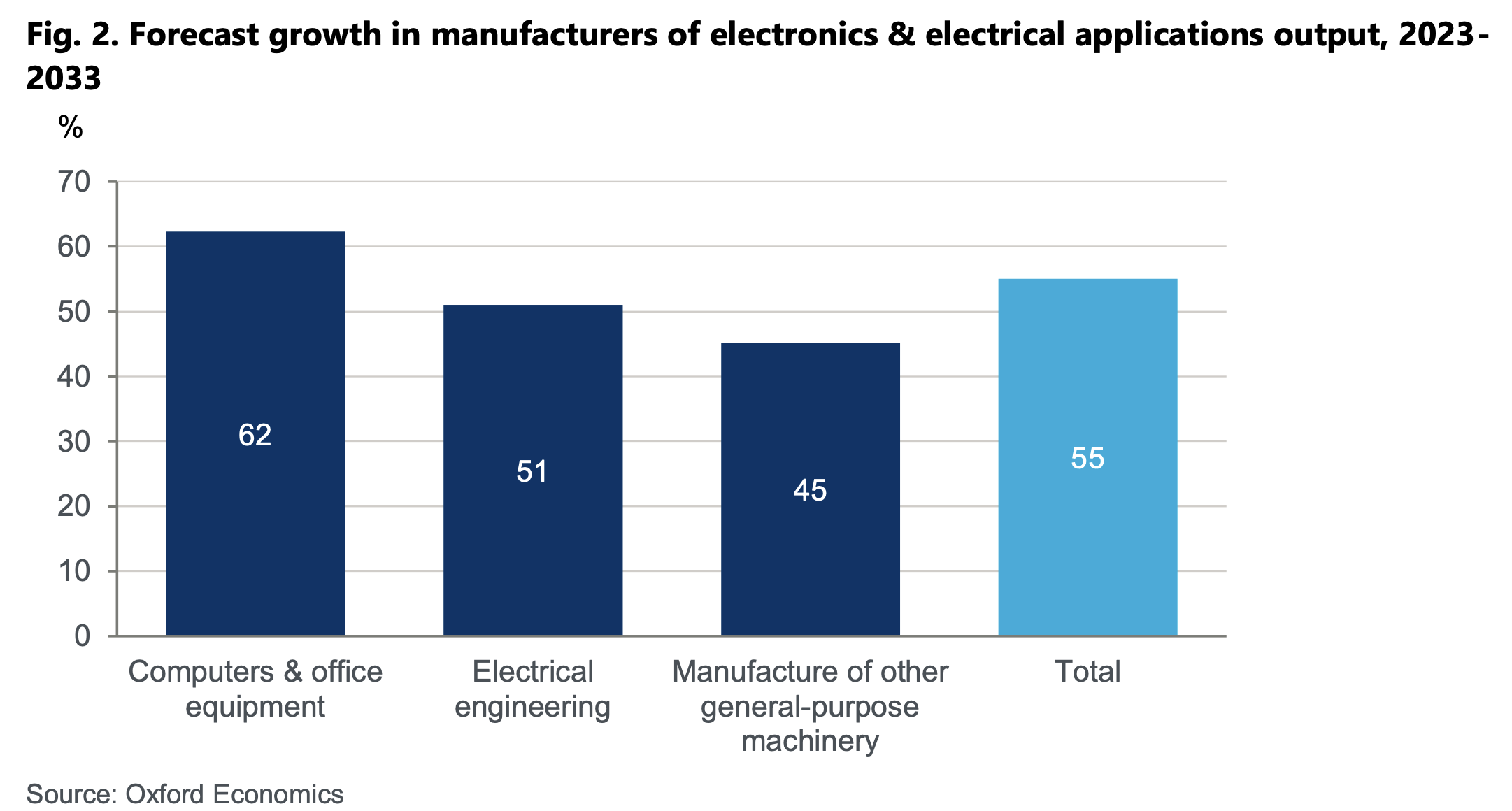

The fastest-growing sector within this industry is the manufacturing of computers and office equipment, with a predicted 62% increase in manufacturing between 2023 and 2033. Products from electrical engineering and other general machinery are also expected to grow, albeit at a slightly slower pace.

Solder alloys, which require silver as a key component, made up 9% of global industrial silver demand in 2022. The main consumers of silver for solder alloys were China, the United States, and Germany.

Forecasts for the next decade indicate that the total production of industries that use silver for solder alloys will increase by 34% between 2023 and 2033. This growth will be driven by key sectors such as motor vehicle manufacturing, electronic components and boards, general machinery, iron and steel production, and structural metal products.

China is expected to play a dominant role in this growth and will contribute 41% to the expansion of production. India and South Korea are also expected to contribute significantly to the growth of industries that use silver for solder alloys.

About 24% of industrial silver demand in 2022 fell under "other industrial applications," which includes a wide range of applications not covered by electrical/electronic or solder alloys. To understand how this demand will evolve, forecasts for the gross output of all manufacturing industries (with the exception of the two categories mentioned earlier) were analyzed.

Over the next ten years, the production of these end-user industries is expected to increase by 26%. China is predicted to generate 48% of this growth, while the United States, Japan, South Korea, and France are also contributing to the expansion of production.

By weighting the growth forecasts of these three main segments based on their silver consumption in 2022, we can deduce that the demand for industrial silver will increase by 46% in real terms between 2023 and 2033. Remarkably, the electrical and electronic applications industry is expected to show the fastest growth, with a 55% increase in manufacturing.

Growth in silver demand is predicted to be faster in the first five years (2023-2028) compared to the second half of the decade (2028-2033). In addition, China is expected to play a crucial role, contributing 51% to the growth of the production of industries that use silver as an intermediate.

The jewellery industry is a significant buyer of silver, with 71% of silver manufactured for jewellery coming from Asia in 2022, mainly India. Forecasts indicate that the demand for silver in jewelry production will increase by 34% between 2023 and 2033.

Silverware production, classified under the structural metals production industry, relies heavily on silver. In 2022, India, Nepal, and China were the top consumers of silver for silverware production. Over the next ten years, the industry's production of structural metals, weighted by the use of silverware makers, is expected to increase by 29%.

Finally, this analysis provides insight into the future demand for industrial silver, which spans various industrial sectors. It highlights the significant growth expected in industries such as electrical and electronic applications, solder alloys, and jewelry, with Asia, particularly China and India, playing a crucial role in driving this demand. These predictions provide valuable guidance for stakeholders in the silver production industry, allowing them to navigate changing market dynamics and make informed decisions over the next decade. However, it is essential to recognize the possibility of unforeseen challenges or economic shocks that could affect these forecasts. On our course page you can see how the Silver price has developed in recent years.