9.3

8.064 reviews

English

EN

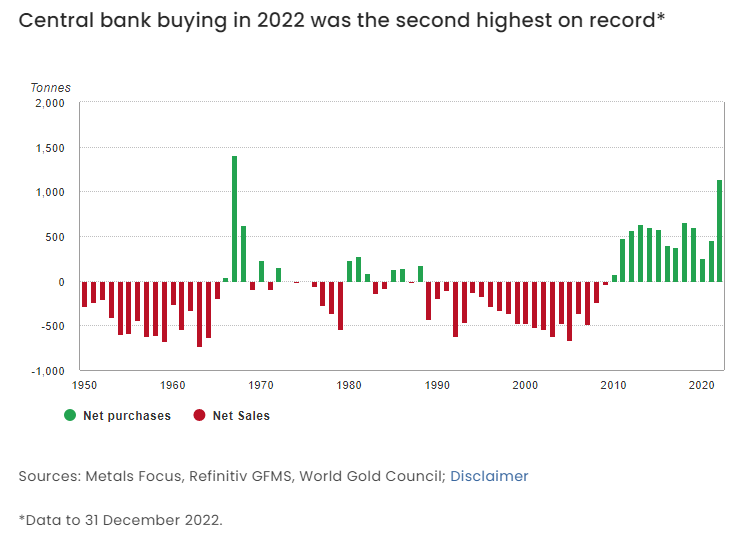

Central banks added 1,136 tonnes of gold to their reserves last year, the largest one-year purchases since 1967. Central banks bought a lot of gold in the fourth quarter in particular. Along with record demand for coins and bars in Europe and the U.S., overall global demand for gold reached its highest level in more than a decade. This is what the World Gold Council in its annual report on the gold market.

Geopolitical uncertainty and the need for diversification were the main drivers for central banks to buy more gold. Demand for investment gold also increased, as savers and investors are concerned about high inflation. Especially in Europe and the US, gold coins and bars were hard to come by. What were the key findings from the World Gold Council report?

Due to large purchases by central banks and investors, total global demand rose to 4,741 tonnes last year. That was the highest level since 2011, when the U.S. government was close to the debt ceiling and credit rating agencies downgraded the U.S. national debt. In that year, the gold price rose to a then-record of $1,920 per troy ounce. Last year, it was the war in Ukraine and high inflation that sparked a flight to gold. Still, demand for the precious metal did not rise across the board. Due to strict lockdowns, less gold was sold in China than usual. Demand for the precious metal also fell in gold ETFs and in the technology sector.

Central banks have been net buyers of gold since 2010. Central banks of emerging economies in particular have bought a lot of gold in recent years and that was also the case in 2022. As a result, central banks have been laying a solid foundation for the gold market and the gold price for twelve years in a row. Interestingly, only a quarter of the total gold purchases last year were reported to the IMF, the buyer of most of which is unknown. These are purchases that may be made by Russia or China or by large sovereign wealth funds from these countries. Russia already announced last year that the Less openness about its reserves, after Western countries decided to freeze Russia's assets.

Among the reported purchases, Turkey topped the list with the purchase of 148 tonnes of gold, followed by China with 62 tonnes. It was the first time since September 2019 that China had added precious metal to its reserves Added. Other major buyers were Egypt (+47 tonnes), Qatar (+35 tonnes), Uzbekistan (+34 tonnes), Iraq (+34 tonnes), India (+33 tonnes) and the United Arab Emirates (+25 tonnes). Ecuador, the Czech Republic, Serbia, Oman, Kyrgyzstan and Tajikistan also added a few tons of gold to their reserves last year. The only major seller was the central bank of Kazakhstan, which sold 51 tonnes of gold. In recent years, this country was still one of the largest buyers of gold.

For central banks, the gold stock is important because this reserve has no counterparty risk. And that is becoming increasingly important in a world with increasing geopolitical tensions and economic sanctions. Last year, Russia's foreign exchange reserves were blocked by Western countries, leaving the central bank unable to use half of its reserves. In that scenario, gold is more attractive because it cannot be sanctioned. For example, Russia keeps its entire gold reserves, which account for almost a quarter of its reserves, entirely in its own country.

Emerging economies will continue to expand their gold reserves in the coming years to strengthen their monetary and economic sovereignty. This is confirmed in a recently published paper from the IMF, which was co-written by Barry Eichengreen, among others. This economist wrote several books on gold and the monetary system. The report confirms the correlation between gold purchases by central banks and economic and financial sanctions. From the executive summary of the report:

"We document two sets of factors that contribute to this trend. First, gold is attractive to central bank reserve managers as a safe haven during periods of economic, financial and geopolitical volatility, when returns on alternative financial assets are low. Second, the imposition of financial sanctions by the United States, the United Kingdom, the European Union and Japan, the major reserve-issuing economies, is accompanied by an increase in the share of central bank reserves held in the form of gold."

Central banks' gold purchases reach highest level since 1967 (Source: World Gold Council)

Due to high inflation and geopolitical turmoil, there was a lot of demand for investment gold last year. Total demand increased by 10% to 1,106.8 tonnes, mainly due to additional purchases of coins and bars in the United States and Europe. The global demand for investment gold was above the average of the past five years and even rose to record highs in Western countries, as the graphs below show. In Germany, the demand for Gold Coins and last year by 13.1% to a New record of 196 tonnes. For the whole of Europe, the demand increased to more than 300 tonnes, which has only happened once before.

It was striking that the demand for gold coins and Gold bars in China last year was almost a quarter lower than a year earlier. According to the World Gold Council, this decline is attributable to strict lockdowns. As a result, the Chinese economy was running in a lower gear. If the Chinese economy fully reopens this year, it could give another boost to the gold market, due to pent-up demand from last year. Search results from search engine Baidu show that Chinese people searched for gold more often last year than in 2021. That suggests that the precious metal is still in high demand in China.

In India, too, demand for investment gold fell slightly year-on-year. This may have something to do with the relatively high average Gold price of $1,800 per troy ounce in 2022. In general, consumers in India and China buy less when gold prices are high, while private individuals in Western countries buy more gold.

Demand for investment gold rose in 2022 due to high inflation (Source: World Gold Council)

Western investors bought record amounts of gold coins and bars (Source: World Gold Council)

It was striking that the market for investment gold had two faces last year. While demand for coins and bars rose, gold ETF inventories fell by 110.4 tonnes. A possible explanation for this is that gold ETFs are mainly popular with investment funds and institutional parties, and that they are more influenced by the development of interest rates. Rising interest rates are usually unfavorable for gold, but due to high inflation, there is still a negative real interest rate. In 2020, falling interest rates led to a large inflow of wealth into gold ETFs.

Gold stocks ETFs down again in 2022 (Source: World Gold Council)

Global demand for jewellery fell 3% last year to 2,086.2 tonnes. This means that jewellery is still the most important market for gold. Globally, the market has largely recovered from the negative impact of the coronavirus pandemic and lockdowns, but in China the market lagged last year. Demand for jewellery fell by 15% to 570.9 tonnes, 113 tonnes less than the average of the past ten years. The graphs below show that the demand for jewellery has been in a slightly downward trend in recent years.

Global demand for jewellery slightly down in 2022 (Source: World Gold Council)

Chinese Jewelry Demand Lower Than 10-Year Average (Source: World Gold Council)

The demand for gold for industrial applications is generally fairly constant, but there was a clear decline in the fourth quarter. Total demand from the electronics sector fell by 7% to 251.7 tonnes. Due to the deteriorating economic outlook, sales of mobile phones and computers declined. In fact, computer sales fell 28% in the fourth quarter, the biggest drop in three decades. The economic outlook for this year is not much better, but the technology sector represents only 10 to 15 percent of the total gold market. Changes in this market segment therefore have a relatively limited impact on the overall gold market.

The total global supply of gold rose 2% last year to 4,754 tonnes, of which 3,611.9 tonnes came from gold mines and 1,144 tonnes from recycling. Gold mine production rose by only 1% compared to a year earlier, despite the relatively high gold price. From this we can conclude that it is becoming increasingly difficult for the mining sector to further increase production. China managed to increase its gold production by 42 tonnes in 2022, but production fell in Russia and South Africa. Production also fell in Mexico and Colombia.

The average production costs of gold miners, the so-called all-in sustaining costs (AISC), rose to $1,289 per troy ounce in the third quarter of last year. That's the cost of extracting the gold from the ground and finding new underground gold reserves. In the space of a year, these costs have increased by 14%, mainly due to high energy prices. These had a downward effect on the profit margin of gold miners in the fourth quarter. Despite this, it remains lucrative for most mines to extract gold, although it is becoming increasingly difficult for mines to find high-quality gold reserves.

Production of gold mines barely increases (Source: World Gold Council)

The supply of scrap gold last year was comparable to 2021. In the first half, the high gold price provided additional supply, but this was offset by lower supply in the second half of the year. It is striking that in recent years there has been much less scrap gold on the market than in the period from 2009 to 2012. According to the World Gold Council, much more gold came onto the market at that time due to the combination of an economic crisis and the high gold price. A lot of scrap gold has already been melted down in that time. The fact that there is now less scrap gold on the market, despite high inflation and a poor economic outlook, is probably due to the large-scale fiscal support measures. As a result, people are better off financially now than in the years after the 2008 credit crisis.

Supply of scrap gold stabilises at a lower level (Source: World Gold Council)

Also read these articles: