9.4

7.466 Reviews

English

EN

Savers who have more than a hundred thousand euros in their bank account lose almost 4% of their purchasing power every year. The interest rate on savings has long since ceased to compensate for wealth tax, let alone official inflation. Add negative interest rates to that and you're a thief of your own wallet if you save a lot of money. In ten years' time, a third of your purchasing power evaporates, while over a period of twenty years you even lose more than half. And that hasn't always been the case, because in the 90s, the savings interest rate was still enough to grow your wealth. What are the alternatives to saving?

From an early age, we were taught that it is important to save. Not only to be able to make large purchases, but also to build up a buffer for financial setbacks. Saving also yielded money, because you built up more and more capital over the years due to the interest rate. Those days are over, because since the financial crisis and the corona crisis, savings rates have only fallen further. Meanwhile you pay at all major Dutch banks even half a percent negative interest rate on savings above €100,000 to €150,000.

In the 1990s, a savings interest rate of 5 to 7 percent was still common, so that you could get a sufficient return as a saver. But due to a persistent decline in interest rates, saving has yielded less and less in recent years. Adjusted for official inflation and wealth tax, the return on savings has been negative for years. Especially for wealthy savers, because they also pay wealth tax to the government and interest to their bank. So, even if we rely on official inflation figures - which almost no one believes anymore - saving in a bank account is a good way to lose purchasing power.

Below you can see the effective return on savings over the past thirty years. We obtained figures from the savings rate of De Nederlandsche Bank and inflation rates of the Central Bureau of Statistics (CBS). For the period from 1991 to 2016, we have set the wealth tax at 1.2%. For the last five years, we have been using the new method of the Tax authorities to calculate the fictitious return. This results in a slightly higher wealth tax that fluctuates around 1.3%. We see that the effective return on savings has fallen sharply, especially in recent years.

Effective return on savings has been negative for years

This calculation example assumes a savings balance of more than €100,000, to which both wealth tax and negative interest apply. At less than a ton, you don't currently pay negative interest, but that could change in the future. In recent years, banks have increasingly lowered the threshold for negative interest rates, because they have to pay interest to the central bank on their excess reserves. This interest will increasingly be passed on to savers, especially when market interest rates remain so low.

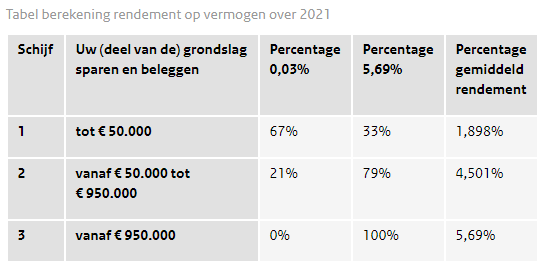

The wealth tax in the Netherlands spares most savers. Up to €50,000 you do not pay wealth tax, while assets between €50,000 and €1 million are taxed at a fictitious return of 4.5%. The Tax and Customs Administration taxes savings at a much lower fictitious return of 0.03%, but at the same time assumes that you invest the majority of your assets and earn a return of 5.69%. This brings the effective return to 4.5%, on which you then pay 30% tax. If you have more than €1 million in assets, the Tax and Customs Administration assumes that you invest the entire amount above that limit. Even if you keep it in a savings account and the interest rate is negative.

Calculation of wealth tax in 2021 (Source: Tax authorities)

For this calculation example, we used inflation figures from the Central Bureau of Statistics. According to these figures, the official inflation rate in the Netherlands has averaged about 2% per year over the past thirty years. The highest recorded inflation rate was in 2001, when the annual price level rose by 4.5%. Many Dutch people will probably experience this differently, because the costs of groceries and other fixed costs have risen much faster than two percent in recent years.

Based on empirical data, we would estimate the actual inflation rate to be a few percentage points higher than the official statistics. The website Shadowstats has been calculating inflation figures for years based on the traditional calculation method of the American statistical office. According to this calculation, inflation in the US has consistently been a few percentage points higher than the official figures indicate since the early 1980s. But even if we use the official inflation figures for the Netherlands, the savings rate has lagged behind the return required to maintain your purchasing power for years. The graph below shows this well.

Savings interest rates have been too low for years to maintain purchasing power

It is always useful to have some savings on hand, but it is no longer lucrative to park assets structurally and for a longer period of time in the savings account. Of course, you can look for an exotic bank that pays a fraction of a percent more interest, but that's not a solution. In fact, you may run more risk and are not always covered under the deposit guarantee scheme. You can also lock up money with a bank for a longer period of time to receive more interest, but we wouldn't really recommend that to anyone either. Should a new banking crisis break out, you will not be able to withdraw your money. If the bank where you parked your money fails, you will receive a maximum of €100,000 back under the deposit guarantee scheme.

If you have more than a ton of savings, it is wise to spread it over several banks. You can park a ton of savings per bank under the deposit guarantee scheme. Also, most banks only charge negative interest rates above €100,000, which makes it lucrative to spread assets across different banks. These options are worth considering if you have a few hundred thousand, but if you have more assets in euros, this becomes very inconvenient. In that case, it is advisable to invest your assets and spread them across different asset classes. On average, this also yields a much higher return than a savings account.

For all savers, the purchasing power of savings is currently evaporating. A few percent loss of purchasing power per year is the premium you currently pay for the security and convenience of a savings account (up to €100,000). This premium can increase considerably over a longer period of time, as we wrote in the introduction. Within ten years, you will have lost a third of your purchasing power. Therefore, it is attractive for all savers to consider alternatives.

For example, if you pay a high mortgage interest rate, it can be lucrative to make some extra repayments. This will save you on fixed costs in the long term. You can also choose to invest capital, for example in shares or precious metals. In the long run, these generate a return that is sufficient to maintain your purchasing power. Over the longer term, equities yield about 7 to 8 percent return per year, while the gold price has risen by a similar percentage over the past fifty years. So these are attractive alternatives to the savings account.

If you have a lot of wealth, you can also consider investing in real estate. This not only generates income in the form of rentals, but also an increase in the value of the home in the longer term, based on historical price developments. Finally, it is also possible to invest part of your assets in Bitcoin or other cryptocurrencies. Cryptocurrency returns have been very high in recent years, as has volatility. Savers may be able to invest a small part of their assets in it, because the potential upside much larger than the Downside. Precious metals such as gold and silver are then a safer alternative and more suitable as an alternative means of savings.

Disclaimer: Holland Gold does not provide investment advice and this article should not be considered as such. Past performance is no guarantee of future results.

This contribution was made from Geotrendlines