9.3

8.837 reviews

English

EN

Although palladium is relatively unknown among private investors, it is a widely used precious metal in industry. It plays a particularly important role in the automotive industry by filtering harmful exhaust gases. Stricter emissions requirements and concerns about geopolitical sanctions pushed the palladium price to a record high in 2022. Since then, the price has come under pressure due to the rise of electric vehicles and expectations of a supply surplus. Is the price decline the beginning of a prolonged downturn, or could the combination of a recovering automotive industry and the emergence of new industrial applications create opportunities for a recovery?

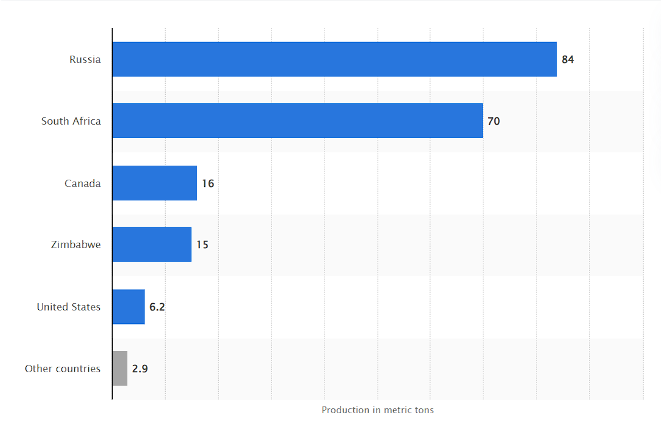

Compared with gold, silver and platinum, palladium is by far the scarcest precious metal. In 2025, global mine production amounted to only around 190 tonnes, compared with more than 3,000 tonnes of gold. This limited production is also difficult to scale up. Palladium is largely extracted as a by-product of platinum and nickel mining. Even when demand rises sharply, producers are therefore unable to increase output easily.

Palladium production (Source: Statista)

The geographical concentration of production also makes the market vulnerable. Around 80% of global supply comes from South Africa and Russia. Because of this high degree of concentration, geopolitical developments can have a major impact on the supply of the metal. This became particularly clear in 2022, when the palladium price rose to a record high amid concerns that Russia’s invasion of Ukraine would lead to sanctions that could disrupt supply.

However, the market has moved into the opposite situation in recent years. Despite palladium’s scarcity, there is currently a supply surplus. Analyst Jeroen Vandamme pointed out in the Holland Gold Podcast that high inventories are being combined with a rapidly increasing supply of recycled palladium from scrapped vehicles. As catalytic converters from vehicles produced fifteen to twenty years ago are recycled in large numbers, increasing amounts of palladium are returning to the market. As a result, shortages appear less likely for the time being, while the risk of a persistent supply surplus is increasing.

The demand side of the palladium market is also relatively undiversified. Around 85% of global palladium consumption comes from the automotive industry, where the metal plays an essential role in catalytic converters that transform harmful exhaust gases into less harmful substances. Since the introduction of stricter emissions standards, such as the Euro 6d regulations, car manufacturers have also been required to use more palladium per vehicle in order to comply with the rules.

The rise of hybrid vehicles also offers opportunities for palladium demand. Because the combustion engine in a hybrid vehicle regularly switches on and off, the catalytic converter takes longer to reach its optimal operating temperature. Palladium performs better than platinum under these conditions, meaning that hybrid vehicles contain an average of 10% to 20% more palladium than a conventional petrol-powered car.

These positive developments are offset by the rise of fully electric vehicles. Because these vehicles do not have a combustion engine and therefore do not require a catalytic converter, their demand for palladium disappears entirely. For this reason, there is an active search for new applications for the metal.

For example, Russian producer Nornickel is investing 100 million dollars in a technology that uses palladium in lithium-sulphur batteries. These batteries are regarded as a promising successor to today’s lithium-ion batteries because of their high energy density and relatively low cost. Their limited lifespan, however, remains a major obstacle. According to Nornickel, the addition of palladium could extend their lifespan by around 1,000 charging cycles – equivalent to approximately 10 to 15 years. If the technology is successfully completed within three years, this application could generate around 47 tonnes of additional annual palladium demand.

New opportunities are also emerging within the hydrogen economy. Thanks to its unique ability to store and purify hydrogen while allowing only hydrogen to pass through it, palladium is increasingly being studied for applications in hydrogen fuel cells and other hydrogen technologies.

New markets are also emerging outside the energy sector. Last year, China purchased 20,000 ounces of palladium to test its use in the fibreglass industry. Following successful industrial trials lasting 300 days, researchers are now examining whether platinum can be replaced by palladium on a larger scale. If this transition is successful, it could eventually generate around 50 tonnes of additional annual demand.

Although palladium may be an interesting investment because of its applications in industry and new technologies, it remains a relatively small market. As a result, its price often reacts much more strongly to changes in supply and demand than the prices of gold or silver. Geopolitical developments, disruptions to mining operations and the market’s strong dependence on the automotive industry can cause the price to move sharply within a short period of time.

This makes palladium a fundamentally different investment from gold and silver. While gold and silver are primarily regarded as safe havens and stores of value, palladium is first and foremost an industrial commodity. Palladium is therefore not a safe haven like gold. However, the combination of scarcity, innovation and a sharply lower price still makes it a metal worth watching.