9.2

8.875 reviews

English

EN

Author: Jan Nieuwenhuijs

Because of the enormous amount of information on the internet, but perhaps the same amount of misconceptions on this subject, in this article we will discuss how the international gold market works and how the physical gold price is determined. After all, how can we ever understand gold if we don't know how the market works? We have divided this article into three parts. Below is part 1.

The physical gold price is determined by the supply and demand of physical gold. The global physical market can be divided into exchange trading and bilateral trading. In addition to the physical market, there are several gold derivatives markets that influence the physical market. To understand the whole apparatus, we will analyze the operation of gold exchanges, bilateral trading, and derivatives markets separately, and finally discuss the connection between derivatives and the physical market. Derivatives can also be traded on exchanges and bilaterally, but for the sake of clarity, we will deal with them separately.

It is important to mention that there is no single physical gold price. Because gold is a commodity, and the forces between commodity supply and demand are not the same in all locations—and energy and time are required to move commodities—the price of physical gold differs geographically. Moreover, physical gold exists in many shapes, weights, and purities. The manufacturing cost for bars is more or less fixed but comparatively cheaper for large bars due to their higher value.

What most people consider to be the spot price of gold is the price per troy ounce fine gold, derived from the trade in large bars in London ("loco London"). Large bars traded in London weigh around 400 troy ounces. The smaller a bar compared to "large bars," the higher the premium it will attract. Gold coins and jewellery enjoy even higher premiums per fine weight, due to even higher manufacturing costs. The "real price of physical gold" therefore depends on where you are located and which gold product you are trading.

The fine weight of a gold product is calculated as follows:

Fine Weight = Gross Weight * Purity

Collection of large bars. In wholesale, gold is always priced by fine weight. Large bars have a purity of at least "995.0 parts per thousand."

An exchange is a centralized market. Multiple gold contracts can be traded on each exchange. On the Shanghai Gold Exchange, for example, spot gold contracts are traded that range in size from 100 grams to 12.5 Kg. Supply and demand meet through the order book of the exchange. Simplified, some market participants require bid (buy) and ask (sell) Limit Orders in the order book, while others bid and ask Market Orders submit. The orders are linked to each other via a computer, after which the orders are fulfilled, and so the price is determined.

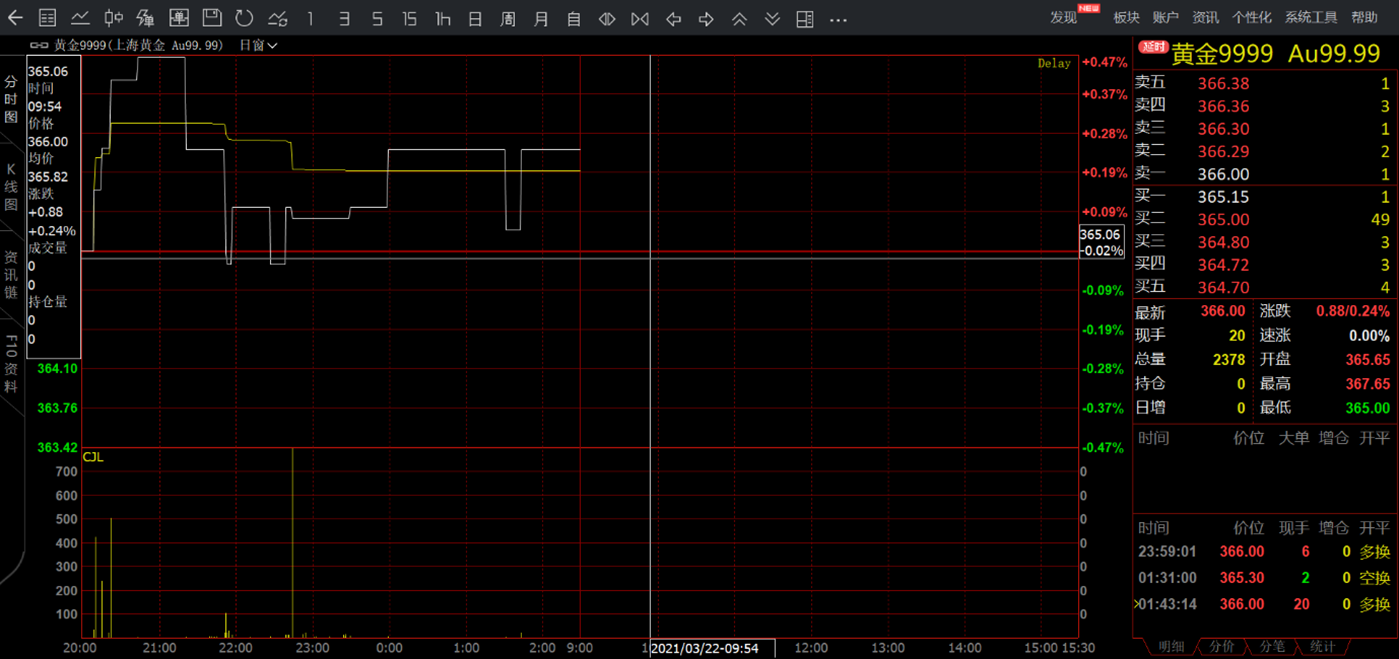

The order book of the Au99.99 contract of the Shanghai Gold Exchange, in the evening of March 22, 2021. Bid and ask prices are shown in red (top right corner); The corresponding quantities, in yellow, represent the depth of the market (liquidity). The highest bid price is ¥365.15 yuan per gram; The lowest ask rate is ¥366 yuan. The market was illiquid during this trading session as the quantities listed in the order book were very low.

The order book is transparent to all traders, and there is one central authority that sets the trading rules. This ensures that stock exchange trading is more transparent than trading in bilateral trading networks. The latter are also known as Over-the-counter (OTC) markets. There are traders who prefer stock exchange trading, and others who prefer OTC trading. The advantage of OTC trading is that it offers more flexibility and discretion.

Spot gold exchanges are thinly dispersed. Examples include the Shanghai Gold Exchange in China, the Borsa Istanbul in Turkey and the Dubai Gold and Commodities Exchange in the United Arab Emirates.

Arbitrage ensures that prices between different parts of the global gold market remain equal. When gold is cheaper in Dubai than in Shanghai, an arbitrator can reap profits without risk. The classic example is that an arbitrator takes his profits by buying physical gold where it's cheap and transporting it to where it's more expensive to sell. Whether the trade is profitable does not depend only on the price Spread, but also the costs of financing (interest), shipping, insurance, and, if necessary, the melting of bars. Alternatively, the arbitrator may take a long position on one exchange and a short position on the other until the spread is closed, at which point he closes his positions.

In general, gold is traded at a discount in net-exporting countries, such as South Africa, where domestic demand is lower than domestic mining production, versus a premium in countries that are net importers. Gold trading centres such as the United Kingdom (UK) can pivot from a net importer to a net exporter and vice versa. This ensures that local gold is trading at a premium or discount to parts of the world that trade with the U.K. (mostly Asia).

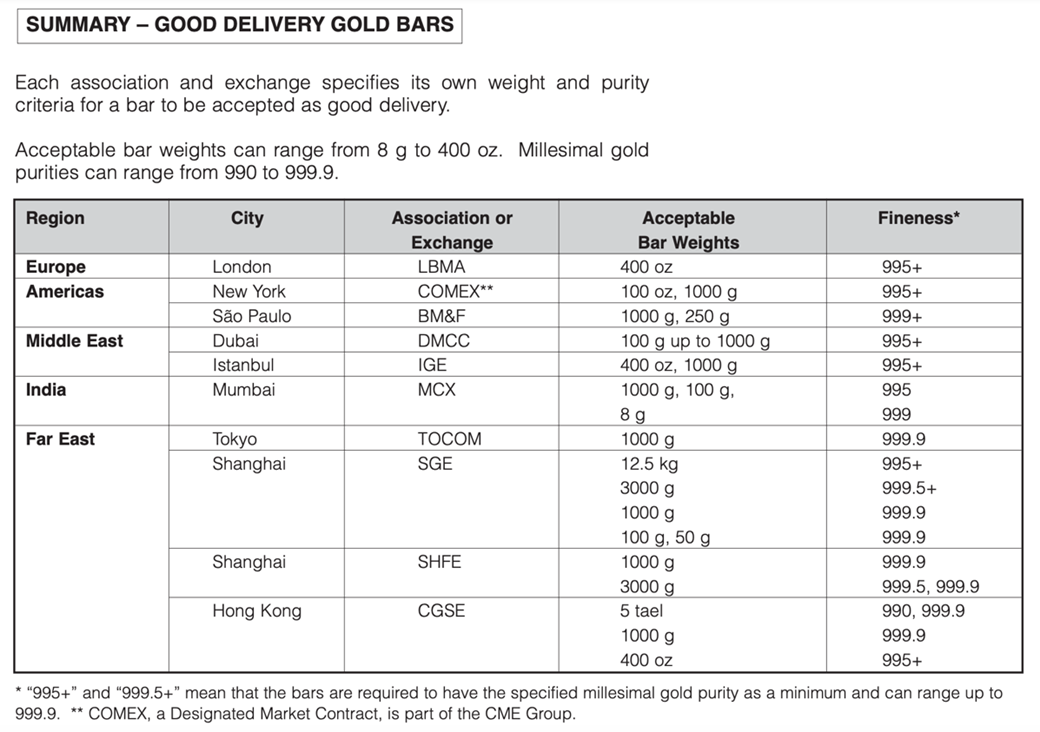

Gold bar standards around the world. On some of the exchanges mentioned above, only derivatives are traded. Source: Gold Bars Worldwide.

Gold bar weighing 187.5 grams (five taels) tradable on the Chinese Gold and Silver Exchange in Hong Kong.

In the previous chapter, we discussed that there are only a few physical gold exchanges worldwide. The majority of physical gold trading therefore takes place bilaterally. This means that two parties trade directly with each other, either through an electronic trading system, by telephone, or Face-to-face.

Because gold is not perishable and has retained its value for thousands of years, all the gold that has ever been mined is still in circulation. As a result, gold more like a currency than a commodity is traded in terms of supply and demand dynamics. Physical supply and demand is anything but limited to annual mine production and newly manufactured products.

Every day, gold is traded on a bilateral basis between thousands of companies—refineries, banks, traders, jewelers, miners, industrial producers, investors—and millions of individuals worldwide. Gold can be traded in any shape, and of course, in the supply chain its weight, shape or purity can be adjusted.

At the smallest level, a bilateral transaction might be a Turkish woman selling a gold bracelet to her male neighbor. By agreeing to its price, the neighbor exerts influence on the international price of gold, albeit extreme few. Because, if the neighbor rejected the woman's price , she would sell the bracelet to a jeweler who is connected to the international gold market where the supply would increase. Accepting its bid price ensures that the supply does not increase. This example makes it clear that in every (bilateral) transaction, buyer and seller influence the price of gold.

Gold jewellery on display in Abu Dhabi.

Business-to-business trading in a bilateral trading network is referred to as an OTC market. Globally, the London Bullion Market, overseen by the London Bullion Market Association (LBMA), is the most dominant OTC market for gold. Another essential OTC market is located in Switzerland: the capital of gold refining in the world. Every year, hundreds to thousands of tons of gold are transported to Switzerland, where, depending on demand, 400-ounce bars for London, 1 Kg bars for Asia, 100-ounce bars for New York, or other bars and products are manufactured. Also, there are many safes for investors in Switzerland.

The London Bullion Market has a special structure because it is based on bilateral trading and yet has a centralized nature. We will discuss this market in the next section on derivatives, because in the London Bullion Market, most transactions are carried out through "paper contracts."

A derivative is a financial contract whose value depends on an underlying asset. In this article, we will talk exclusively about derivatives with physical gold as the underlying asset. The main difference between physical gold and a derivative of gold is that owning physical gold does not carry any counterparty risk, unlike a derivative of gold. About other commodities, such as corn, it can be said, "you can eat corn, but you can't eat a derivative of corn." It boils down to the same economic conclusion: the physical supply cannot be increased by the creation of derivatives.

Despite this, derivatives have a significant impact on the physical price of gold. This is because they are traded in large volumes and they often use leverage. The most relevant derivatives markets are the paper market in London, Exchange Traded Funds, and the futures market in New York.

This article originally appeared on The Gold Observer